Over the past six months, TriCo Bancshares’s stock price fell to $41.01. Shareholders have lost 6% of their capital, which is disappointing considering the S&P 500 has climbed by 6.4%. This might have investors contemplating their next move.

Is there a buying opportunity in TriCo Bancshares, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is TriCo Bancshares Not Exciting?

Even with the cheaper entry price, we're swiping left on TriCo Bancshares for now. Here are three reasons why TCBK doesn't excite us and a stock we'd rather own.

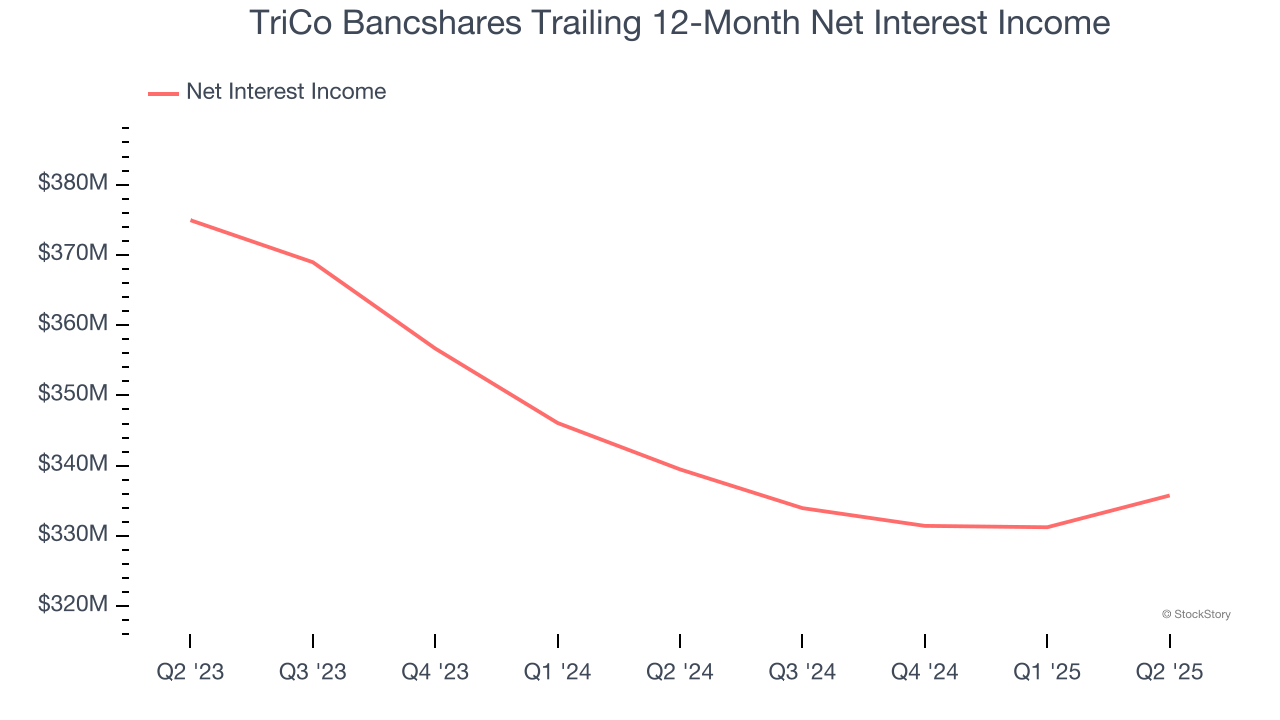

1. Net Interest Income Points to Soft Demand

Our experience and research show the market cares primarily about a bank’s net interest income growth as one-time fees are considered a lower-quality and non-recurring revenue source.

TriCo Bancshares’s net interest income has grown at a 5.7% annualized rate over the last five years, worse than the broader banking industry and in line with its total revenue.

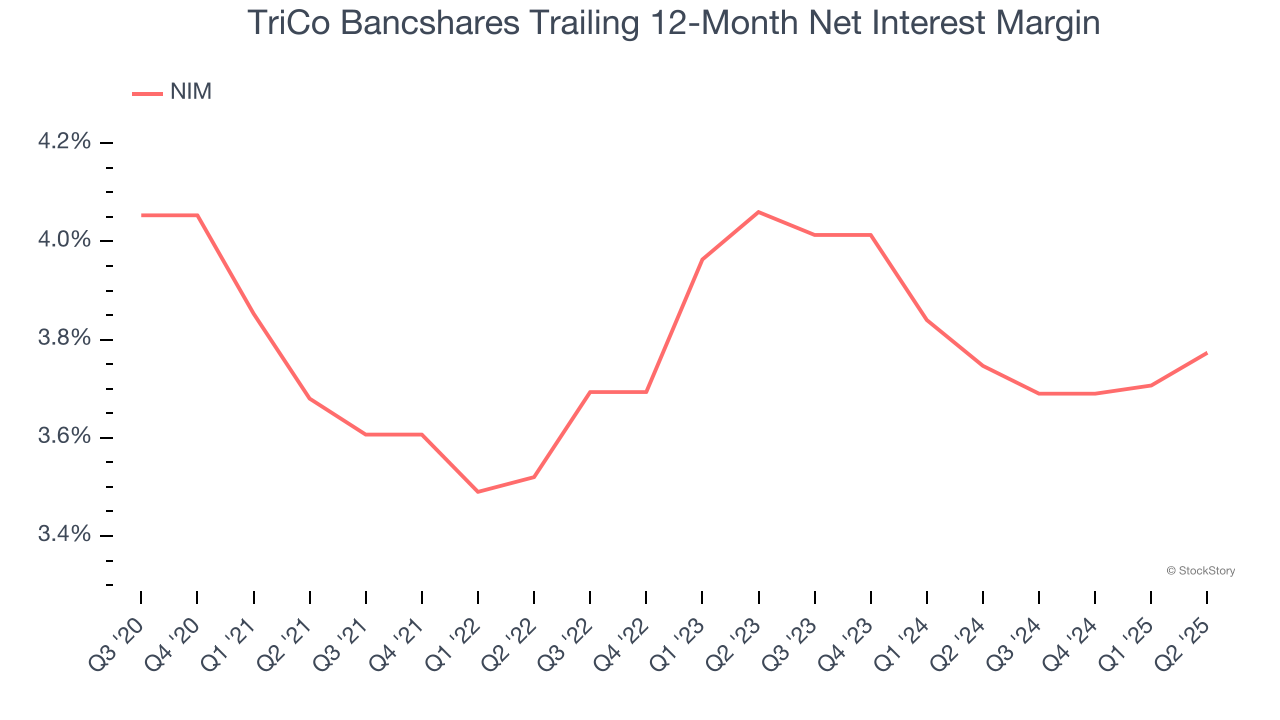

2. Net Interest Margin Dropping

Net interest margin (NIM) serves as a critical gauge of a bank's fundamental profitability by showing the spread between interest income and interest expenses. It's essential for understanding whether a firm can sustainably generate returns from its lending operations.

Over the past two years, TriCo Bancshares’s net interest margin averaged 3.8%. However, its margin contracted by 28.7 basis points (100 basis points = 1 percentage point) over that period.

This decline was a headwind for its net interest income. While prevailing rates are a major determinant of net interest margin changes over time, the decline could mean TriCo Bancshares either faced competition for loans and deposits or experienced a negative mix shift in its balance sheet composition.

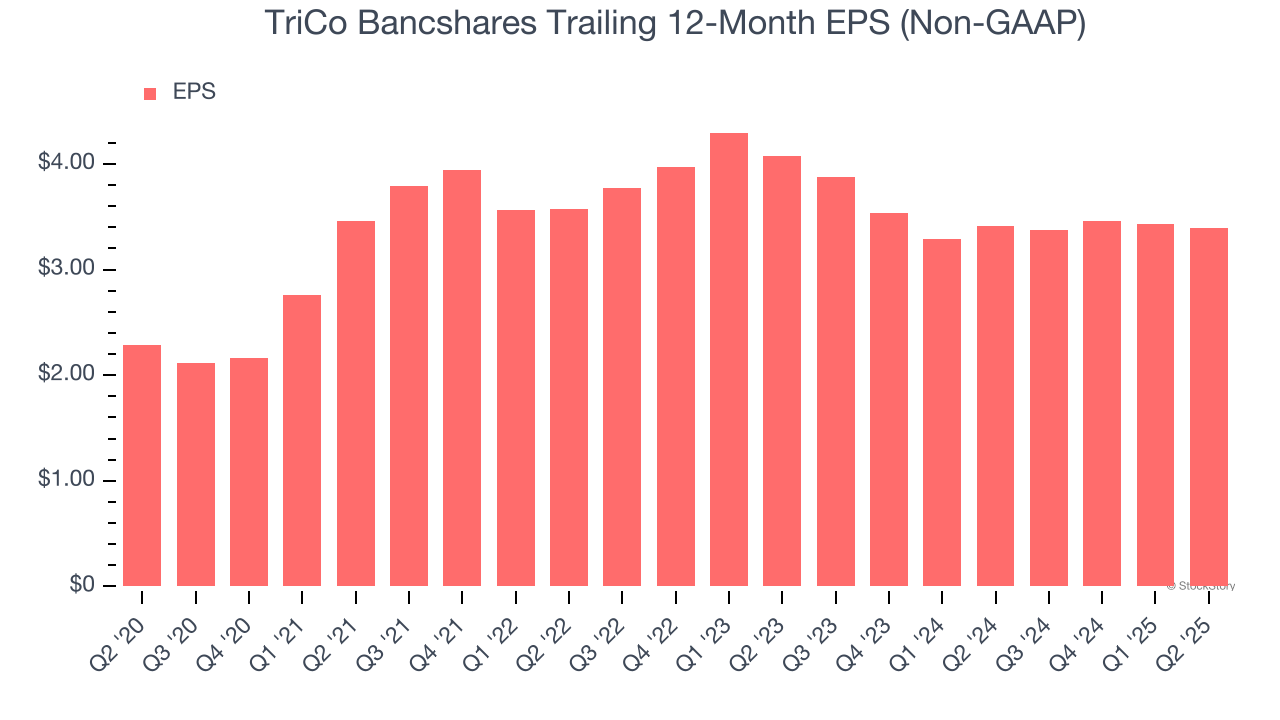

3. EPS Took a Dip Over the Last Two Years

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for TriCo Bancshares, its EPS declined by more than its revenue over the last two years, dropping 8.7%. This tells us the company struggled to adjust to shrinking demand.

Final Judgment

TriCo Bancshares’s business quality ultimately falls short of our standards. Following the recent decline, the stock trades at 1.1× forward P/B (or $41.01 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better opportunities elsewhere. Let us point you toward one of our top software and edge computing picks.

High-Quality Stocks for All Market Conditions

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.