Over the past six months, Penske Automotive Group’s shares (currently trading at $160.42) have posted a disappointing 5.8% loss, well below the S&P 500’s 8.8% gain. This may have investors wondering how to approach the situation.

Is there a buying opportunity in Penske Automotive Group, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Penske Automotive Group Not Exciting?

Even with the cheaper entry price, we're cautious about Penske Automotive Group. Here are three reasons you should be careful with PAG and a stock we'd rather own.

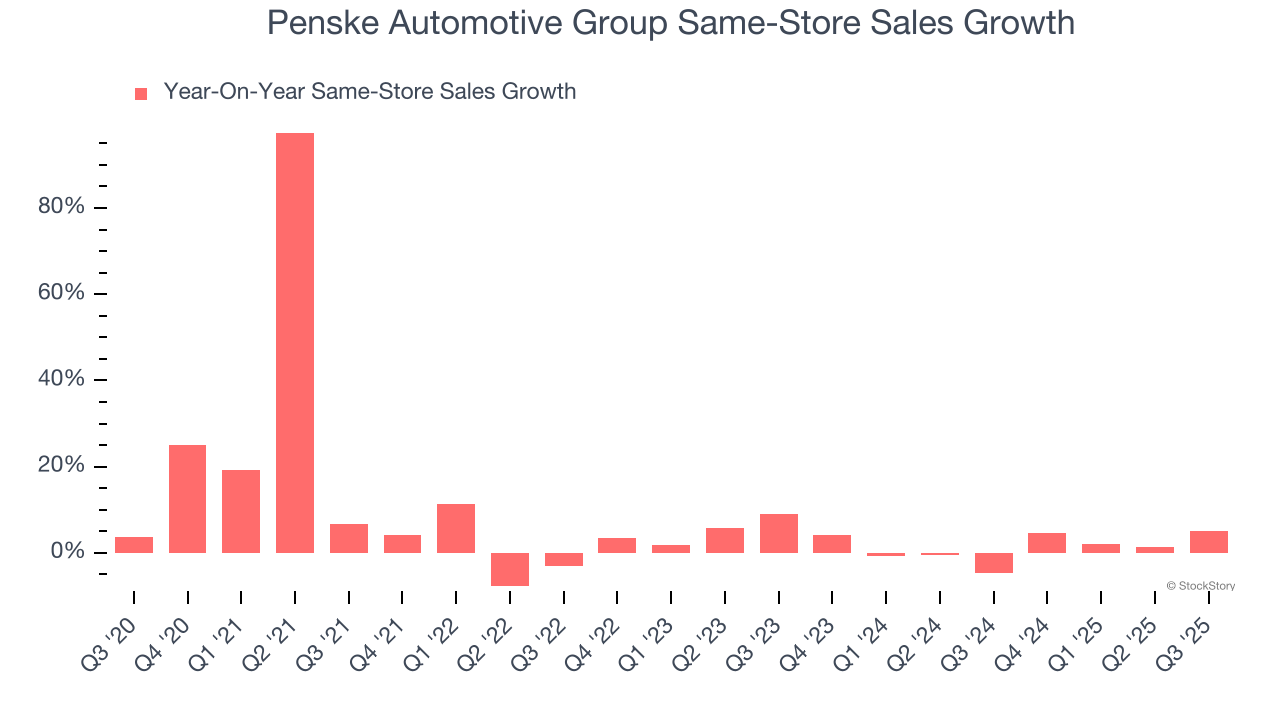

1. Same-Store Sales Falling Behind Peers

Same-store sales show the change in sales for a retailer's e-commerce platform and brick-and-mortar shops that have existed for at least a year. This is a key performance indicator because it measures organic growth.

Penske Automotive Group’s demand within its existing locations has been relatively stable over the last two years but was below most retailers. On average, the company’s same-store sales have grown by 1.4% per year.

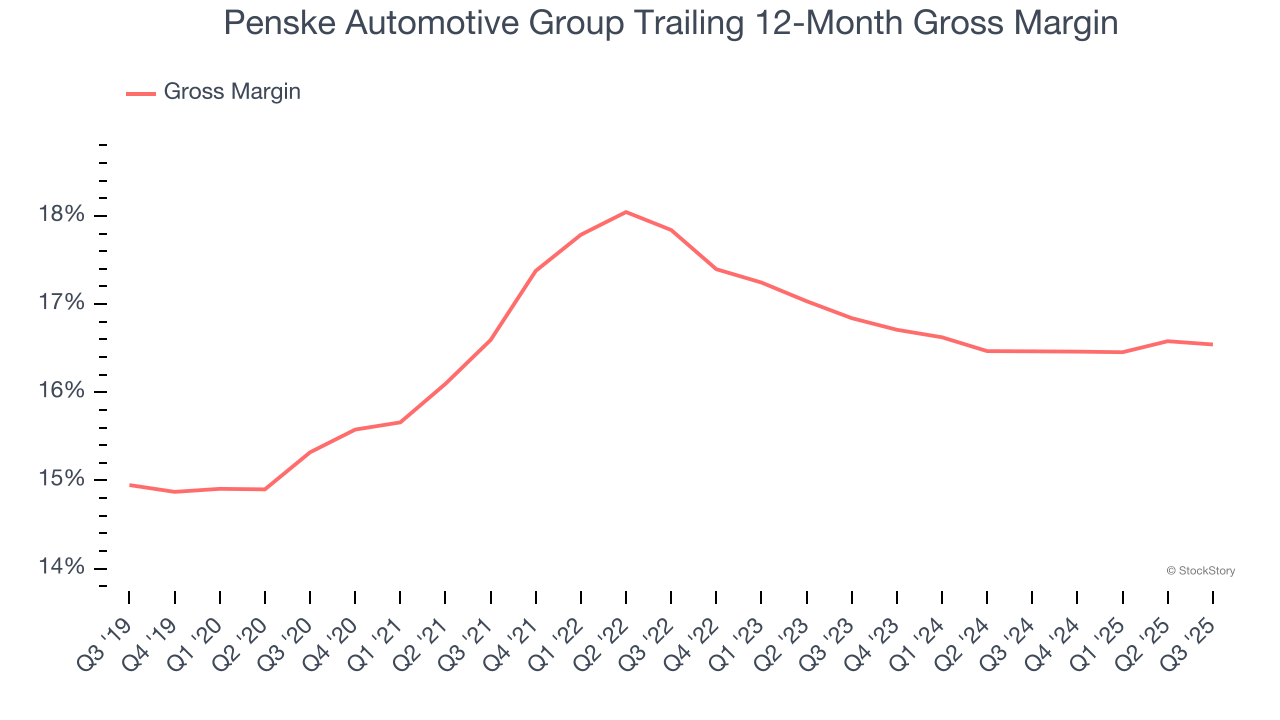

2. Low Gross Margin Reveals Weak Structural Profitability

Gross profit margins are an important measure of a retailer’s pricing power, product differentiation, and negotiating leverage.

Penske Automotive Group has bad unit economics for a retailer, signaling it operates in a competitive market and lacks pricing power because its inventory is sold in many places. As you can see below, it averaged a 16.5% gross margin over the last two years. Said differently, Penske Automotive Group had to pay a chunky $83.50 to its suppliers for every $100 in revenue.

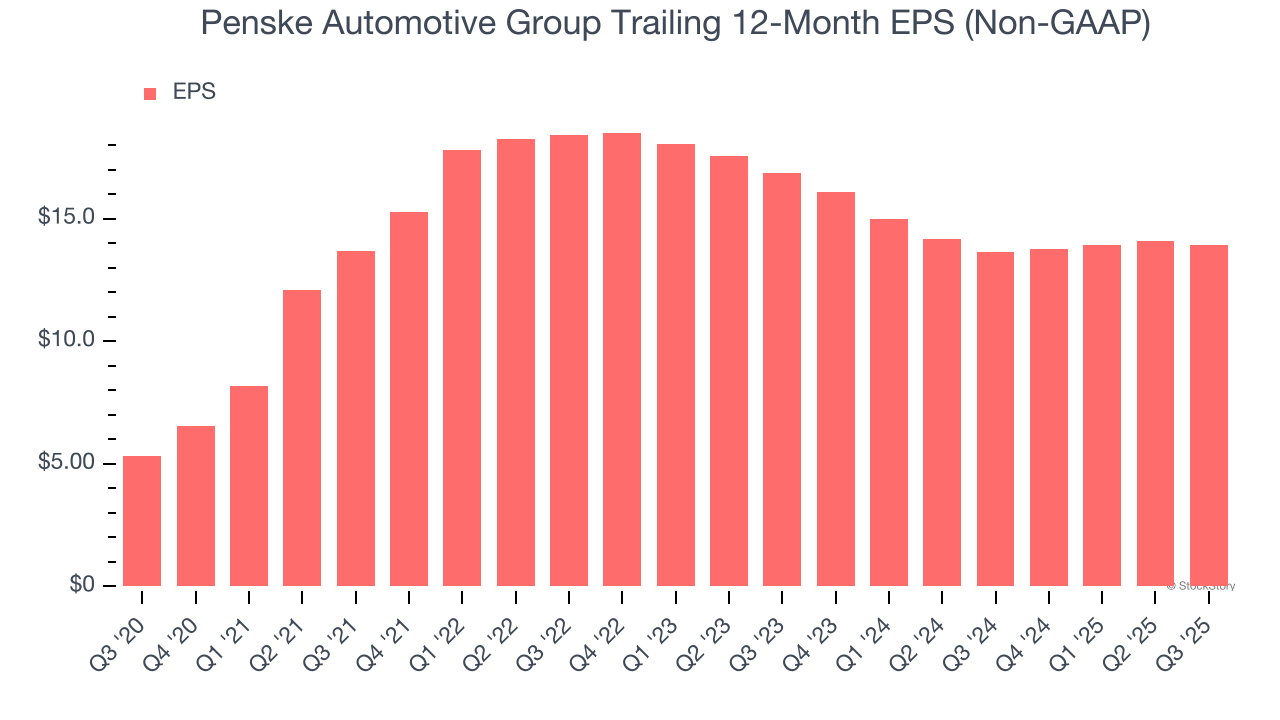

3. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Penske Automotive Group, its EPS declined by 8.8% annually over the last three years while its revenue grew by 4.2%. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

Penske Automotive Group’s business quality ultimately falls short of our standards. After the recent drawdown, the stock trades at 11.9× forward P/E (or $160.42 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're fairly confident there are better stocks to buy right now. We’d recommend looking at one of Charlie Munger’s all-time favorite businesses.

Stocks We Would Buy Instead of Penske Automotive Group

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.