Since September 2020, the S&P 500 has delivered a total return of 94.2%. But one standout stock has nearly doubled the market - over the past five years, Texas Capital Bank has surged 175% to $86.52 per share. Its momentum hasn’t stopped as it’s also gained 20.6% in the last six months thanks to its solid quarterly results, beating the S&P by 5.1%.

Is now the time to buy Texas Capital Bank, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Texas Capital Bank Not Exciting?

We’re glad investors have benefited from the price increase, but we're sitting this one out for now. Here are three reasons there are better opportunities than TCBI and a stock we'd rather own.

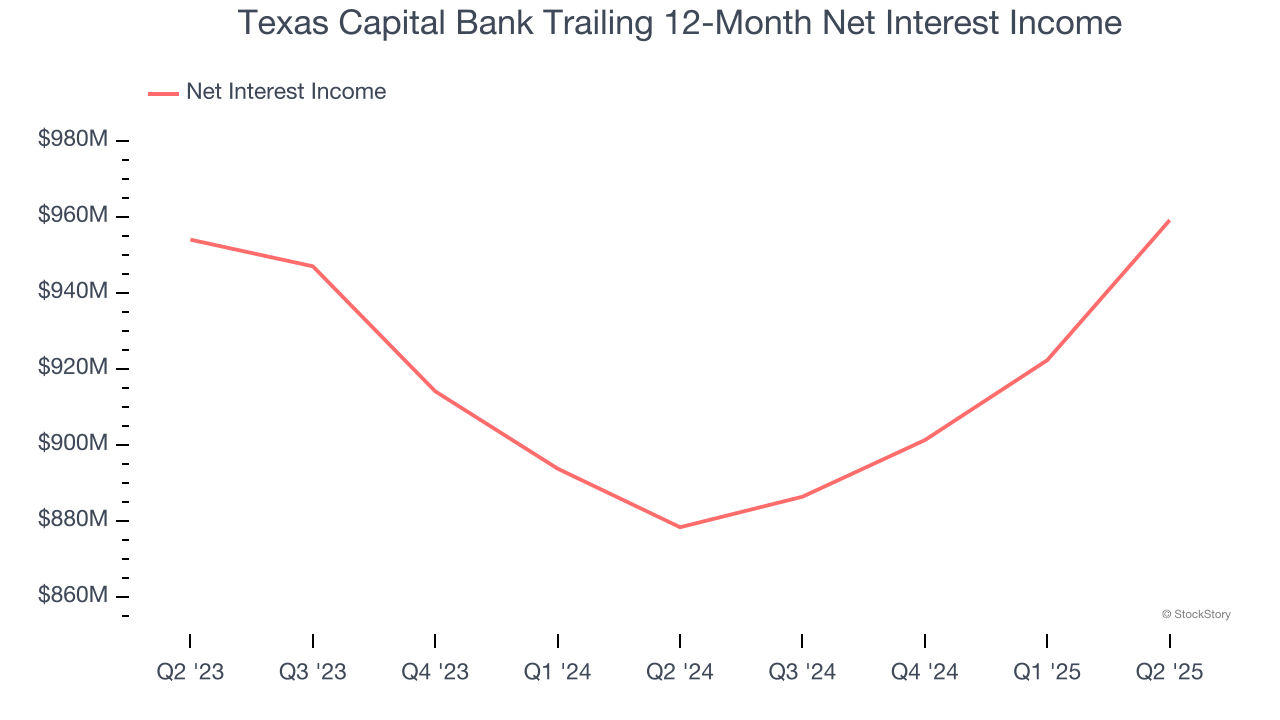

1. Net Interest Income Points to Soft Demand

Markets consistently prioritize net interest income over non-recurring fees, recognizing its superior quality compared to the more unpredictable revenue streams.

Texas Capital Bank’s net interest income has grown at a 2.2% annualized rate over the last five years, much worse than the broader banking industry and in line with its total revenue. Its growth was driven by an increase in its net interest margin, which represents how much a bank earns in relation to its outstanding loans, as its loan book shrank throughout that period.

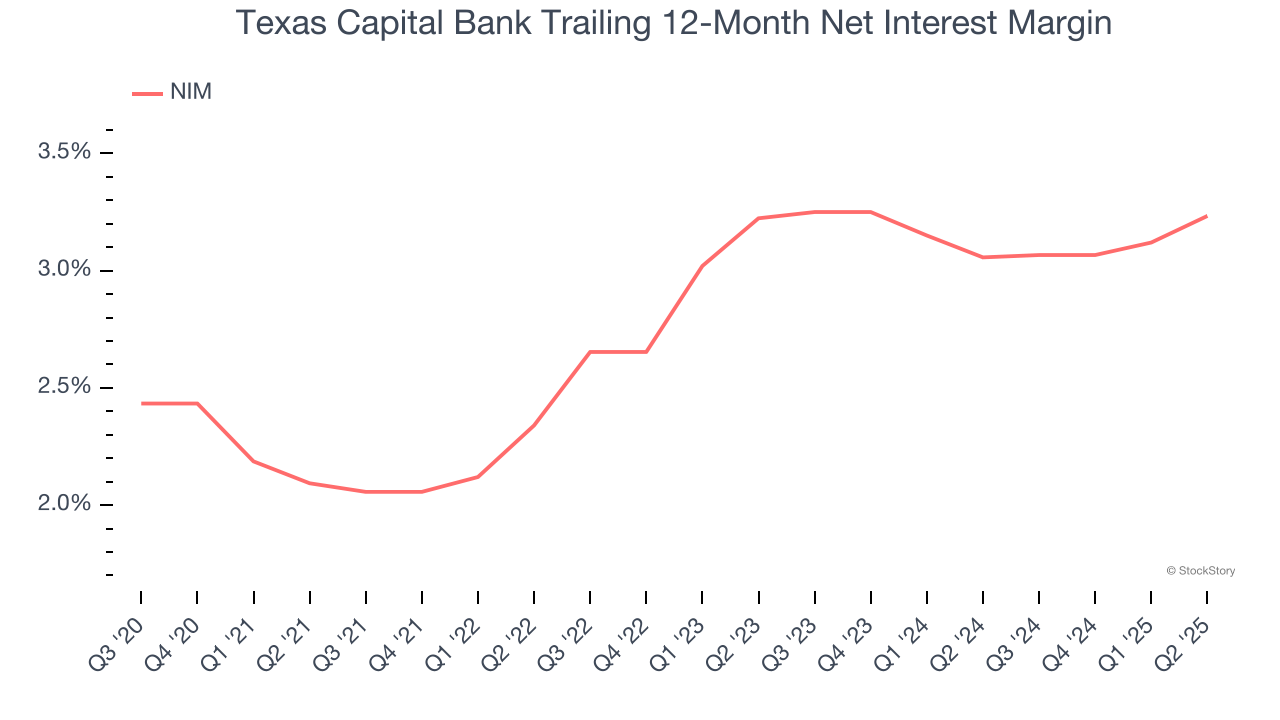

2. Low Net Interest Margin Reveals Weak Loan Book Profitability

Net interest margin (NIM) represents the unit economics of a bank by measuring the profitability of its interest-bearing assets relative to its interest-bearing liabilities. It's a fundamental metric that investors use to assess lending premiums and returns.

Over the past two years, we can see that Texas Capital Bank’s net interest margin averaged a subpar 3.1%, reflecting its high servicing and capital costs.

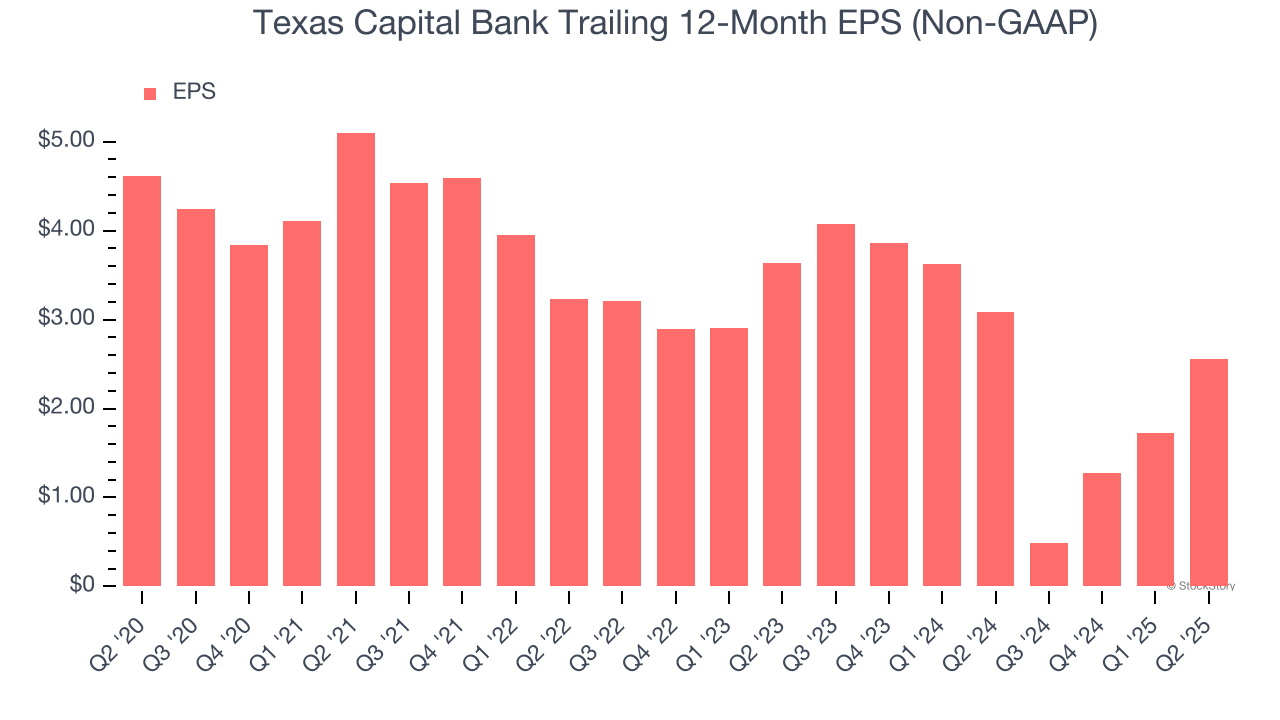

3. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Texas Capital Bank, its EPS declined by 11.1% annually over the last five years while its revenue grew by 2%. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Texas Capital Bank’s business quality ultimately falls short of our standards. With its shares beating the market recently, the stock trades at 1.2× forward P/B (or $86.52 per share). Investors with a higher risk tolerance might like the company, but we don’t really see a big opportunity at the moment. We're fairly confident there are better stocks to buy right now. We’d suggest looking at a top digital advertising platform riding the creator economy.

Stocks We Like More Than Texas Capital Bank

Donald Trump’s April 2025 "Liberation Day" tariffs sent markets into a tailspin, but stocks have since rebounded strongly, proving that knee-jerk reactions often create the best buying opportunities.

The smart money is already positioning for the next leg up. Don’t miss out on the recovery - check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 183% over the last five years (as of March 31st 2025).

Stocks that made our list in 2020 include now familiar names such as Nvidia (+1,545% between March 2020 and March 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.