Over the last six months, Performance Food Group’s shares have sunk to $94.21, producing a disappointing 5.3% loss - a stark contrast to the S&P 500’s 8.1% gain. This may have investors wondering how to approach the situation.

Is now the time to buy Performance Food Group, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Do We Think Performance Food Group Will Underperform?

Even though the stock has become cheaper, we don't have much confidence in Performance Food Group. Here are three reasons we avoid PFGC and a stock we'd rather own.

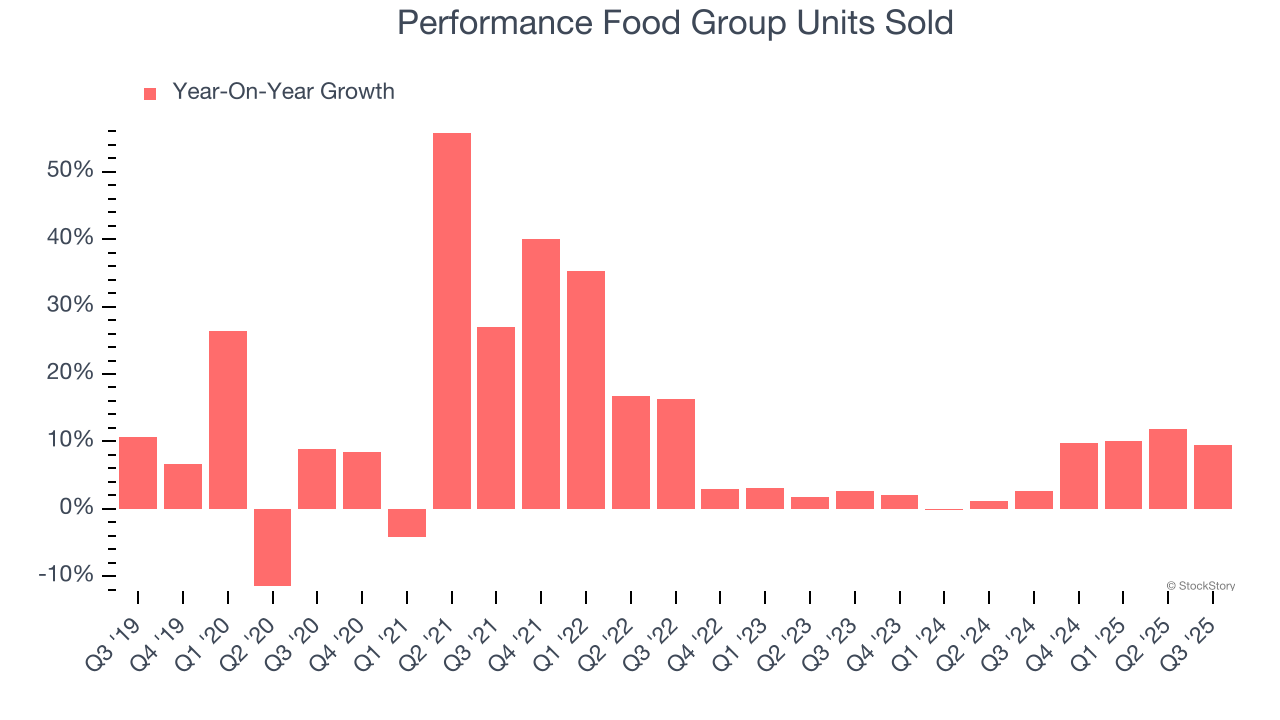

1. Weak Sales Volumes Indicate Waning Demand

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful Distributors company because there’s a ceiling to what customers will pay.

Over the last two years, Performance Food Group’s units sold averaged 5.8% year-on-year growth. This performance was underwhelming and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

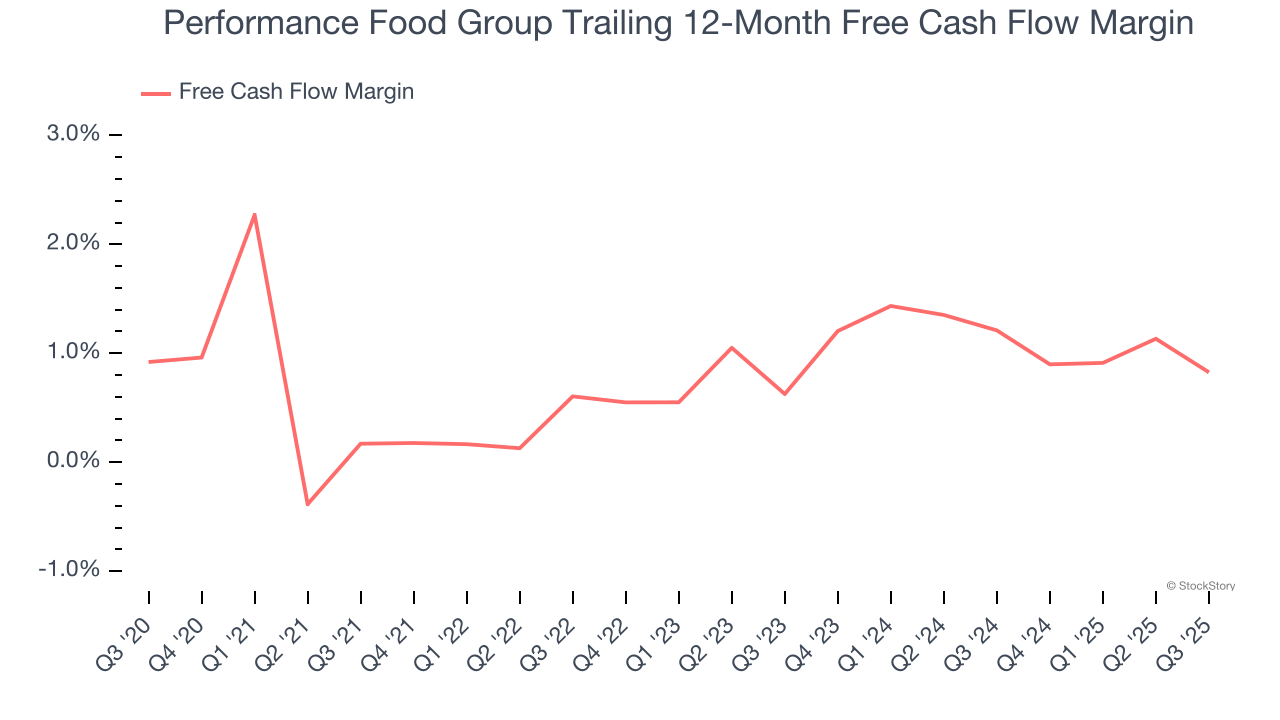

2. Mediocre Free Cash Flow Margin Limits Reinvestment Potential

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Performance Food Group has shown poor cash profitability over the last two years, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 1%, lousy for a consumer discretionary business.

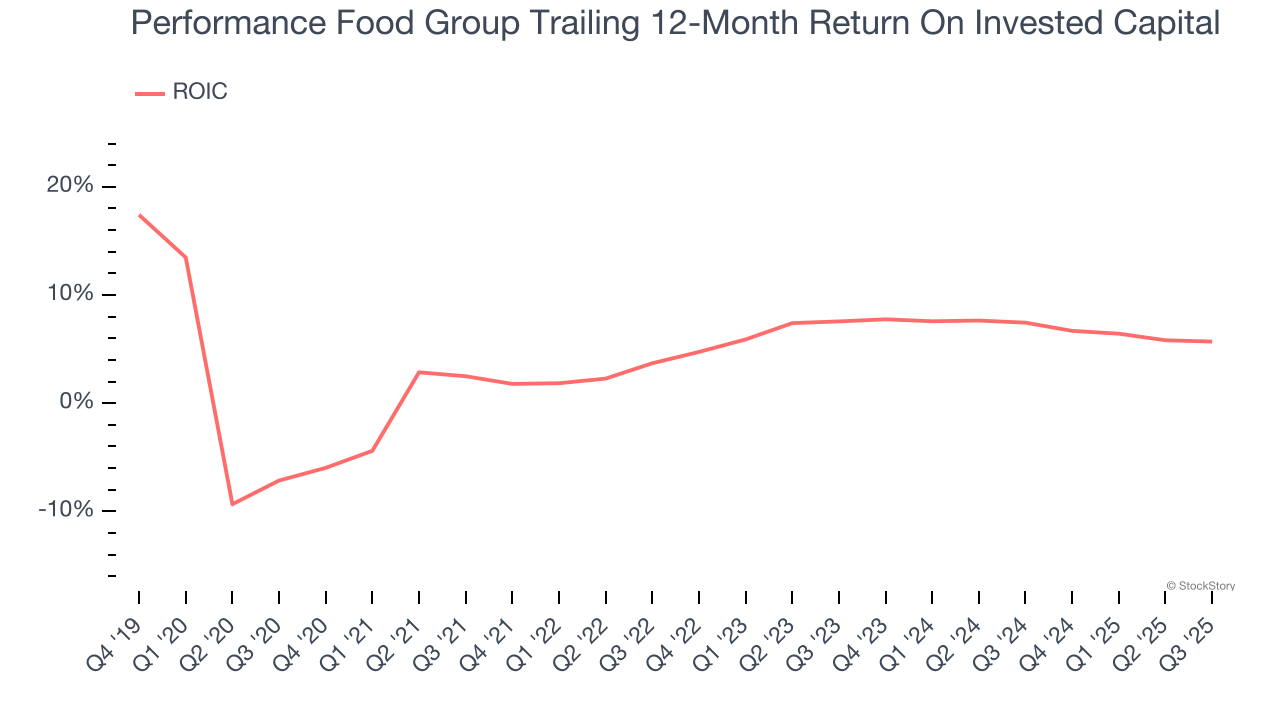

3. New Investments Bear Fruit as ROIC Jumps

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. On average, Performance Food Group’s ROIC increased by 3.5 percentage points annually over the last few years. This is a good sign, and we hope the company can continue improving.

Final Judgment

Performance Food Group doesn’t pass our quality test. Following the recent decline, the stock trades at 18.4× forward P/E (or $94.21 per share). This valuation tells us a lot of optimism is priced in - we think there are better stocks to buy right now. We’d suggest looking at the most entrenched endpoint security platform on the market.

Stocks We Like More Than Performance Food Group

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.