Since July 2025, HEICO has been in a holding pattern, posting a small return of 4.4% while floating around $338.15.

Does this present a buying opportunity for HEI? Or is its underperformance reflective of its story and business quality? Find out in our full research report, it’s free.

Why Are We Positive On HEICO?

Founded in 1957, HEICO (NYSE: HEI) manufactures and services aerospace and electronic components for commercial aviation, defense, space, and other industries.

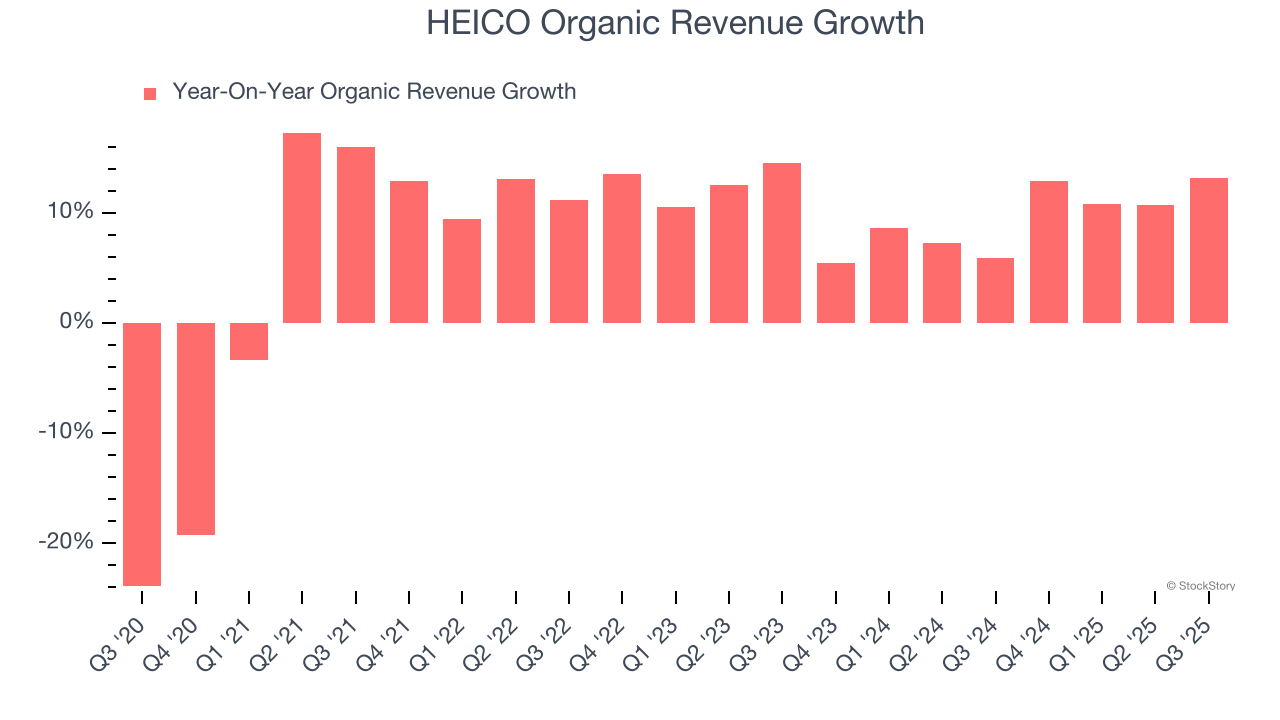

1. Organic Growth Indicates Solid Core Business

In addition to reported revenue, organic revenue is a useful data point for analyzing Aerospace companies. This metric gives visibility into HEICO’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, HEICO’s organic revenue averaged 9.4% year-on-year growth. This performance was solid and shows it can expand steadily without relying on expensive (and risky) acquisitions.

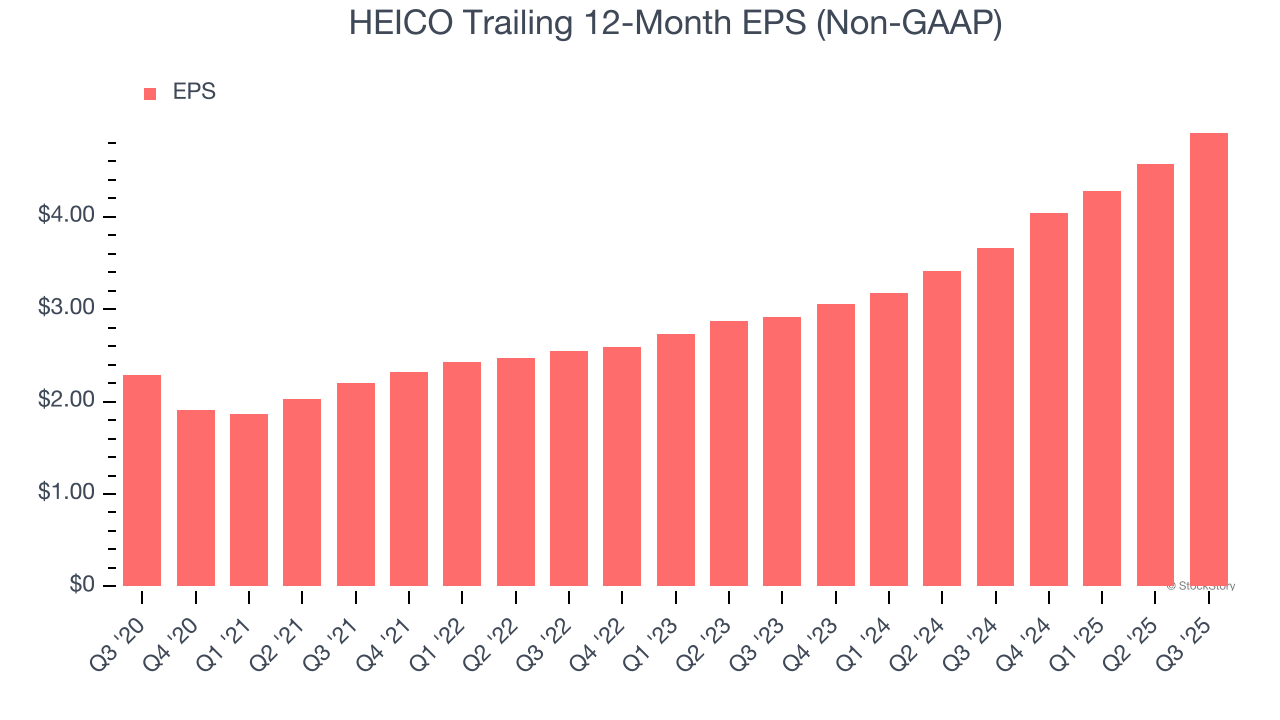

2. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

HEICO’s EPS grew at a spectacular 16.5% compounded annual growth rate over the last five years. This performance was better than most industrials businesses.

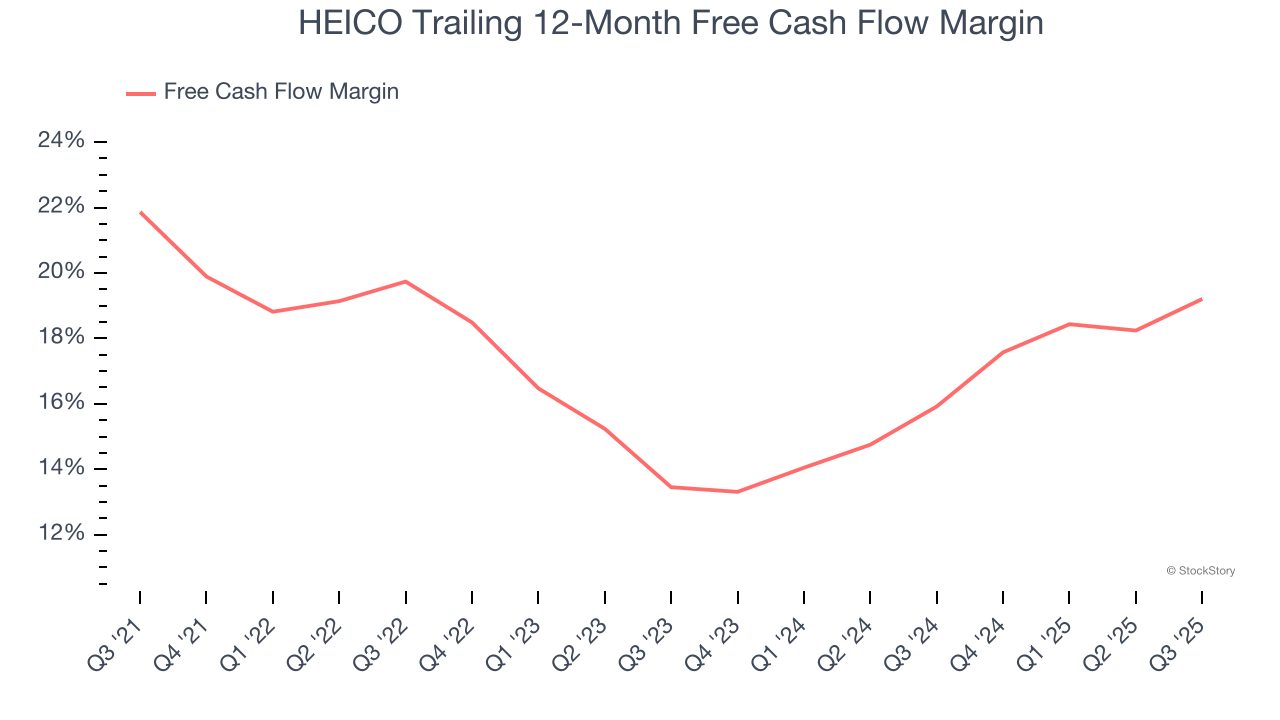

3. Excellent Free Cash Flow Margin Boosts Reinvestment Potential

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

HEICO has shown terrific cash profitability, putting it in an advantageous position to invest in new products, return capital to investors, and consolidate the market during industry downturns. The company’s free cash flow margin was among the best in the industrials sector, averaging 17.7% over the last five years.

Final Judgment

These are just a few reasons why we think HEICO is one of the best industrials companies out there, but at $338.15 per share (or 60.8× forward P/E), is now the right time to buy the stock? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than HEICO

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.