Since December 2024, Casella Waste Systems has been in a holding pattern, posting a small return of 3.4% while floating around $115.93. However, the stock is beating the S&P 500’s 1.9% decline during that period.

Is there a buying opportunity in Casella Waste Systems, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Casella Waste Systems Not Exciting?

Despite the relative momentum, we're swiping left on Casella Waste Systems for now. Here are three reasons why CWST doesn't excite us and a stock we'd rather own.

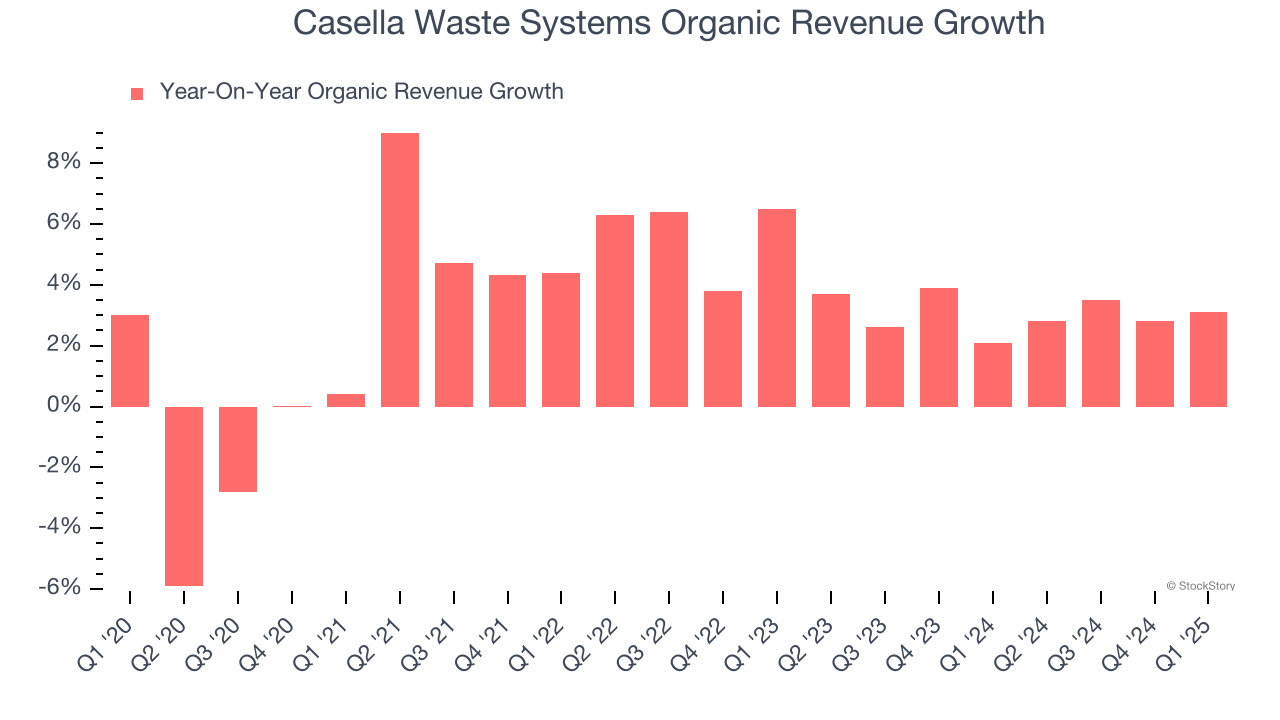

1. Slow Organic Growth Suggests Waning Demand In Core Business

We can better understand Waste Management companies by analyzing their organic revenue. This metric gives visibility into Casella Waste Systems’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, Casella Waste Systems’s organic revenue averaged 3.1% year-on-year growth. This performance was underwhelming and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

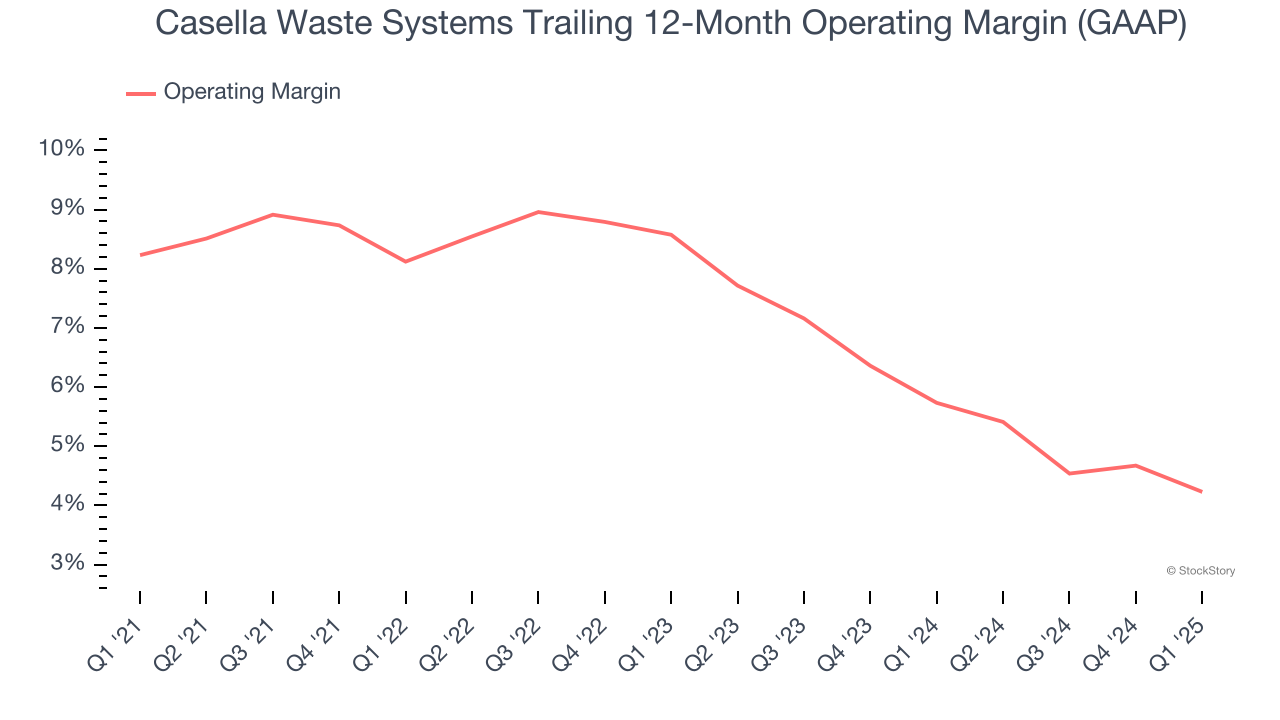

2. Shrinking Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Looking at the trend in its profitability, Casella Waste Systems’s operating margin decreased by 4 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Casella Waste Systems’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers. Its operating margin for the trailing 12 months was 4.2%.

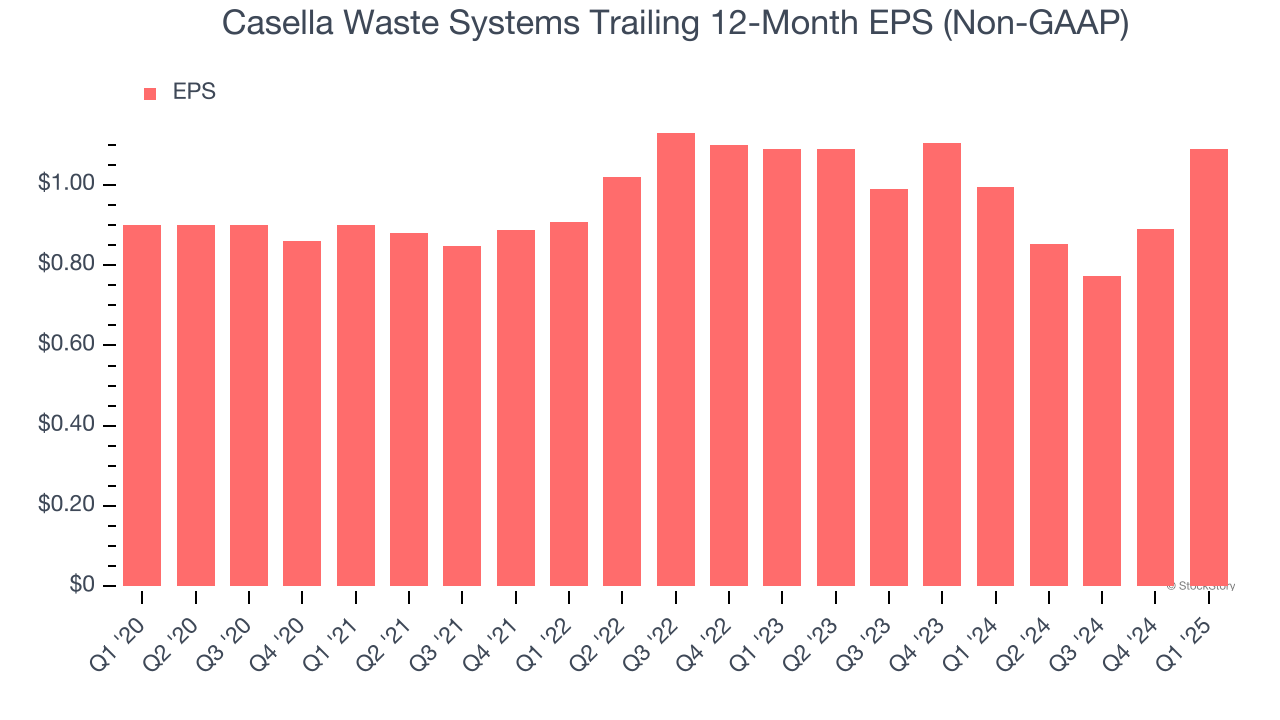

3. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Casella Waste Systems’s EPS grew at a weak 3.9% compounded annual growth rate over the last five years, lower than its 16.5% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Casella Waste Systems’s business quality ultimately falls short of our standards. Following its recent outperformance in a weaker market environment, the stock trades at 96.1× forward P/E (or $115.93 per share). This valuation tells us a lot of optimism is priced in - we think there are better opportunities elsewhere. Let us point you toward a safe-and-steady industrials business benefiting from an upgrade cycle.

High-Quality Stocks for All Market Conditions

Donald Trump’s victory in the 2024 U.S. Presidential Election sent major indices to all-time highs, but stocks have retraced as investors debate the health of the economy and the potential impact of tariffs.

While this leaves much uncertainty around 2025, a few companies are poised for long-term gains regardless of the political or macroeconomic climate, like our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.