Coinbase Global (COIN) has been the place where retail investors buy Bitcoin (BTCUSD) at midnight and track Ethereum (ETHUSD) before breakfast. Founded as a pure-play crypto exchange, the New York-based platform built its reputation on making digital assets accessible to the everyday investor. Now, it is expanding that playbook.

Beyond crypto, Coinbase has rolled out commission-free stock and ETF trading for all U.S. users – 24 hours a day, five days a week. Over 8,000 U.S.-listed equities and ETFs are now available inside the same app where users trade Bitcoin, complete with $1 fractional shares, instant funding via dollars or USDC, and seamless integration with Yahoo Finance for one-click execution.

The move places Coinbase squarely in competition with some prominent players in this space, which have aggressively courted retail trader cash. But this is not just about matching features. CEO Brian Armstrong has framed it as part of his “Everything Exchange” vision; bridging traditional finance and the digital asset economy under one unified portfolio.

And Coinbase is not stopping there, with plans to expand its stock offerings, introduce tokenized equities, and broaden access to stock perpetuals for international traders seeking 24/7 exposure to U.S. markets.

With COIN stock having lost more than half its value since July peak, is this expansion the catalyst investors have been waiting for, or just another ambitious bet in an increasingly crowded space? Should investors be snapping up COIN now?

About Coinbase Stock

Founded in 2012, Coinbase is a Delaware-based crypto giant, boasting a $47.8 billion market cap. As one of the largest exchanges globally, it serves both retail and institutional investors. Beyond trading, it is expanding through global licenses, acquisitions, and innovations like stablecoin payments, crypto cards, and subscriptions, positioning itself as a key architect in the evolution of digital finance.

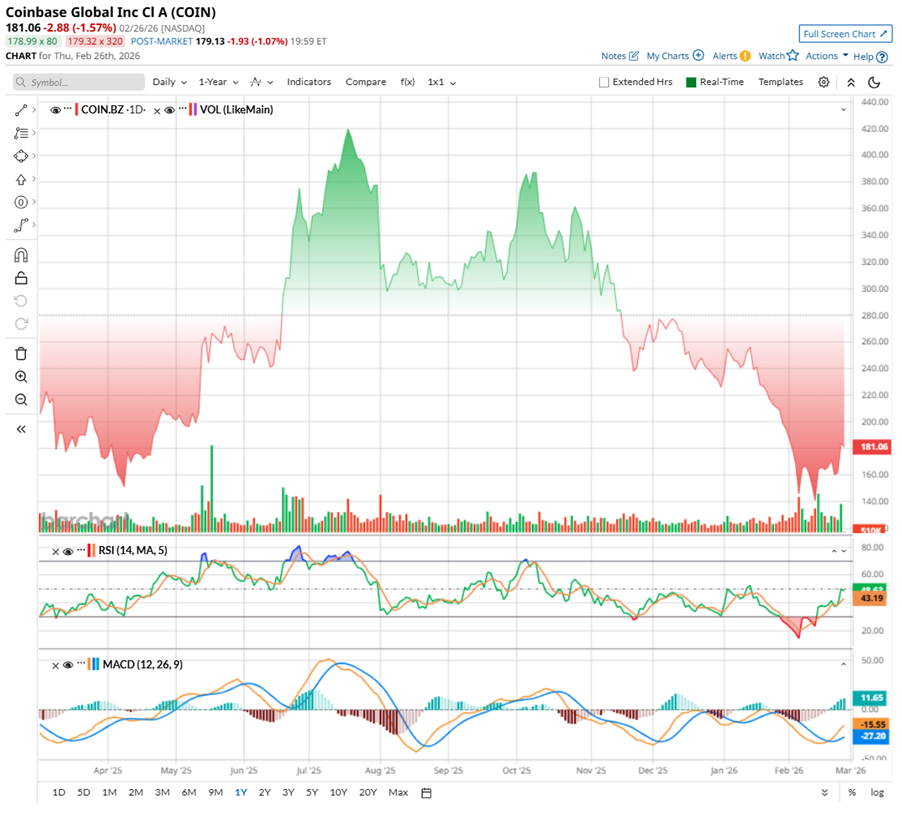

Coinbase’s shares have largely moved in sync with the broader crypto cycle. When Bitcoin rallied and regulatory sentiment improved, COIN rode that optimism, sprinting to a July peak of $444.64. But as quickly as momentum built, it faded. A broad pullback in digital assets sent the shares tumbling nearly 59% from those highs. Over the past six months, the stock is down about 43.09%, and it has slipped roughly 16.59% over just the past one month.

Still, the recent price action hints at stabilization. Over the past five trading sessions, COIN has rose 2.63%, helped by improving crypto sentiment and the company’s official rollout of U.S. stock and ETF trading as part of its “Everything Exchange” push. A partnership with Yahoo Finance and a positive turn in the Coinbase Premium indicator added to confidence.

From a technical standpoint, trading volume has started to pick up, which is often an early sign that investor interest is returning. The 14-day RSI, which had slipped into oversold territory in February, has now rebounded to around 46.31, suggesting that selling pressure is cooling rather than intensifying.

Momentum indicators are also turning constructive. The MACD line recently crossed above its signal line after spending weeks below it, a shift that typically signals improving bullish momentum. Plus, the histogram has moved into positive territory, indicating that upward momentum is gradually building. While it is not a full breakout yet, the setup suggests the stock may be attempting to stabilize and form a near-term base.

Coinbase Reports Mixed Results

Coinbase delivered its fourth-quarter 2025 results on Feb. 12, against a mixed backdrop for crypto markets and uneven investor sentiment. The numbers told a story of resilience, but also pressure. Total revenue amounted to $1.78 billion, down 22% year-over-year (YOY) and roughly in line with expectations. Non-GAAP EPS landed at $0.66, sharply lower than $3.37 a year ago, as softer trading activity weighed on fees.

Net revenue slipped 22.2% to $1.71 billion. Transaction revenue fell 37% to $982.7 million amid lower volumes, but subscription and services revenue rose 13.5% to $727.4 million, supported by stronger stablecoin income and recurring services. Adjusted EBITDA stayed positive, though well below last year’s level.

For the full year, total trading volume surged to $5.23 trillion, marking a sharp 156% jump from the prior year, signaling how active the platform was during crypto’s rebound phases. However, the company did not disclose an overall trading volume figure specifically for Q4. On the consumer side, Q4 spot trading volume came in at $56 billion, slipping 6% sequentially as retail activity cooled. Institutional spot trading was stronger in absolute terms at $215 billion for Q4, though that too declined 13% sequentially, reflecting softer participation from larger players.

Importantly, Coinbase’s balance sheet remained solid. Cash stood at $11.28 billion, and free cash flow was supported by operations. Coinbase One subscribers hit a record near 1 million. The company also added $39 million in Bitcoin to its investment portfolio through steady weekly purchases.

Capital returns were another headline. In Q4, Coinbase repurchased about 3.3 million shares for $850 million, and bought back another 4.9 million shares for $895 million by Feb. 10, 2026. Altogether, the $1.7 billion in buybacks more than offset 2025 stock-based compensation dilution. In January, the board approved an additional $2 billion repurchase authorization, leaving $2.3 billion available as of Feb. 10.

Looking ahead to Q1 2026, management expects subscription and services revenue between $550 million and $630 million. Transaction expenses should land in the low-to-mid teens as a percentage of net revenue. Operating costs remain elevated, with R&D and G&A projected at $925 million to $975 million, sales and marketing at $215 million to $315 million, and stock-based compensation around $250 million.

Despite volatility, management highlighted rising market share, strong product engagement, Base network growth, and ongoing international and regulatory opportunities.

Analysts monitoring Coinbase expect the company’s bottom line to decline by 70.6% YOY to $0.57 per share in Q1, with revenue anticipated to be around $1.59 billion. Adjusted EPS for fiscal 2026 is projected to be around $3.32, down 17.6% YOY. However, in fiscal 2027, EPS on an adjusted basis is anticipated to surge 31.6% annually to $4.37.

What Do Analysts Expect for Coinbase Stock?

Wall Street has not exactly turned bearish on Coinbase, but it has turned more cautious. This month, several brokerage firms trimmed their price targets on COIN, reflecting a more measured outlook. Bank of America, for instance, lowered its target to $288 from $340 recently, though it maintained a “Buy” rating. The firm is adjusting earnings estimates across brokers and exchanges following recent quarterly results.

Meanwhile, Mizuho's analyst Dan Dolev cut his target sharply to $170 from $280 and kept a “Neutral” stance, pointing to weaker Bitcoin prices and ongoing pressure from the crypto downturn. In fact, Mizuho believes Robinhood (HOOD) may currently be better positioned than Coinbase in this environment.

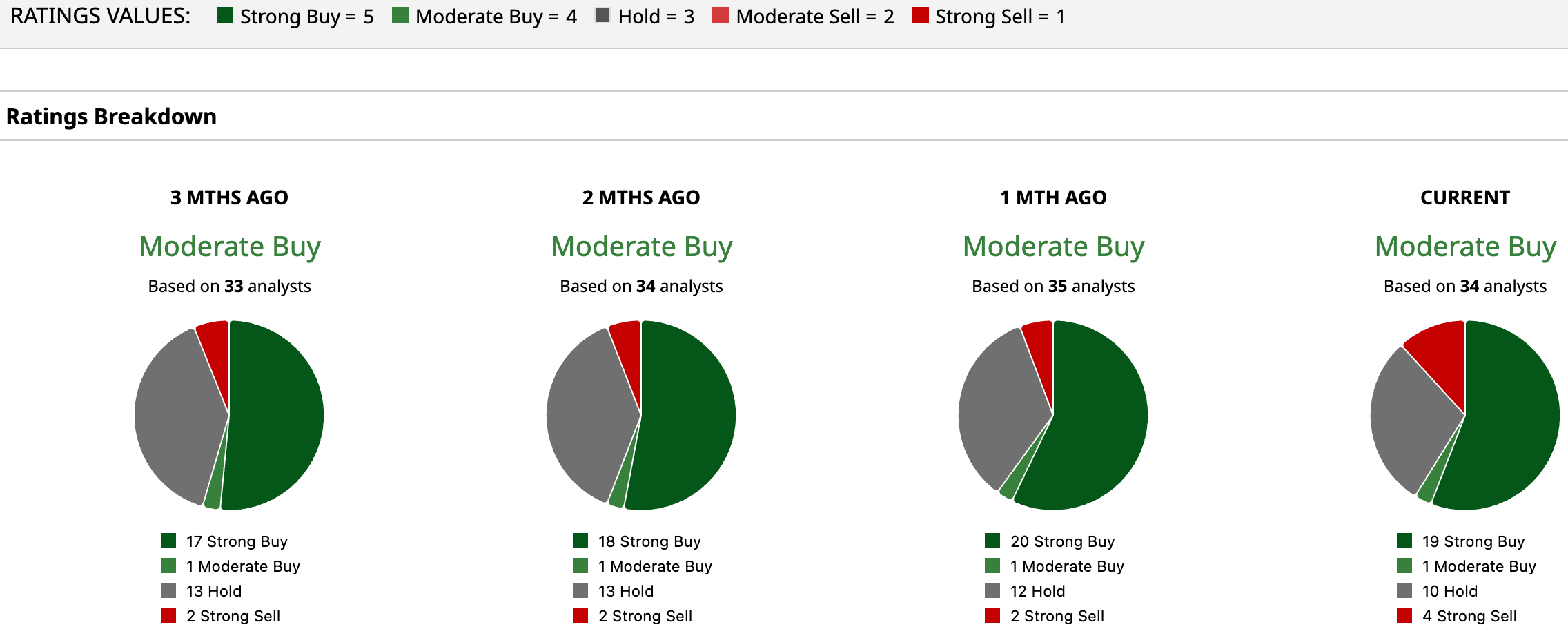

Wall Street leans bullish on COIN, with the stock having a “Moderate Buy” consensus rating overall. Out of 34 analysts, 19 now rate it a “Strong Buy,” one calls it a “Moderate Buy.” 10 analysts are playing it safe with a “Hold,” and the remaining four are outright bearish with a “Strong Sell” rating.

The mean price target of $250.49 implies rebound potential of 42.4%. Meanwhile, the Street’s highest projection of $440 suggests COIN stock could rise as much as 150% from here.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- As Coinbase Rolls out 24/5 Stock Trading, Should You Snap up COIN?

- Circle Stock Is Soaring on Earnings, and 1 Analyst Thinks It Can Still Gain 260% from Here

- As Circle Stock Breaks Through Key Resistance Levels, Should You Chase the CRCL Rally?

- Could This 1 Surprising Stock Be the Best Buy for a Future Dominated by AI Agents?