With a market cap of $29.4 billion, Expedia Group, Inc. (EXPE) is a global online travel company that operates across the United States and international markets, offering a wide range of travel products and services. The company organizes its business into three main segments: B2C; B2B; and trivago.

Companies valued more than $10 billion are generally classified as “large-cap” stocks, and Expedia Group fits this criterion perfectly. Through its platforms, Expedia Group supports lodging, flights, alternative accommodations, and travel-related services while leveraging marketing channels like mobile apps, loyalty programs, and social media.

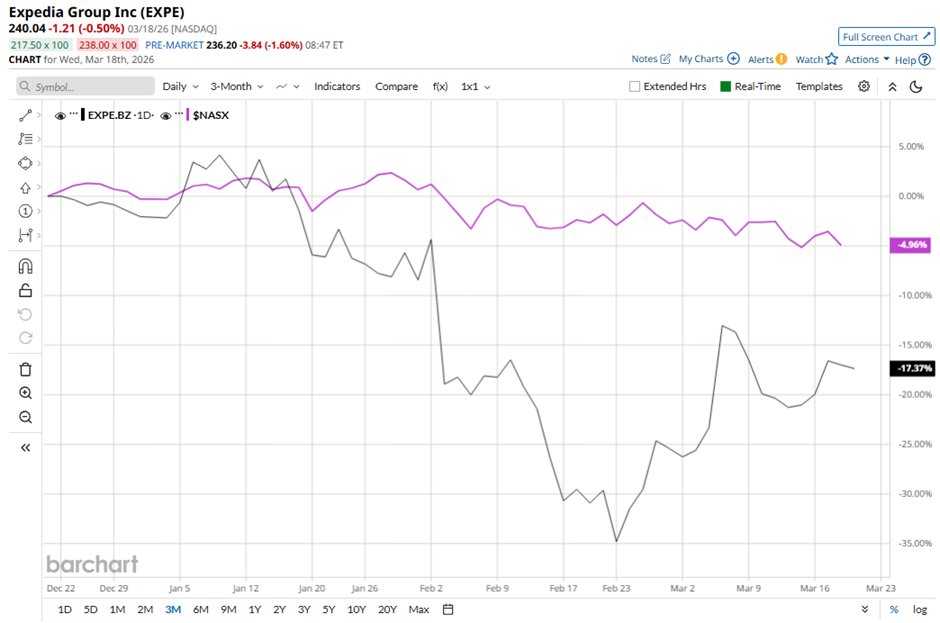

Shares of the Seattle, Washington-based company have declined 20% from its 52-week high of $303.80. EXPE stock has decreased 18.2% over the past three months, underperforming the Nasdaq Composite’s ($NASX) nearly 5% drop over the same time frame.

The stock has dipped 16.5% on a YTD basis, lagging behind NASX’s 4.7% decline. However, shares of Expedia Group have surged 37.2% over the past 52 weeks, outpacing NASX’s 24.8% return over the same time frame.

Yet, the stock has been trading below its 50-day moving average since late January.

Expedia Group shares tumbled 6.4% following its Q4 2025 results on Feb. 12 as investors focused on its cautious 2026 outlook amid macro uncertainty and uneven consumer spending. The company expects full-year adjusted core profit margin growth of only 1 - 1.25 percentage points, down from 2.4 percentage points in 2025, even though Q1 2026 margins are projected to rise 3 - 4 points. Despite stronger-than-expected Q4 adjusted EPS of $3.78 and revenue of $3.54 billion, net income declined 31% to $205 million and EPS fell 27% to $1.60.

In comparison, rival Travel + Leisure Co. (TNL) has outpaced EXPE stock. TNL stock has fallen marginally on a YTD basis and soared 50.4% over the past 52 weeks.

Despite the stock’s underperformance on a YTD basis, analysts remain moderately optimistic about its prospects. EXPE stock has a consensus rating of “Moderate Buy” from the 36 analysts in coverage, and the mean price target of $275.20 is a premium of 14.6% to current levels.

On the date of publication, Sohini Mondal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

- The Bears Are Losing the Battle Over Oracle, According to This Analyst. Should You Buy the Dip in ORCL Stock Here?

- Looking for Safety and Yield as Oil Prices Whip Saw? This Stock Has You Covered.

- Worse Than 2008? Google Searches for ‘Can’t Sell My House’ Just Hit an All-Time High

- Fuel for Growth or Red Flag: What Does a $4 Billion Debt Offering Really Mean for Nebius Stock?