Nvidia, Inc. (NVDA) stock may be deeply oversold after its earnings release last week. It could be worth over 50% more, using an FCF valuation, as shown in my Feb. 27 Barchart article. Two plays: sell short OTM one-month puts for a 3% yield; buy ITM calls six months out.

NVDA closed at $177.19 on Friday, Feb. 27, down from the pre-earnings Feb. 25 peak of $195.56, but still higher than a recent trough of $171.88, although its six-month low is $167.02 on Sept. 5.

Has this drop been overdone? It looks like that is the case, especially given Nvidia's strong free cash flow (FCF) and FCF margins.

I discussed thisin my Feb. 27 Barchart article, “Nvidia's Massive Free Cash Flow Margins Could Push NVDA Stock 45% Higher.” I showed that NVDA could be worth $263 per share.

Higher NVDA Price Target

Here is a summary of how I estimated that price target.

NVIDIA generated a 44.7% FCF margin in 2025. FCF could rise to $161 billion in 2026. This is based on analysts' 2026 revenue estimates of about $365 billion, using a 44% FCF margin:

$364.38b x 0.44 = $160.3b

That means its valuation could rise to $6,412 billion, using a 2.5% FCF yield metric:

$160.3b est. FCF/ 0.025 = $6,412 billion

That's 49% higher than its $4.307 trillion market cap, according to Yahoo! Finance. So, the price target is 48.8% higher:

$177.19 price today x 1.488 = $263 price target (PT)

The point is that based on Nvidia's strong FCF margins, if they persist over 2026 (and there's every reason to believe this will be the case based on management guidance), NVDA stock looks deeply undervalued.

However, NVDA stock could stay cheap for a while. So, what is the best play here?

Shorting Out-of-the-Money (OTM) NVDA Puts

One way to play NVDA, especially for value investors who want to set a potentially lower buy-in point, is to sell short out-of-the-money (OTM) puts in one-month expiry periods.

That way, an investor can get paid after posting collateral and waiting to buy into NVDA at a lower (i.e., OTM) price.

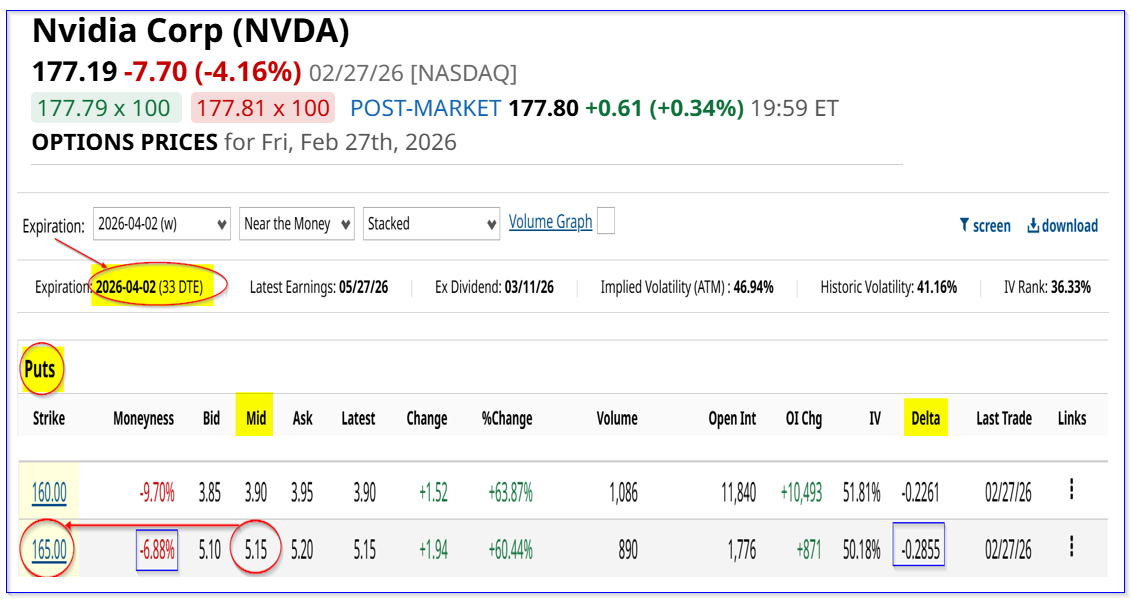

For example, the April 2, 2026, expiry period shows that the $165.00 put strike price, which is over 6.8% lower than Friday's close, has a high premium. As a result, its $5.15 midpoint price gives a short-seller of this contract an immediate 3.12% one-month yield (i.e., $5.15/$165.00).

Here is what that means in practice.

First, the investor contributes $16,500 in cash or buying power with their brokerage firm. The $16.5K serves as collateral if NVDA falls to $165.00 on or before April 2 (i.e., $165 x 100 shs per put contract).

The investor can then enter an order to “Sell to Open” 1 put contract at $165.00. The cash-secured collateral allows the brokerage firm to lend the put contracts to the selling investor to sell them short, without owning them in the first, or “open,” trade.

At some point, the investor will have to “Buy to Close” the contract or, if the stock stays over $165.00 by April 4, the contract will expire. At that point, the collateral is released back to the investor (i.e., the $16.5K in cash is no longer restricted).

Next, the brokerage firm will immediately post $515 (i.e., $5.15 x 100 shs per contract) into the short-seller's account. So, the investment has immediately yielded 3.12%:

$515/$16,500 = 0.0312 = 3.12% for one month

Moreover, this also means the investor has a potentially much lower breakeven (B/E) point, if NVDA falls to $165.00 on or before April 2:

$165.00 - $5.15 = $159.85 breakeven (B/E)

That B/E is almost 10% below Friday's close (i.e., -9.79% lower than $177.19). That's why value investors love this kind of play. They get paid while waiting to buy in at a lower price.

Note that a more risk-averse investor can short the $160.00 put contract, which is 9.7% lower than Friday's close, providing more downside protection. They can make a 2.3475% one-month yield ($3.90/$160.00), with a 11.9% lower B/E ($156.10/$177.19-1).

Buying ITM Calls

But, what if NVDA rises from here or never falls to $165.00? The short-put investor gets no upside in the price as a long-term value buyer would have.

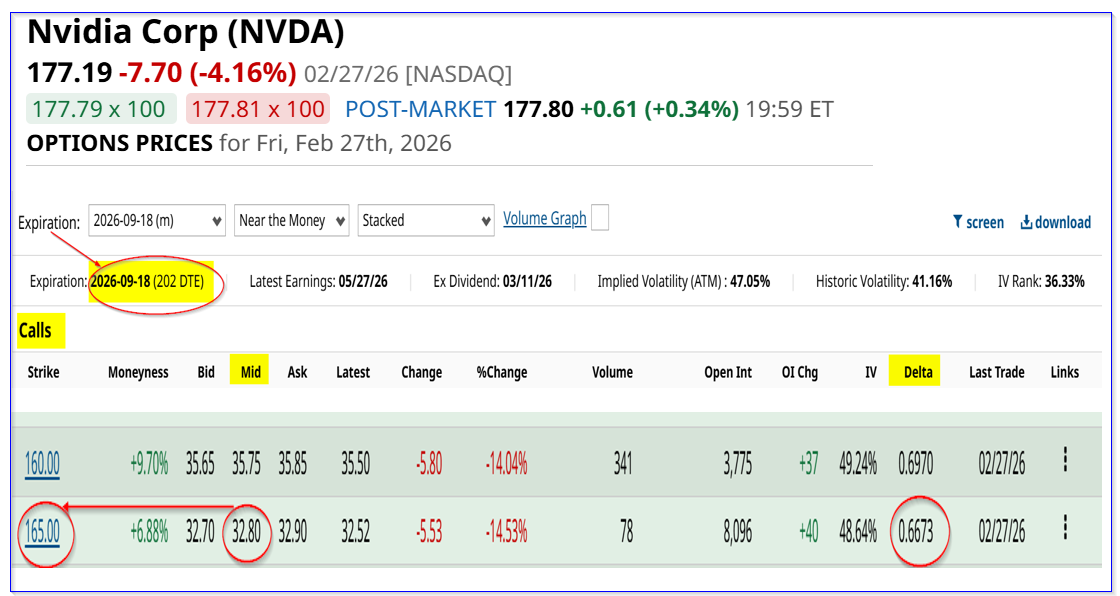

One way to play this is to also buy a 6-month expiry call option at the same $165.00 strike price. This call option is in-the-money (ITM), since the spot price, $177.19, is higher than the call strike price.

For example, the Sept. 18, 2026, expiry period shows that the $165.00 call option has a midpoint premium of $32.80. That means the investor has to pay $3,280 for this call option.

Its intrinsic value is $177.19-$165.00, or $12.19, or $1,219 per contract. So, the extra amount being paid for this call (i.e., its extrinsic value) is:

$32.80-$12.19 = $20.61, or $2,061 per contract

However, if an investor can keep making $515 for 6 months by shorting one-month OTM puts, the total accumulated would be $3,090. That more than covers the extrinsic value paid.

For example, assume the investor can make $3,000 shorting OTM puts for 6 months:

$3,280 paid for the call - $3,000 income from puts = $280 net cost for the 9/19/26 call

In other words, the investor would have a net cost of $16,780 per share (i.e., $16,500 +$280/100 or $167.80 per call) if they were to exercise the call.

So, if NVDA closes at $220 on Sept. 19, the total return would be:

$22,000 - $16,780 = $5,220

Given the $16,500 cash-secured collateral outlay to short puts each month, this works out to a 6-month ROI of 31.6%:

$5,220 / $16,500 = 0.3164 = 31.64%

A long-only buyer of NVDA would have made 24.16% (i.e., $220/$177.19), or +$4,281 for 100 shares. However, the short-put investor would still have use of the $16,500 returned collateral.

So, the investor's actual ROI is much higher, given its lower cost base, the accumulation of short-put play income during this period, and the in-the-money (ITM) call downside protection.

The bottom line is that value investors love shorting OTM puts and buying ITM calls in NVDA stock at today's prices.

On the date of publication, Mark R. Hake, CFA did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart