Valued at a market capitalization of roughly $76.5 billion, Elevance Health, Inc. (ELV) positions itself as a lifelong, trusted health partner, driven by a mission to improve the health of humanity. The company supports individuals, families, and communities at every stage of the healthcare journey, connecting them with the care, tools, and resources needed to live healthier, more fulfilling lives.

Through a broad and integrated portfolio spanning medical, pharmacy, behavioral, clinical, home health, and complex care solutions, Elevance Health serves more than 109 million consumers nationwide. Headquartered in Indianapolis, Indiana, the company stands out for its scale, reach, and holistic approach to delivering modern healthcare solutions. The company is planning to lift the curtain on its fiscal 2025 fourth-quarter earnings results at the end of January next year.

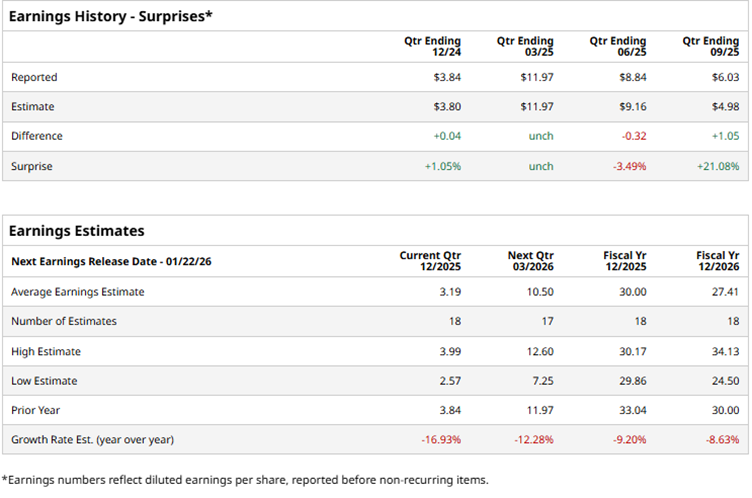

Heading into the report, expectations are clearly tempered. Wall Street analysts forecast Elevance Health’s EPS to fall nearly 17% year over year to $3.19, setting a cautious near-term backdrop. The company’s earnings track record has been mixed, having met or beaten estimates in three of the past four quarters, with just one miss along the way. Looking further out, the pressure is expected to persist, with fiscal 2025 EPS projected to decline 9.2% to $30, followed by another 8.6% drop in fiscal 2026 to $27.41.

Elevance Health shares have struggled to keep pace with the broader market, sliding 6% over the past year. By comparison, the broader S&P 500 Index ($SPX) advanced a solid 16% over the same period, while the SPDR S&P Health Care Services ETF (XHS) surged 20.1%.

On Oct. 21, Elevance Health delivered a fiscal 2025 third-quarter earnings report that comfortably beat Wall Street expectations on both the top and bottom lines, underscoring the strength of its operating model. Total revenue surged 12% year over year to $50.71 billion, easily topping consensus estimates of $49.52 billion, as the company benefited from continued growth across its diversified healthcare platform.

Management highlighted its focus on improving affordability and enhancing the member experience, driven by expanding value-based care partnerships and AI-enabled digital solutions designed to simplify access and improve health outcomes. While adjusted EPS declined 30% year over year to $6.03, the figure still handily beat expectations of $4.98, signaling resilient execution despite margin pressures in a rapidly evolving healthcare landscape.

Wall Street’s view on Elevance Health is cautious but tilted to the upside, with the stock carrying an overall “Moderate Buy” consensus. Of the 21 analysts covering ELV, 11 rate it a “Strong Buy” and one assigns a “Moderate Buy,” signaling confidence in the company’s longer-term fundamentals. Meanwhile, nine analysts remain on the sidelines with a “Hold,” reflecting near-term uncertainty. The average price target of $387.63 points to 12.6% upside from current levels.

On the date of publication, Anushka Mukherjee did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart