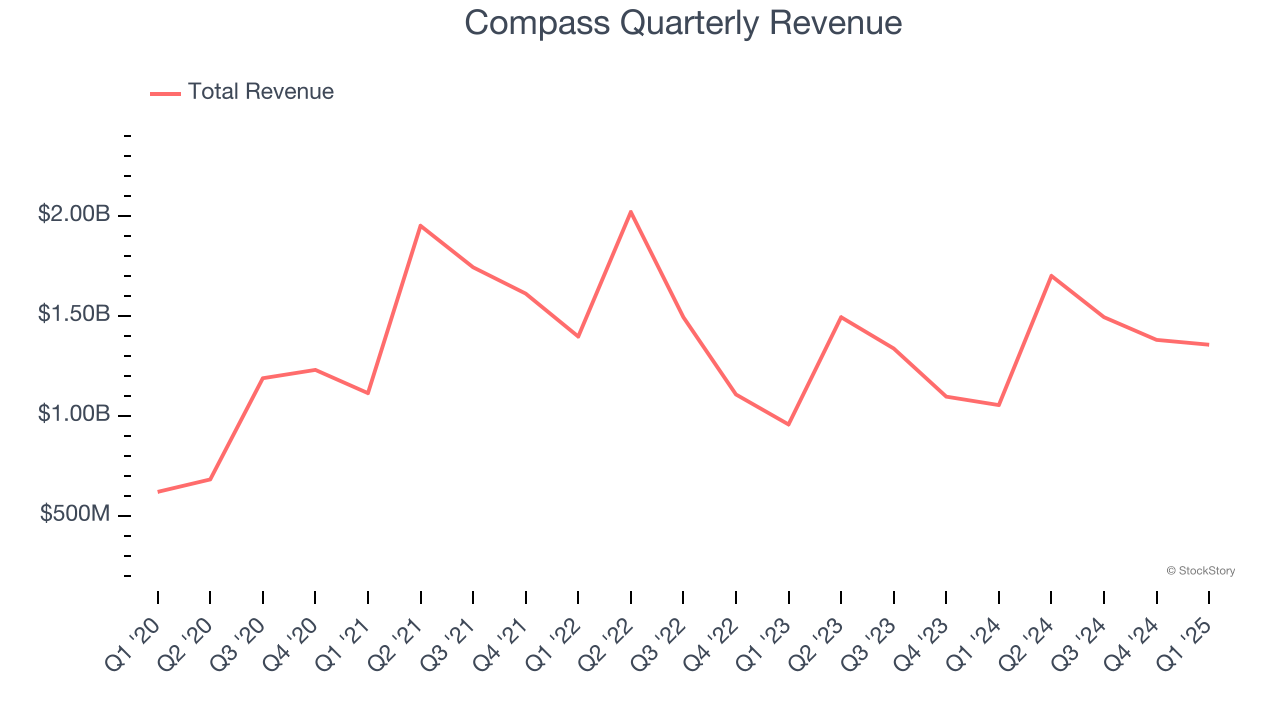

Real estate technology company Compass (NYSE: COMP) missed Wall Street’s revenue expectations in Q1 CY2025, but sales rose 28.7% year on year to $1.36 billion. Next quarter’s revenue guidance of $2.08 billion underwhelmed, coming in 1.5% below analysts’ estimates. Its non-GAAP loss of $0.09 per share was significantly below analysts’ consensus estimates.

Is now the time to buy Compass? Find out by accessing our full research report, it’s free.

Compass (COMP) Q1 CY2025 Highlights:

- Revenue: $1.36 billion vs analyst estimates of $1.42 billion (28.7% year-on-year growth, 4.6% miss)

- Adjusted EPS: -$0.09 vs analyst estimates of $0.02 (significant miss)

- Adjusted EBITDA: $15.6 million vs analyst estimates of $20.47 million (1.2% margin, 23.8% miss)

- Revenue Guidance for Q2 CY2025 is $2.08 billion at the midpoint, below analyst estimates of $2.11 billion

- EBITDA guidance for Q2 CY2025 is $125 million at the midpoint, below analyst estimates of $126.9 million

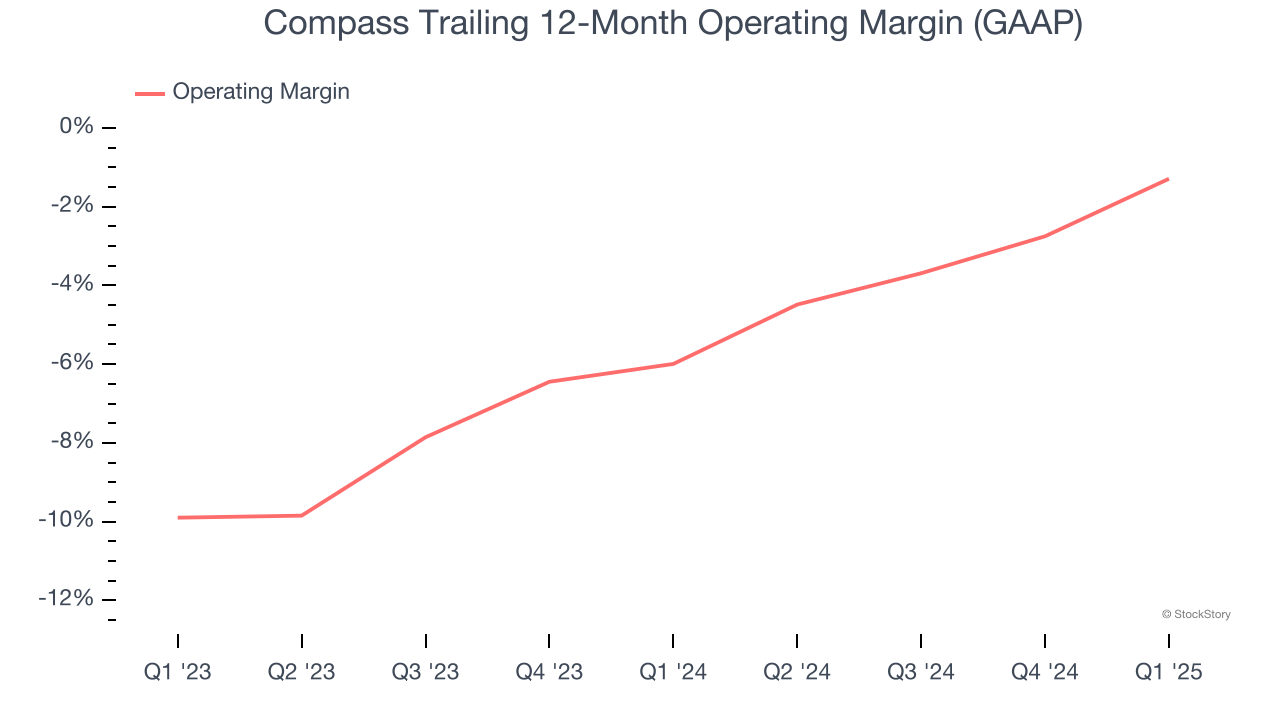

- Operating Margin: -4%, up from -12.5% in the same quarter last year

- Free Cash Flow Margin: 1.4%, similar to the same quarter last year

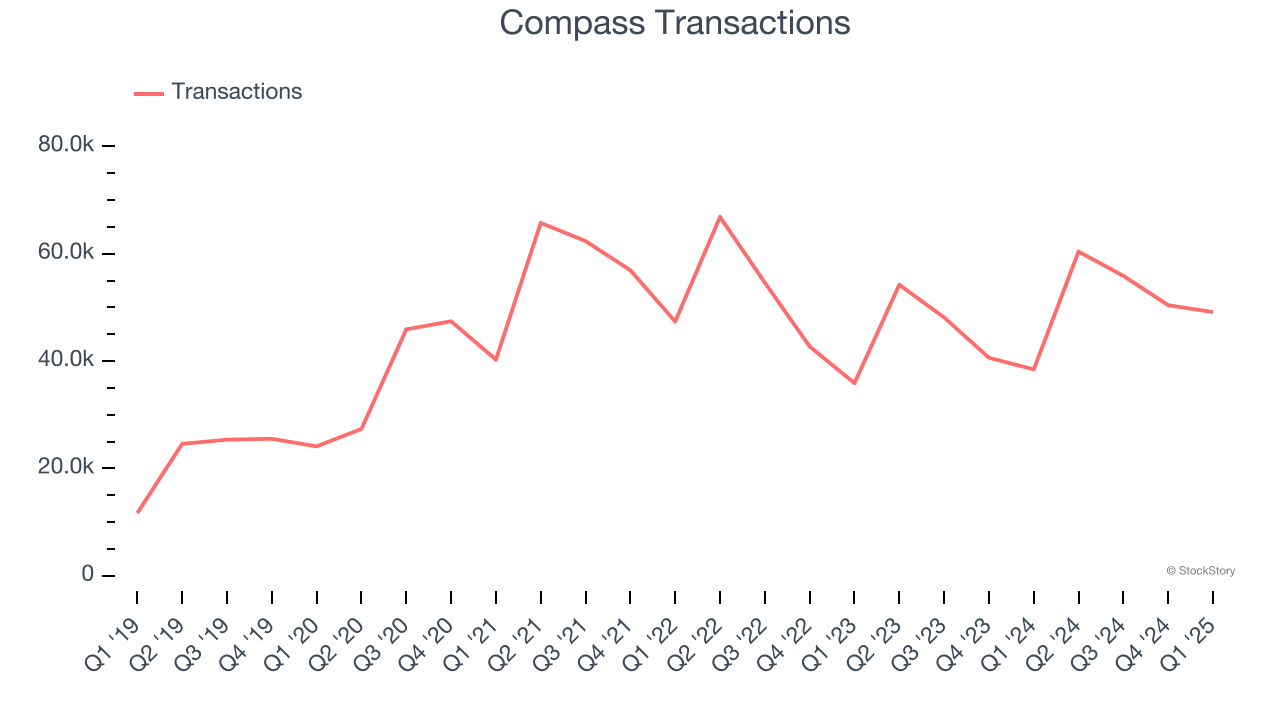

- Transactions: 49,121, up 10,672 year on year

- Market Capitalization: $3.97 billion

"Despite the heightened market volatility in Q1, Compass achieved record Q1 free cash flow, record Q1 Adjusted EBITDA2 and grew revenue by 28.7% year-over-year," said Robert Reffkin, Founder and Chief Executive Officer of Compass.

Company Overview

Fueled by its mission to replace the "paper-driven, antiquated workflow" of buying a house, Compass (NYSE: COMP) is a digital-first company operating a residential real estate brokerage in the United States.

Sales Growth

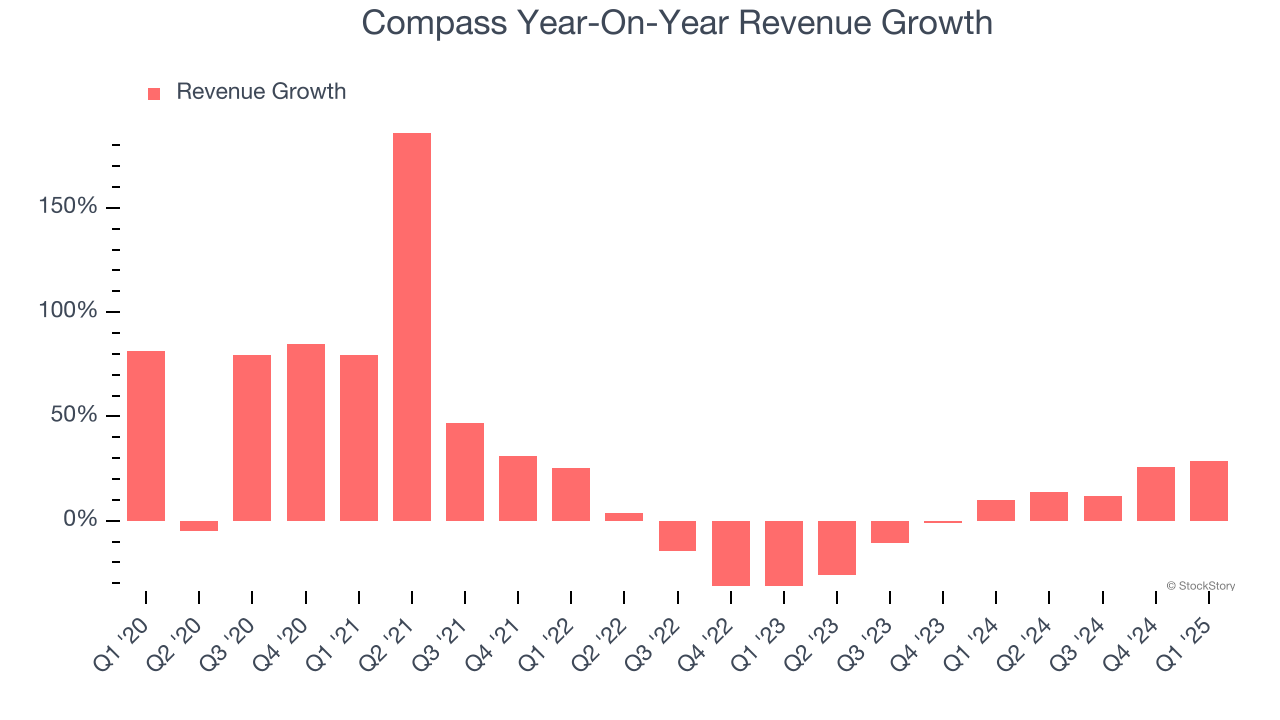

A company’s long-term sales performance is one signal of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Compass grew its sales at a decent 17.4% compounded annual growth rate. Its growth was slightly above the average consumer discretionary company and shows its offerings resonate with customers.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Compass’s recent performance shows its demand has slowed as its annualized revenue growth of 3.1% over the last two years was below its five-year trend.

We can dig further into the company’s revenue dynamics by analyzing its number of transactions, which reached 49,121 in the latest quarter. Over the last two years, Compass’s transactions averaged 6.4% year-on-year growth. Because this number is higher than its revenue growth during the same period, we can see the company’s monetization has fallen.

This quarter, Compass generated an excellent 28.7% year-on-year revenue growth rate, but its $1.36 billion of revenue fell short of Wall Street’s high expectations. Company management is currently guiding for a 22% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 23.2% over the next 12 months, an improvement versus the last two years. This projection is admirable and indicates its newer products and services will catalyze better top-line performance.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Compass’s operating margin has risen over the last 12 months, but it still averaged negative 3.4% over the last two years. This is due to its large expense base and inefficient cost structure.

This quarter, Compass generated a negative 4% operating margin. The company's consistent lack of profits raise a flag.

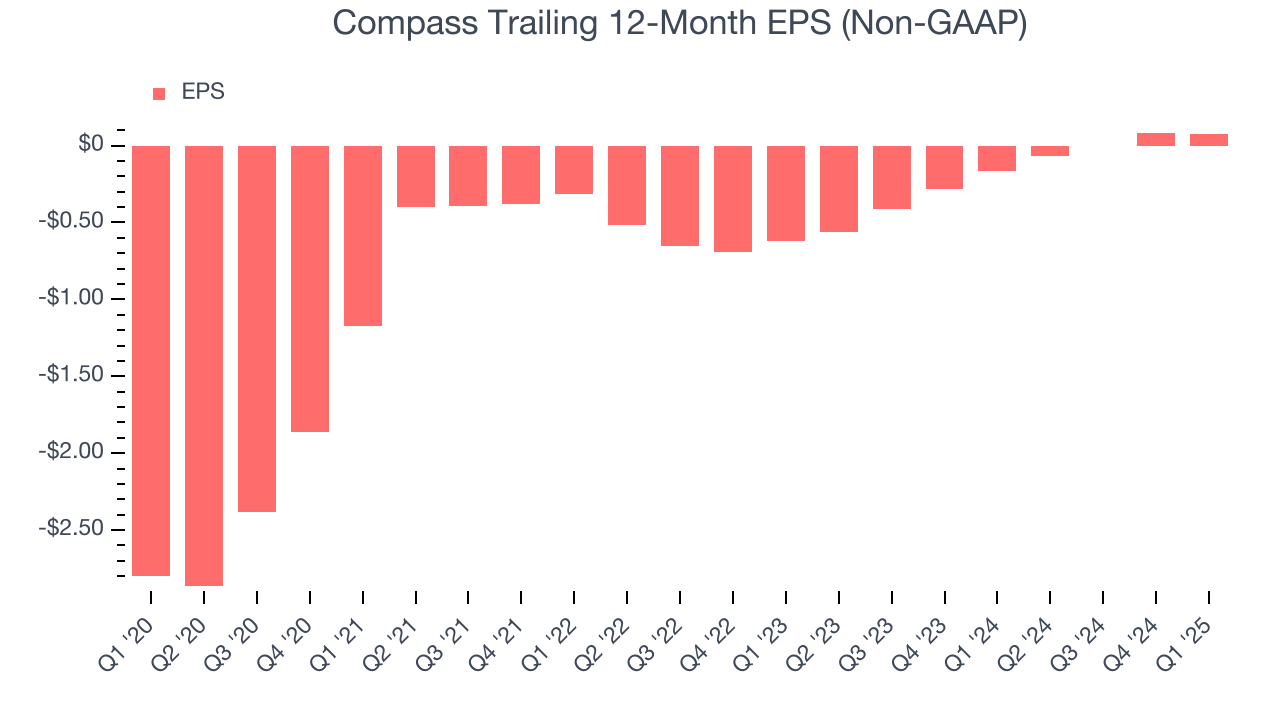

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Compass’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

In Q1, Compass reported EPS at negative $0.09, in line with the same quarter last year. This print missed analysts’ estimates, but we care more about long-term EPS growth than short-term movements. Over the next 12 months, Wall Street expects Compass to perform poorly. Analysts forecast its full-year EPS of $0.08 will hit $0.44.

Key Takeaways from Compass’s Q1 Results

We struggled to find many positives in these results. Its number of transactions missed and its revenue fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock remained flat at $7.73 immediately after reporting.

So do we think Compass is an attractive buy at the current price? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.