Wrapping up Q2 earnings, we look at the numbers and key takeaways for the traditional fast food stocks, including Yum China (NYSE: YUMC) and its peers.

Traditional fast-food restaurants are renowned for their speed and convenience, boasting menus filled with familiar and budget-friendly items. Their reputations for on-the-go consumption make them favored destinations for individuals and families needing a quick meal. This class of restaurants, however, is fighting the perception that their meals are unhealthy and made with inferior ingredients, a battle that's especially relevant today given the consumers increasing focus on health and wellness.

The 13 traditional fast food stocks we track reported a satisfactory Q2. As a group, revenues beat analysts’ consensus estimates by 0.8%.

In light of this news, share prices of the companies have held steady as they are up 2.2% on average since the latest earnings results.

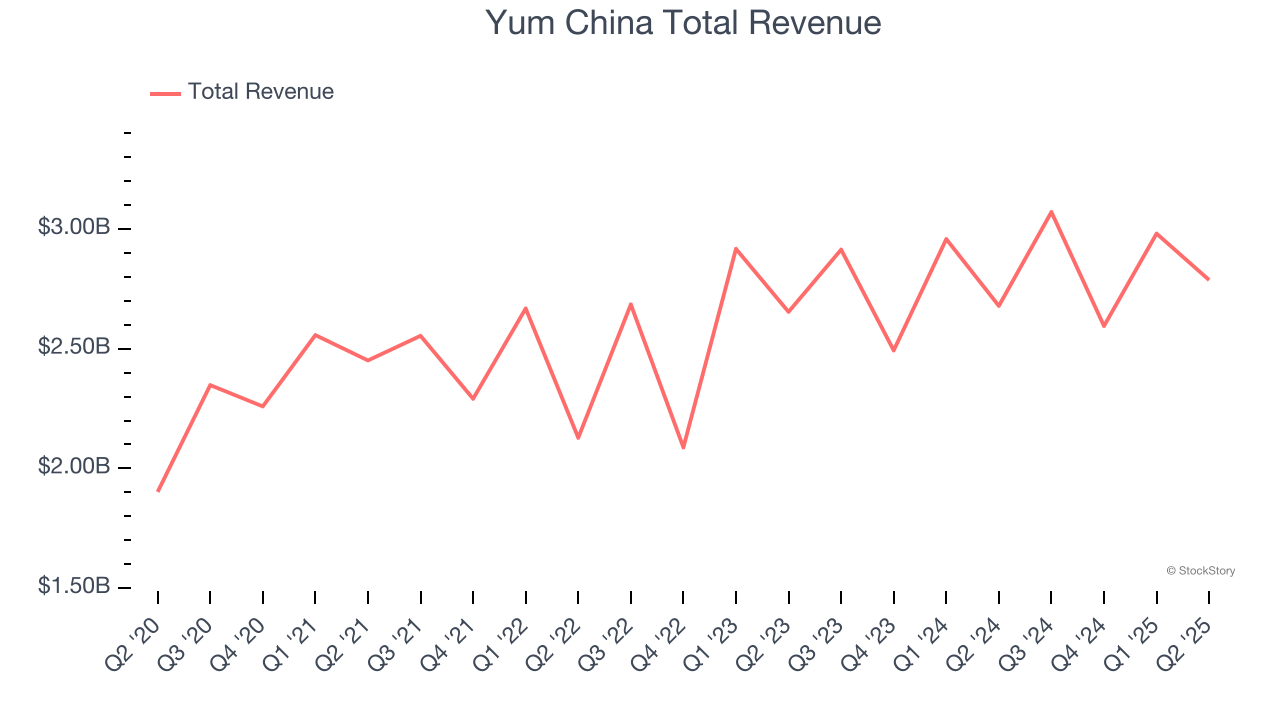

Yum China (NYSE: YUMC)

One of China’s largest restaurant companies, Yum China (NYSE: YUMC) is an independent entity spun off from Yum! Brands in 2016.

Yum China reported revenues of $2.79 billion, up 4% year on year. This print fell short of analysts’ expectations by 0.5%. Overall, it was a mixed quarter for the company with a narrow beat of analysts’ same-store sales estimates but EPS in line with analysts’ estimates.

Unsurprisingly, the stock is down 3.4% since reporting and currently trades at $44.93.

Is now the time to buy Yum China? Access our full analysis of the earnings results here, it’s free.

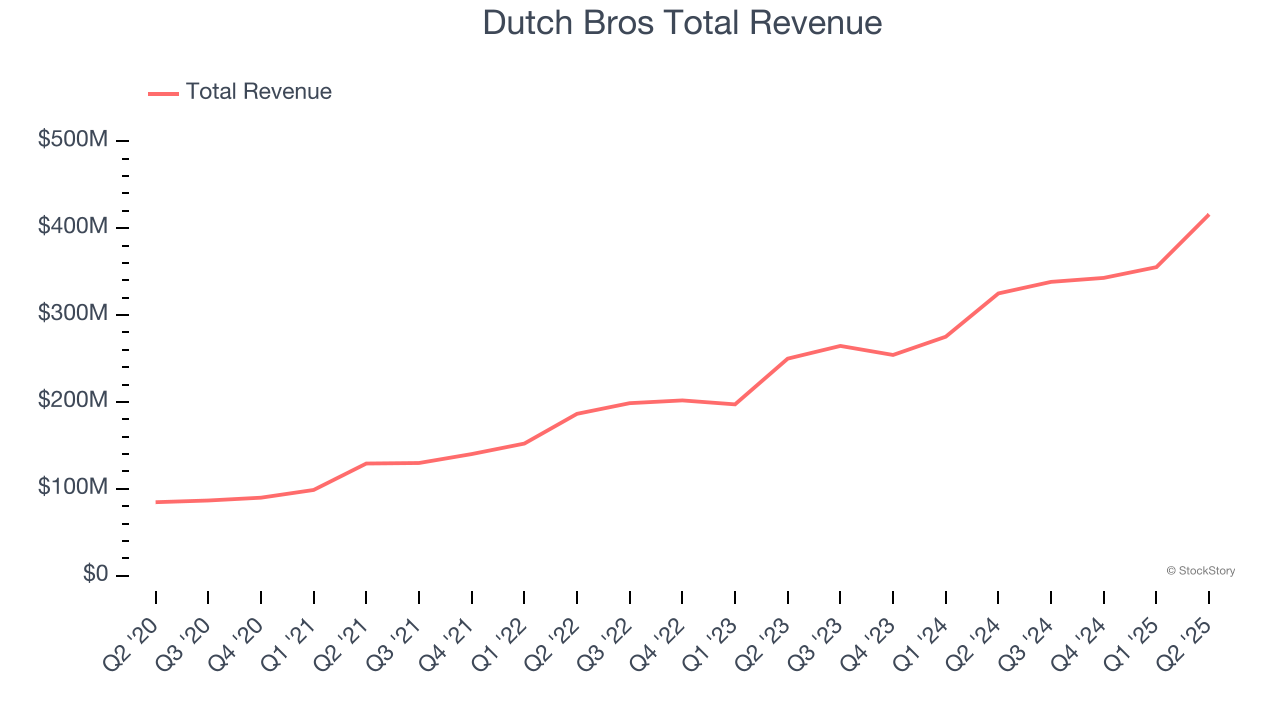

Best Q2: Dutch Bros (NYSE: BROS)

Started in 1992 by two brothers as a single pushcart, Dutch Bros (NYSE: BROS) is a dynamic coffee chain that’s captured the hearts of coffee enthusiasts across the United States.

Dutch Bros reported revenues of $415.8 million, up 28% year on year, outperforming analysts’ expectations by 3.1%. The business had a stunning quarter with an impressive beat of analysts’ EBITDA and same-store sales estimates.

Dutch Bros achieved the biggest analyst estimates beat and fastest revenue growth among its peers. The market seems happy with the results as the stock is up 14.4% since reporting. It currently trades at $66.12.

Is now the time to buy Dutch Bros? Access our full analysis of the earnings results here, it’s free.

Weakest Q2: Jack in the Box (NASDAQ: JACK)

Delighting customers since its inception in 1951, Jack in the Box (NASDAQ: JACK) is a distinctive fast-food chain known for its bold flavors, innovative menu items, and quirky marketing.

Jack in the Box reported revenues of $333 million, down 9.8% year on year, falling short of analysts’ expectations by 2.1%. It was a softer quarter as it posted a miss of analysts’ EBITDA and same-store sales estimates.

Jack in the Box delivered the weakest performance against analyst estimates in the group. Interestingly, the stock is up 8% since the results and currently trades at $20.44.

Read our full analysis of Jack in the Box’s results here.

Starbucks (NASDAQ: SBUX)

Started by three friends in Seattle’s historic Pike Place Market, Starbucks (NASDAQ: SBUX) is a globally-renowned coffeehouse chain that offers a wide selection of high-quality coffee, beverages, and food items.

Starbucks reported revenues of $9.46 billion, up 3.8% year on year. This result surpassed analysts’ expectations by 1.7%. More broadly, it was a slower quarter as it recorded a significant miss of analysts’ EBITDA estimates and a significant miss of analysts’ EPS estimates.

The stock is down 8% since reporting and currently trades at $85.50.

Read our full, actionable report on Starbucks here, it’s free.

Papa John's (NASDAQ: PZZA)

Founded by the eclectic John “Papa John” Schnatter, Papa John’s (NASDAQ: PZZA) is a globally recognized pizza delivery and carryout chain known for “better ingredients” and “better pizza”.

Papa John's reported revenues of $529.2 million, up 4.2% year on year. This number topped analysts’ expectations by 2.7%. Overall, it was a very strong quarter as it also produced an impressive beat of analysts’ same-store sales estimates and a beat of analysts’ EPS estimates.

The stock is up 18.5% since reporting and currently trades at $48.02.

Read our full, actionable report on Papa John's here, it’s free.

Market Update

Thanks to the Fed’s rate hikes in 2022 and 2023, inflation has been on a steady path downward, easing back toward that 2% sweet spot. Fortunately (miraculously to some), all this tightening didn’t send the economy tumbling into a recession, so here we are, cautiously celebrating a soft landing. The cherry on top? Recent rate cuts (half a point in September 2024, a quarter in November) have propped up markets, especially after Trump’s November win lit a fire under major indices and sent them to all-time highs. However, there’s still plenty to ponder — tariffs, corporate tax cuts, and what 2025 might hold for the economy.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.