As the Q4 earnings season wraps, let’s dig into this quarter’s best and worst performers in the engineered components and systems industry, including Timken (NYSE: TKR) and its peers.

Engineered components and systems companies possess technical know-how in sometimes narrow areas such as metal forming or intelligent robotics. Lately, automation and connected equipment collecting analyzable data have been trending, creating new demand. On the other hand, like the broader industrials sector, engineered components and systems companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

The 9 engineered components and systems stocks we track reported a satisfactory Q4. As a group, revenues beat analysts’ consensus estimates by 2.5% while next quarter’s revenue guidance was 0.9% below.

Thankfully, share prices of the companies have been resilient as they are up 10% on average since the latest earnings results.

Timken (NYSE: TKR)

Established after the founder noticed the difficulty freight wagons had making sharp turns, Timken (NYSE: TKR) is a provider of industrial parts used across various sectors.

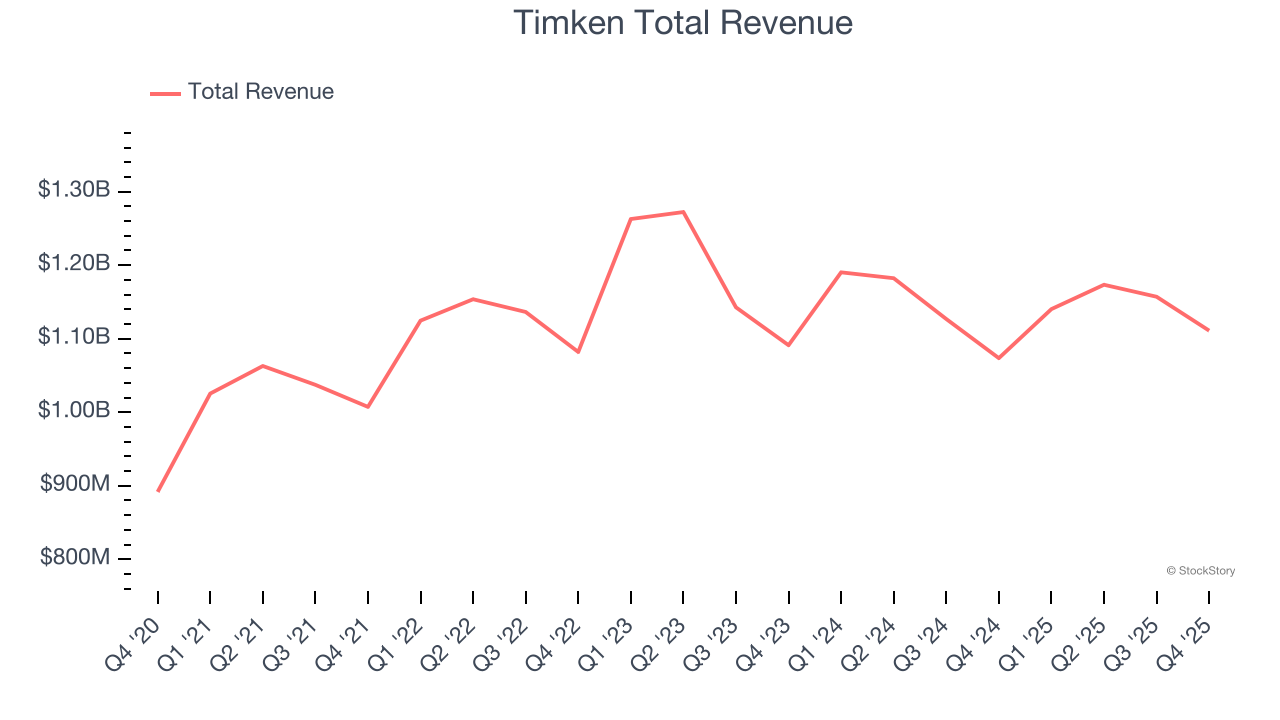

Timken reported revenues of $1.11 billion, up 3.5% year on year. This print exceeded analysts’ expectations by 3.5%. Overall, it was a very strong quarter for the company with a solid beat of analysts’ organic revenue estimates and an impressive beat of analysts’ revenue estimates.

"We finished the year strong, delivering higher organic sales and cash flow in the fourth quarter versus the prior year," said Lucian Boldea, president and chief executive officer.

Interestingly, the stock is up 12.2% since reporting and currently trades at $107.84.

Is now the time to buy Timken? Access our full analysis of the earnings results here, it’s free.

Best Q4: Arrow Electronics (NYSE: ARW)

Founded as a single retail store, Arrow Electronics (NYSE: ARW) provides electronic components and enterprise computing solutions to businesses globally.

Arrow Electronics reported revenues of $8.75 billion, up 20.1% year on year, outperforming analysts’ expectations by 6.6%. The business had an incredible quarter with EPS guidance for next quarter exceeding analysts’ expectations and an impressive beat of analysts’ EBITDA estimates.

The market seems happy with the results as the stock is up 10.7% since reporting. It currently trades at $156.19.

Is now the time to buy Arrow Electronics? Access our full analysis of the earnings results here, it’s free.

Weakest Q4: Worthington (NYSE: WOR)

Founded by a steel salesman, Worthington (NYSE: WOR) specializes in steel processing, pressure cylinders, and engineered cabs for commercial markets.

Worthington reported revenues of $327.5 million, up 19.5% year on year, exceeding analysts’ expectations by 5.4%. Still, it was a slower quarter as it posted a significant miss of analysts’ EBITDA estimates and a significant miss of analysts’ EPS estimates.

Interestingly, the stock is up 4.7% since the results and currently trades at $58.95.

Read our full analysis of Worthington’s results here.

RBC Bearings (NYSE: RBC)

With a Guinness World Record for engineering the largest spherical plain bearing, RBC Bearings (NYSE: RBC) is a manufacturer of bearings and related components for the aerospace & defense, industrial, and transportation industries.

RBC Bearings reported revenues of $461.6 million, up 17% year on year. This number was in line with analysts’ expectations. More broadly, it was a mixed quarter as it also produced a decent beat of analysts’ adjusted operating income estimates but a miss of analysts’ EBITDA estimates.

The stock is up 6.9% since reporting and currently trades at $552.44.

Read our full, actionable report on RBC Bearings here, it’s free.

Graham Corporation (NYSE: GHM)

Founded when its founder patented a unique design for a vacuum system used in the sugar refining process, Graham (NYSE: GHM) provides vacuum and heat transfer equipment for the energy, petrochemical, refining, and chemical sectors.

Graham Corporation reported revenues of $56.7 million, up 20.5% year on year. This result topped analysts’ expectations by 8.3%. It was an exceptional quarter as it also produced a beat of analysts’ EPS estimates and an impressive beat of analysts’ EBITDA estimates.

Graham Corporation delivered the biggest analyst estimates beat and fastest revenue growth, but had the weakest full-year guidance update among its peers. The stock is up 14.4% since reporting and currently trades at $84.40.

Read our full, actionable report on Graham Corporation here, it’s free.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.