As the Q2 earnings season wraps, let’s dig into this quarter’s best and worst performers in the travel and vacation providers industry, including Sabre (NASDAQ: SABR) and its peers.

Airlines, hotels, resorts, and cruise line companies often sell experiences rather than tangible products, and in the last decade-plus, consumers have slowly shifted from buying "things" (wasteful) to buying "experiences" (memorable). In addition, the internet has introduced new ways of approaching leisure and lodging such as booking homes and longer-term accommodations. Traditional airlines, hotel, resorts, and cruise line companies must innovate to stay relevant in a market rife with innovation.

The 18 travel and vacation providers stocks we track reported a mixed Q2. As a group, revenues beat analysts’ consensus estimates by 1.1% while next quarter’s revenue guidance was in line.

In light of this news, share prices of the companies have held steady as they are up 1.1% on average since the latest earnings results.

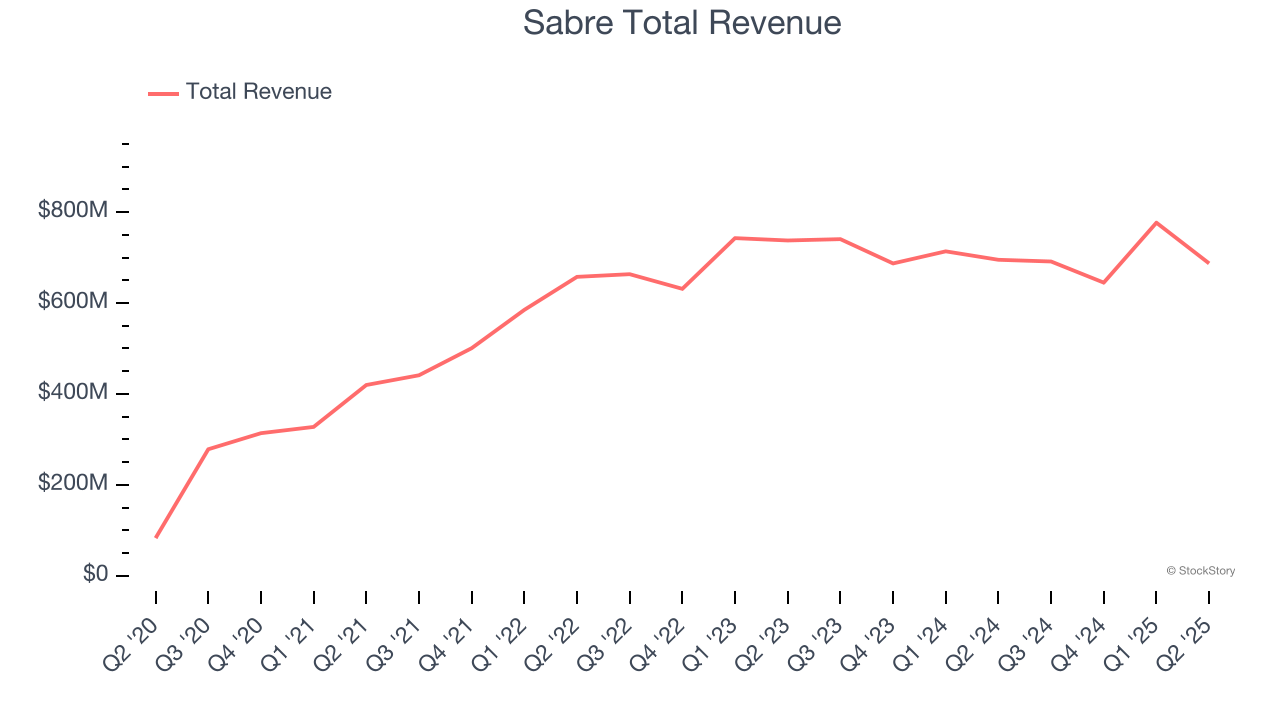

Sabre (NASDAQ: SABR)

Originally a division of American Airlines, Sabre (NASDAQ: SABR) is a technology provider for the global travel and tourism industry.

Sabre reported revenues of $687.1 million, down 1.1% year on year. This print fell short of analysts’ expectations by 7%. Overall, it was a disappointing quarter for the company with full-year EBITDA guidance missing analysts’ expectations significantly and .

Unsurprisingly, the stock is down 40.5% since reporting and currently trades at $1.79.

Read our full report on Sabre here, it’s free.

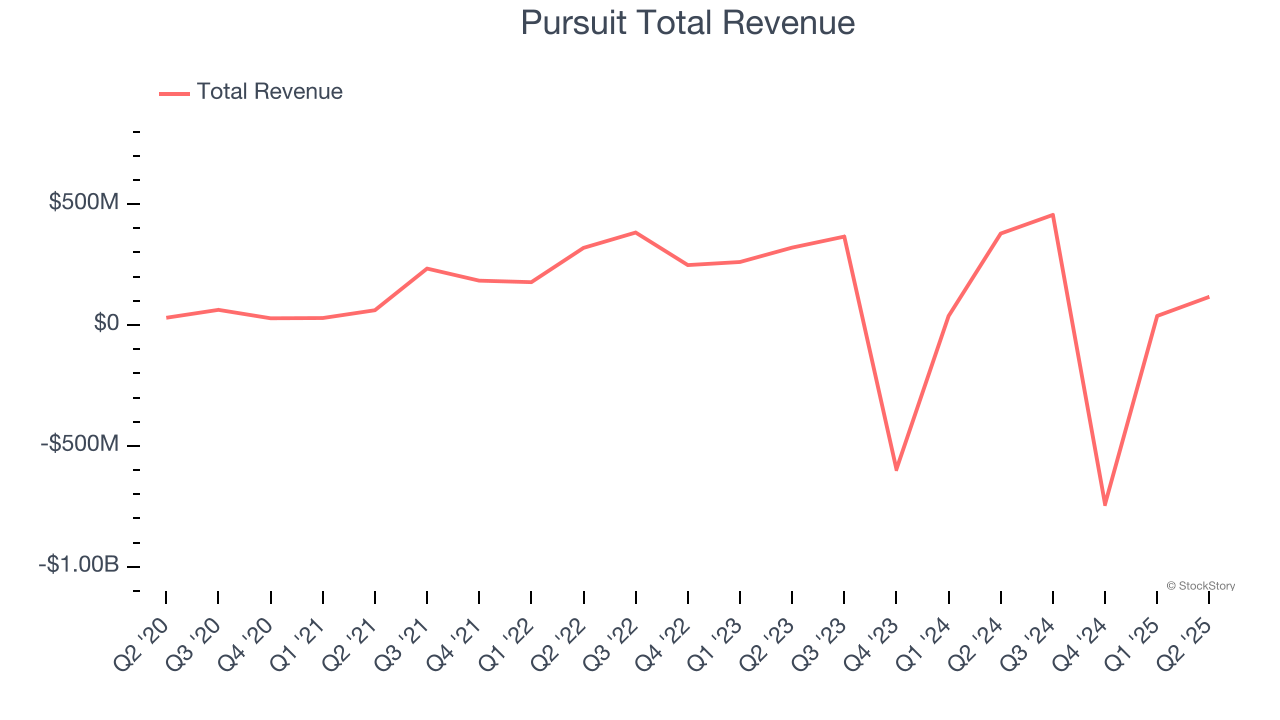

Best Q2: Pursuit (NYSE: PRSU)

With attractions ranging from glacier tours in the Canadian Rockies to an oceanfront geothermal lagoon in Iceland, Pursuit Attractions and Hospitality (NYSE: PRSU) operates iconic travel experiences, experiential marketing services, and exhibition management across North America and Europe.

Pursuit reported revenues of $116.7 million, down 69.2% year on year, outperforming analysts’ expectations by 6.9%. The business had a stunning quarter with a beat of analysts’ EPS estimates and full-year EBITDA guidance exceeding analysts’ expectations.

The market seems happy with the results as the stock is up 21.9% since reporting. It currently trades at $36.60.

Is now the time to buy Pursuit? Access our full analysis of the earnings results here, it’s free.

Weakest Q2: Hilton Grand Vacations (NYSE: HGV)

Spun off from Hilton Worldwide in 2017, Hilton Grand Vacations (NYSE: HGV) is a global timeshare company that provides travel experiences for its customers through its timeshare resorts and club membership programs.

Hilton Grand Vacations reported revenues of $1.27 billion, up 2.5% year on year, falling short of analysts’ expectations by 8.1%. It was a disappointing quarter as it posted a significant miss of analysts’ adjusted operating income estimates.

Hilton Grand Vacations delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 15.3% since the results and currently trades at $43.02.

Read our full analysis of Hilton Grand Vacations’s results here.

Target Hospitality (NASDAQ: TH)

Building mini-communities at places such as oil drilling sites, Target Hospitality (NASDAQ: TH) is a provider of specialty workforce lodging accommodations and services.

Target Hospitality reported revenues of $61.61 million, down 38.8% year on year. This print beat analysts’ expectations by 9.2%. Zooming out, it was a mixed quarter as it also produced full-year revenue guidance exceeding analysts’ expectations but a significant miss of analysts’ EBITDA estimates.

Target Hospitality delivered the biggest analyst estimates beat and highest full-year guidance raise among its peers. The stock is up 20.4% since reporting and currently trades at $8.79.

Read our full, actionable report on Target Hospitality here, it’s free.

Wyndham (NYSE: WH)

Established in 1981, Wyndham (NYSE: WH) is a global hotel franchising company with over 9,000 hotels across nearly 95 countries on six continents.

Wyndham reported revenues of $397 million, up 8.2% year on year. This result surpassed analysts’ expectations by 2.5%. Aside from that, it was a satisfactory quarter as it also recorded a beat of analysts’ EPS estimates but a slight miss of analysts’ adjusted operating income estimates.

The stock is down 5.4% since reporting and currently trades at $81.46.

Read our full, actionable report on Wyndham here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.