SoFi Technologies (SOFI) has been delivering solid financial results quarter after quarter. It continues to attract new members rapidly. At the same time, existing customers are adopting more of the company’s products. These factors are driving SoFi’s financials at a solid pace.

In addition, SoFi’s evolving business mix supports long-term growth. While lending still plays a significant role, SoFi has been rapidly expanding into other segments, including financial services and its technology platform. These businesses are becoming increasingly important to SoFi’s growth story and could make the company less dependent on lending over time.

Further, management is confident that the momentum isn’t slowing down anytime soon. The company expects solid growth trends across its platform to continue through 2028.

While SoFi is firing on all cylinders, concerns about valuation and the potential dilutive impact of capital raises have weighed on the stock. As a result, SoFi shares have declined 29.28% year-to-date (YTD) and now trade 43.4% below its 52-week high.

However, the company’s continued strong business performance and solid fundamentals indicate a steep recovery in its share price.

SoFi to Continue Growing Rapidly

SoFi is rapidly scaling its operations, with adjusted net revenue climbing 37% in the fourth quarter of 2025 alone. Looking ahead, management expects this momentum to carry into 2026, projecting revenue growth of roughly 30%. At the same time, SoFi anticipates its total member base will increase by at least 30% year-over-year (YOY), reflecting the company’s ability to consistently attract new customers.

Further, SoFi is seeing a strong uptake across its product ecosystem. Importantly, many existing members are adopting additional financial products, a trend that significantly strengthens customer relationships. This lowers customer acquisition costs and increases customers’ lifetime value.

Supporting SoFi’s growth is the diversification of its revenue streams. The company has been expanding its fee-based revenue, which carry lower credit risk and is less sensitive to interest-rate cycles. This transition is creating a more stable and durable earnings foundation.

Also, SoFi is likely to benefit from opportunities in artificial intelligence (AI), cryptocurrency, and broader banking capabilities, thereby expanding its addressable market.

Financially, SoFi remains well-positioned to support its growth. The company recently secured $3.2 billion in new capital and continues to benefit from a steadily increasing deposit base. Management used the new capital to pay down higher-cost debt and other expensive funding sources, while allocating the remainder toward income-generating assets. This strategy should help offset the dilutive impact of issuing new shares while improving overall financial efficiency.

Thanks to the momentum in its top line and improving efficiency, SoFi’s earnings could register solid growth. SoFi projects adjusted earnings per share of about $0.60 in 2026, up significantly from $0.39 in 2025.

Beyond 206, SoFi’s outlook remains compelling. With a diversified revenue base, improving balance sheet strength, and expansion opportunities across both new and existing business lines, the company expects revenue to grow at a CAGR of 30% through 2028. Over the same period, adjusted EPS is forecasted to grow even faster, at an estimated annual rate of 38% to 42%.

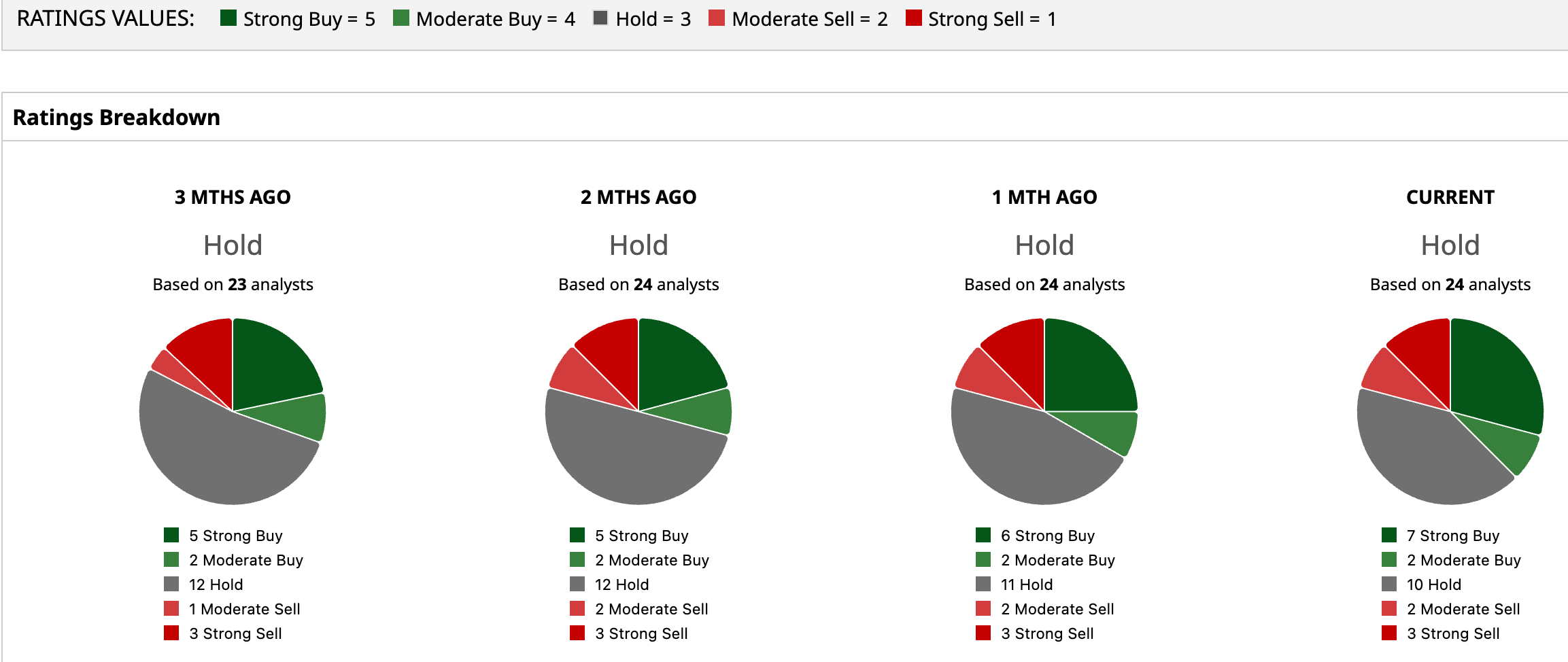

Analysts See Significant Upside in SoFi

The solid momentum in SoFi’s top and bottom lines is likely to support the recovery in its stock. And, the recent selloff in the stock has helped ease earlier concerns about valuation. At the same time, the company’s decision to deploy newly raised funds to reduce debt and lower financing costs strengthens its balance sheet and positions SoFi to generate stronger earnings over time. This should mitigate investor concerns about dilution from capital raises.

Although analysts currently maintain a consensus “Hold” rating on SoFi stock, the average price target of $26.88 suggests considerable room for appreciation from current levels, implying roughly 45% upside.

On the date of publication, Sneha Nahata did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Starboard Value Is Betting Big on This Blue-Chip Dividend Stock. Should You?

- AMZN vs. WMT: Which Is the Better Stock to Buy for the Next 10 Years?

- Why Jefferies Says Microsoft Stock Looks Cheap Despite AI Growth

- Navitas Stock Shoots Above Key Support Levels on AI Data Center Pivot. Should You Buy NVTS Shares Here?