The semiconductor sector has suddenly found itself caught in an unexpected storm thanks to rising oil (CBK26) prices. As tensions escalate in the Middle East, particularly around shipping routes through the Strait of Hormuz, global energy markets have turned volatile. The disruption has pushed crude oil prices sharply higher, briefly surging past the $100 mark and sending ripples through financial markets. And semiconductor stocks are not immune from the tremors.

At first glance, oil and chips might seem worlds apart. But the connection becomes clearer when we look at the energy backbone of modern computing. Semiconductors sit at the heart of everything from cloud computing to artificial intelligence (AI), powering the massive data centers that train and run AI models. These facilities are extremely energy-intensive, relying on power-hungry processors and sophisticated cooling systems. When oil prices surge, energy markets tighten broadly, pushing up electricity costs and potentially slowing the pace at which tech giants can build new data centers and buy more chips.

There is also a supply-chain angle. Critical materials like helium and bromine are essential for semiconductor manufacturing, helping cool equipment and support chip lithography. Any more disruption to transport routes in the region could tighten supply further.

Against this backdrop, the iShares Semiconductor ETF (SOXX) declined 3.5% as of Thursday’s close, and chip heavyweights like Nvidia (NVDA) and Advanced Micro Devices (AMD) slid as well as investors digest the risks. So, is this energy-driven pullback just a temporary shakeout, or an opportunity to pick up these two semiconductor leaders at a discount?

Should You Buy the Dip in Nvidia Stock?

Nvidia hardly needs an introduction. Once celebrated as the king of gaming graphics, it is now the backbone of modern computing. Its GPUs power data centers, AI, robotics, and immersive digital worlds. The CUDA software platform locked developers into a powerful ecosystem, turning Nvidia into an industry standard rather than a supplier. With a market capitalization of $4.45 trillion, the company has become the engine of the AI economy.

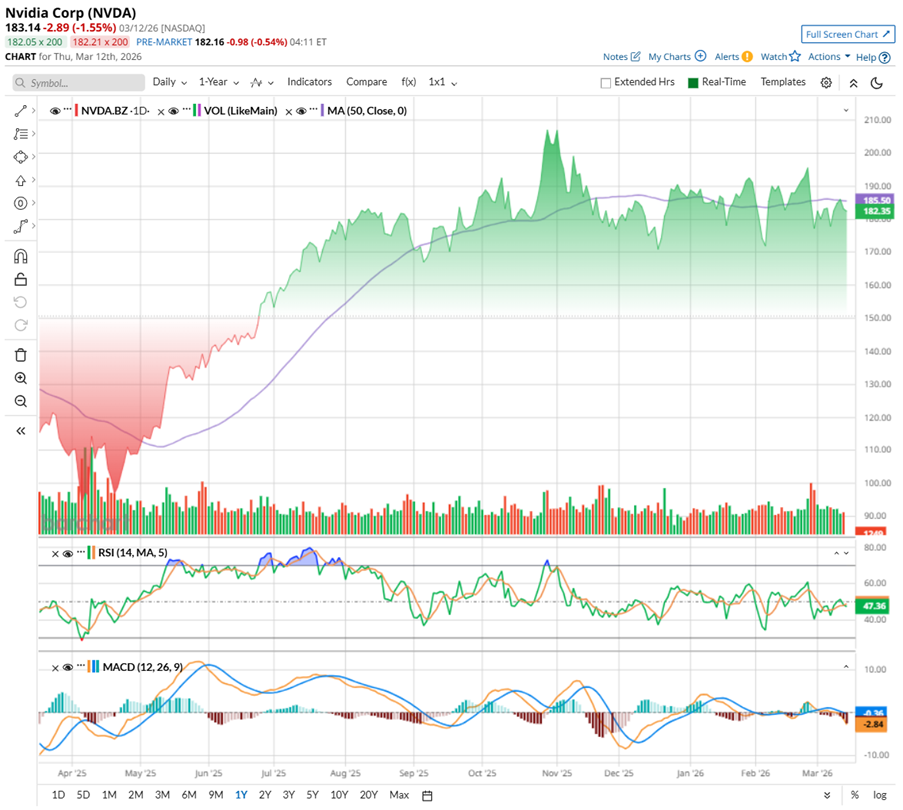

Nvidia's shares have spent the past year climbing in steady waves — rallies, quick breathers, then another push higher. The stock sprinted to a high of $212.19 on Oct. 29, 2025 before cooling off, sliding roughly 13.7% from that high. Even so, the bigger picture still looks strong, with the shares up nearly 58% over the past 52 weeks.

Lately, though, the mood around chip stocks has turned jittery. Oil shocks, inflation worries, and a slump in smartphone demand spooked investors, and Nvidia has not been immune. The stock has slipped below its 50-day moving average, a signal that short-term momentum has taken a breather.

Trading activity also hints at that slowdown. Recent sessions have seen more red volume bars, suggesting sellers have been a bit louder than buyers. Meanwhile, the 14-day relative strength index (RSI) has cooled to around 47 after flirting with overbought levels during October’s rally. Nvidia's run has not broken, but right now, it is clearly catching its breath. The stock may be gearing up for another run higher if buying interest returns.

Valuation-wise, NVDA might look a little pricey compared to its pers, given that it is currently trading around 22.2x forward adjusted earnings and 12.1x forward sales. But zoom out, and that valuation actually sits below its own historical averages, even after the stock’s monster five-year run.

With strong double-digit growth, healthy profit margins, and rising demand from the AI industry, the premium valuation reflects the strength of Nvidia’s market position rather than speculation. In addition, the company has maintained a consistent track record of returning value to investors, having paid dividends for 13 consecutive years.

Nvidia's Latest Earnings Report

When Nvidia unveiled its fiscal fourth-quarter 2026 results on Feb. 25, the numbers once again reminded Wall Street why the company sits at the center of the AI computing boom. The chip giant delivered results that comfortably topped expectations, with revenue climbing to $68.1 billion, up 73.2% year-over-year. Adjusted earnings per share (EPS) jumped 82% annually to $1.62, easily beating analysts’ forecasts.

Demand from hyperscale cloud providers and enterprises racing to build AI infrastructure pushed Nvidia’s data center revenue to $62.3 billion, a roughly 75% annual surge. Gaming also added momentum, with its revenue for Q4 reaching $3.7 billion in the quarter, up about 47% year-over-year, as Nvidia’s latest Blackwell architecture gained traction among high-performance graphics users.

The company is operating from a position of strength. As of Jan. 25, 2026, Nvidia held $62.6 billion in cash, cash equivalents, and marketable securities, while long-term debt stood at just $7.46 billion. The business generated $34.9 billion in free cash flow in the fourth quarter alone and an impressive $96.58 billion in fiscal 2026.

That financial firepower has also translated into generous shareholder returns. During fiscal 2026, Nvidia returned $41.1 billion through share buybacks and dividends, with $58.5 billion still available under its repurchase authorization as of the end of Q4.

The company continues to push the technological frontier. During the annual CES in Las Vegas, Nvidia introduced its next-generation AI superchip, Vera Rubin, designed to deliver 10x the performance per watt of its predecessor, Grace Blackwell. Shipments are expected to begin in the second half of 2026, with future architectures, including Rubin Ultra and Feynman chips, already mapped out for the coming years.

With CEO Jensen Huang describing demand as “skyrocketing,” Nvidia’s outlook reflects that momentum. The company expects fiscal first-quarter 2027 revenue to reach about $78 billion, plus or minus 2%, reinforcing the idea that the global race to build AI infrastructure is accelerating.

What Wall Street Thinks About NVDA Stock

Meanwhile, analysts tracking Nvidia are estimating Q1 fiscal year 2027 EPS to grow 116.9% year-over-year to $1.67. For the full fiscal year 2027, the bottom line is expected to surge 64.6% annually to $7.52 per share, followed by another 25.5% year-over-year increase in fiscal 2028 to $9.44 per share.

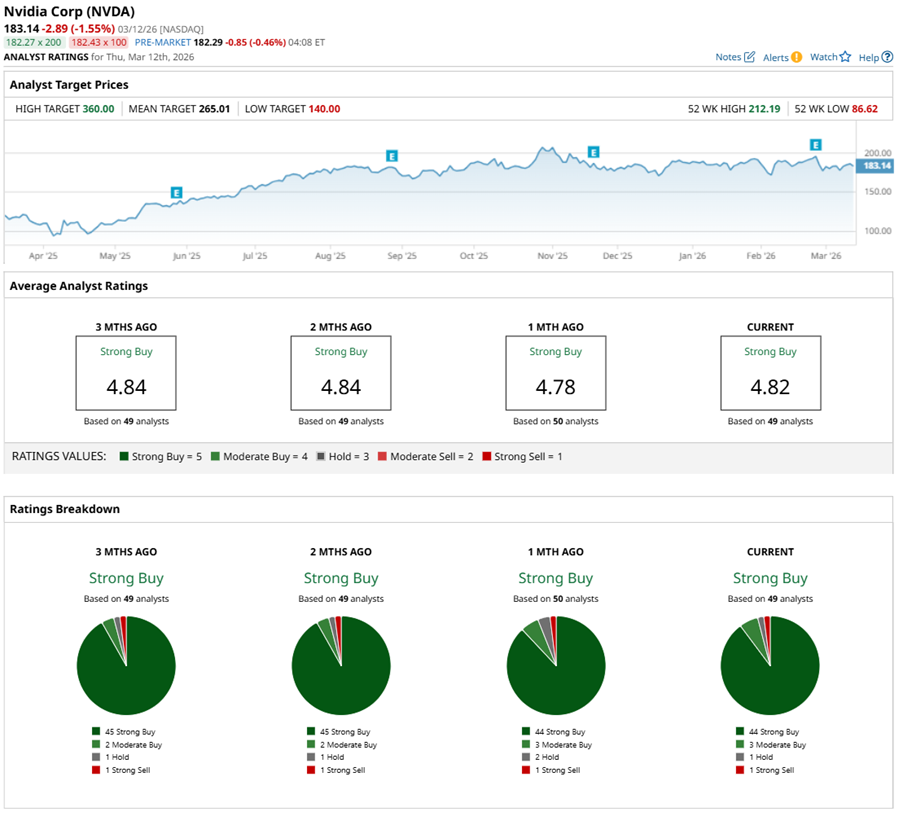

Overall, analysts are upbeat about NVDA’s growth potential, giving the stock a consensus rating of “Strong Buy.” Of the 49 analysts covering the stock, 44 advise a “Strong Buy,” while three suggest “Moderate Buy,” one advises a “Hold,” and only one suggests a “Strong Sell.”

The average analyst price target for NVDA is $265.01, indicating potential upside of 44.7%. The Street-high target price of $360 — set by Tigress Financial — suggests that the stock could rally as much as 96.6% from here.

Should You Buy the Dip in Advanced Micro Devices Stock?

Founded in 1969, Advanced Micro Devices has spent more than five decades pushing the boundaries of high-performance computing. Today, with a market capitalization of $322.4 billion, AMD is a global semiconductor powerhouse, fueling everything from gaming rigs to hyperscale data centers with its Instinct MI350 GPUs, designed for speed, efficiency, and broad accessibility.

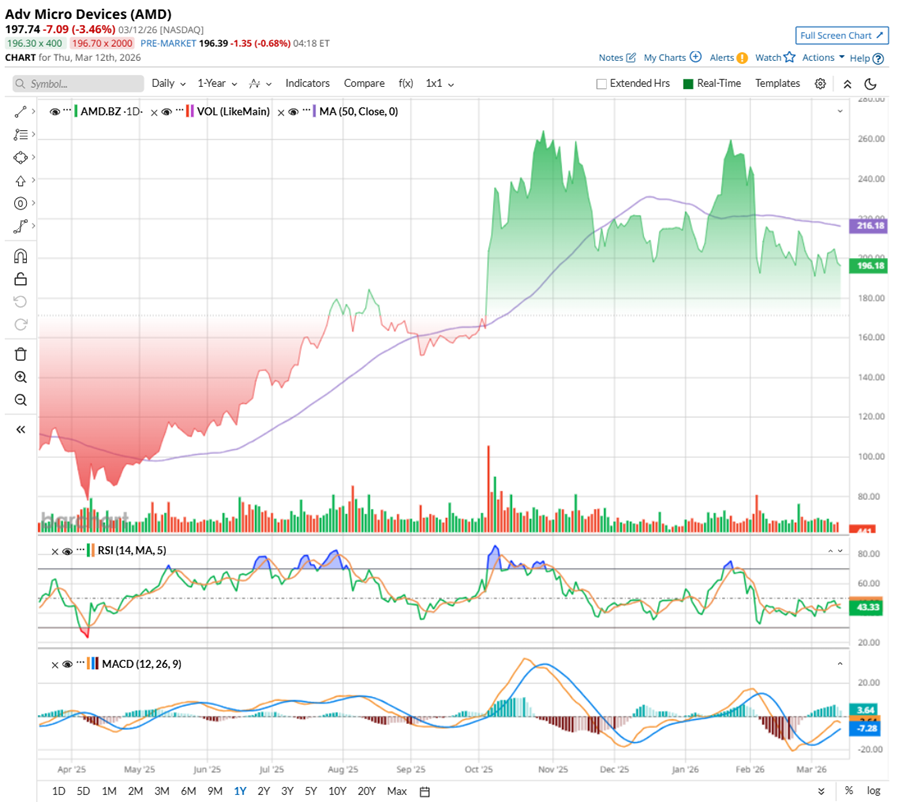

Considering that backdrop, AMD stock has delivered a remarkable run over the past decade. Over the past year, shares have surged about 102.7%, easily outpacing the broader market as excitement around AI chips and high-performance computing gathered pace. In the past six months, the stock climbed another 25.4%, supported by strong analyst sentiment and growing investor confidence. AMD eventually touched a high of $267.08 in October before pulling back roughly 25%, as traders locked in profits after the steep rally.

More recently, geopolitical tensions shaking global oil markets have added fresh nerves to the semiconductor sector, dragging AMD slightly lower. The stock is now trading below its 50-day moving average, signaling softer short-term momentum.

Technically, AMD’s chart suggests the stock may simply be taking a breather. Volume has tilted toward the red in recent sessions, while the 14-day RSI has cooled to around 43 from January’s overbought levels. AMD’s consolidation could simply be a pause before the next potential move higher.

When it comes to valuation, Advanced Micro Devices is not exactly cheap, priced at around 29.8x forward adjusted earnings and 6.9x sales. That’s richer than many peers, but still below its own historical averages. Investors are clearly betting on AMD’s growing role in the AI chip race. If the company keeps delivering strong double-digit revenue and earnings growth, today’s premium valuation could start looking far more reasonable in the coming years.

AMD's Latest Earnings Report

Advanced Micro Devices delivered its stronger-than-expected fourth-quarter report on Feb. 3, generating record revenue of $10.27 billion, up 34% year-over-year, comfortably surging past Wall Street’s expectations. The biggest engine behind that growth was the data center business, where revenue climbed to about $5.38 billion, a solid 39% annual jump as demand for high-performance computing and AI infrastructure kept rising.

But the momentum was not limited to just one segment. AMD’s client and gaming divisions also joined the rally, each posting roughly 37% annual growth. That broad-based expansion suggests the company’s recovery is becoming more balanced, rather than relying on a single product line.

Meanwhile, non-GAAP gross margin expanded to 57%, a sign that AMD is benefiting from a richer product mix and better operating leverage. Earnings reflected that strength as well, with non-GAAP EPS coming in at $1.53, up more than 40% year-over-year and beating Wall Street expectations.

Cash flow added another layer of confidence. FCF reached roughly $2.1 billion, nearly doubling from the previous year and pushing AMD’s cash and short-term investments to about $10.6 billion by the end of the quarter.

Management described 2025 as a defining year. The company is stepping up investments in R&D and infrastructure, with capital expenditures rising to around $974 million.

The near-term outlook is measured but steady. For Q1 2026, AMD guided revenue to about $9.8 billion, plus or minus $300 million, suggesting a modest 5% sequential dip but roughly 32% annual growth. Gross margin is expected to be near 55%. Management acknowledged a double-digit decline in semi-custom SoC sales as the console cycle cools, but that softness is expected to be offset over time by rising AI momentum, with demand for new Instinct MI450 GPUs anticipated to build later in 2026.

What Wall Street Says About AMD Stock

Meanwhile, analysts tracking AMD expect Q1 EPS to come in around $1.03, up 32.1% year-over-year. Looking further ahead, profit is anticipated to jump nearly 72.5% to $5.64 per share in fiscal 2026 and surge another 59.8% in 2027 to $9.01 per share.

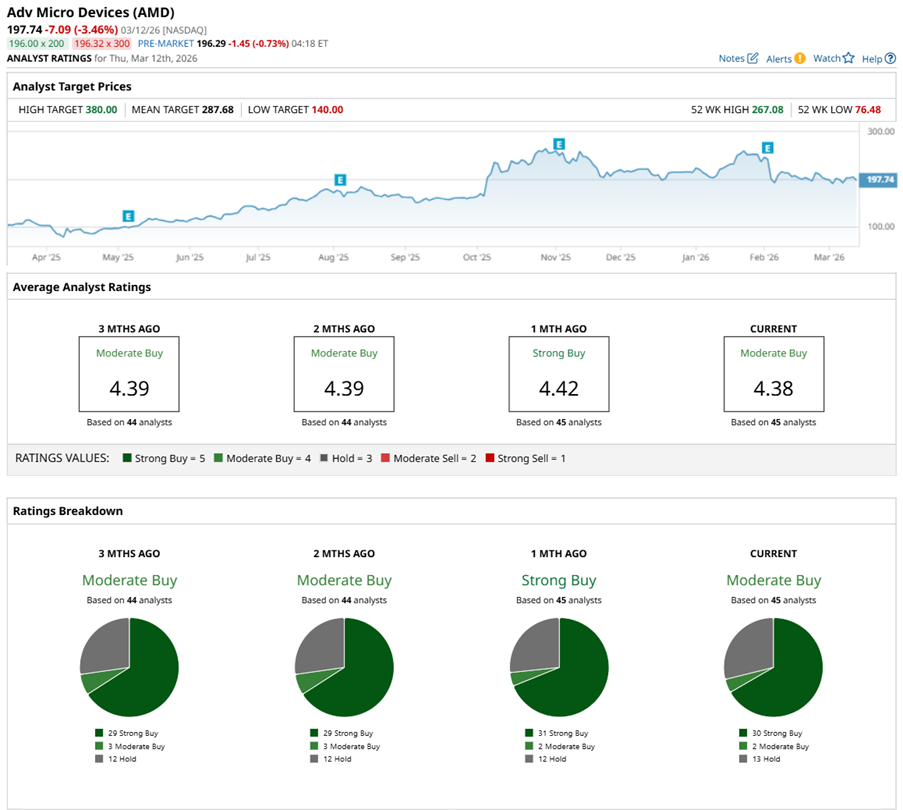

The stock has a “Moderate Buy” consensus rating. Among the 45 analysts monitoring the stock, 30 have issued a “Strong Buy,” two offer a “Moderate Buy,” and 13 advise to “Hold.” The average analyst price target of $287.68 suggests upside potential of 45.5%. The Street-high target of $380 suggests that the chip stock can still rally as much as 92.2% from current levels.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- Oil Supply Disruptions Are Rocking Chip Stocks Like Nvidia or AMD, But Should You Buy the Dip?

- Turn Omega Healthcare into an Income Machine with This Options Play

- Stocks Set to Open Higher as Bond Yields Fall, Fed Meeting and Middle East Conflict in Focus

- Iran War, Fed Conundrum and Other Key Things to Watch this Week