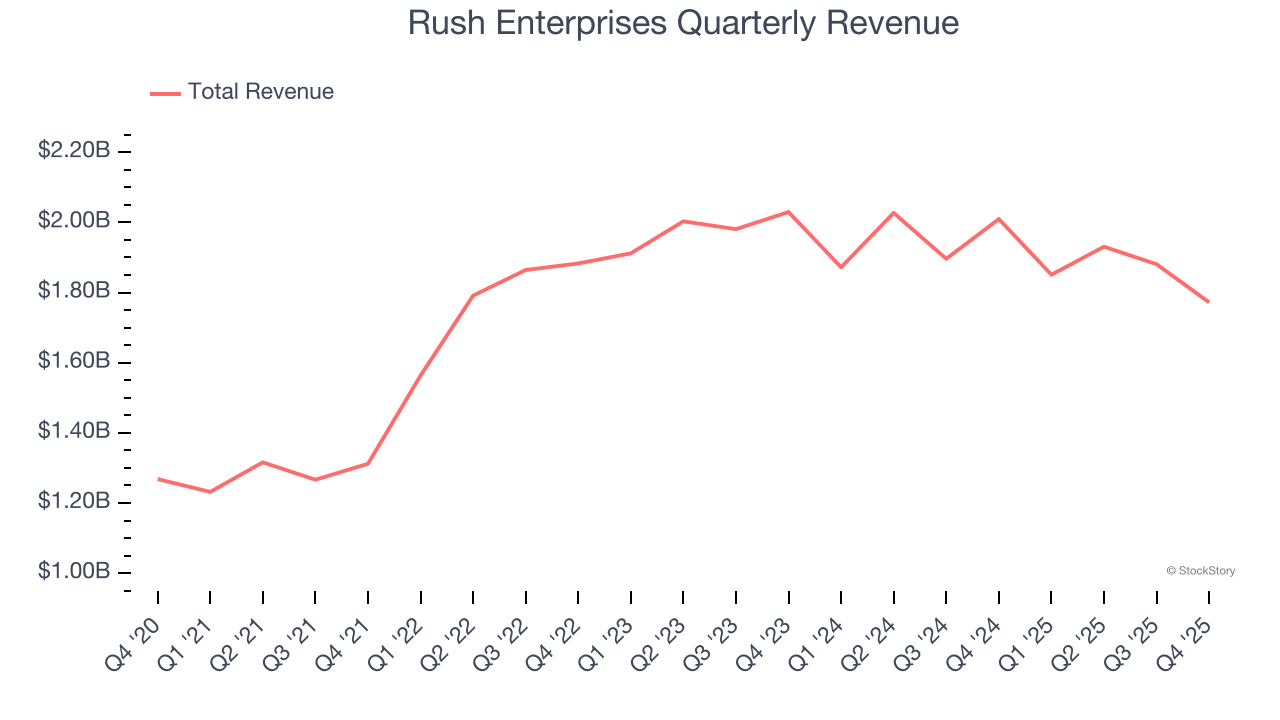

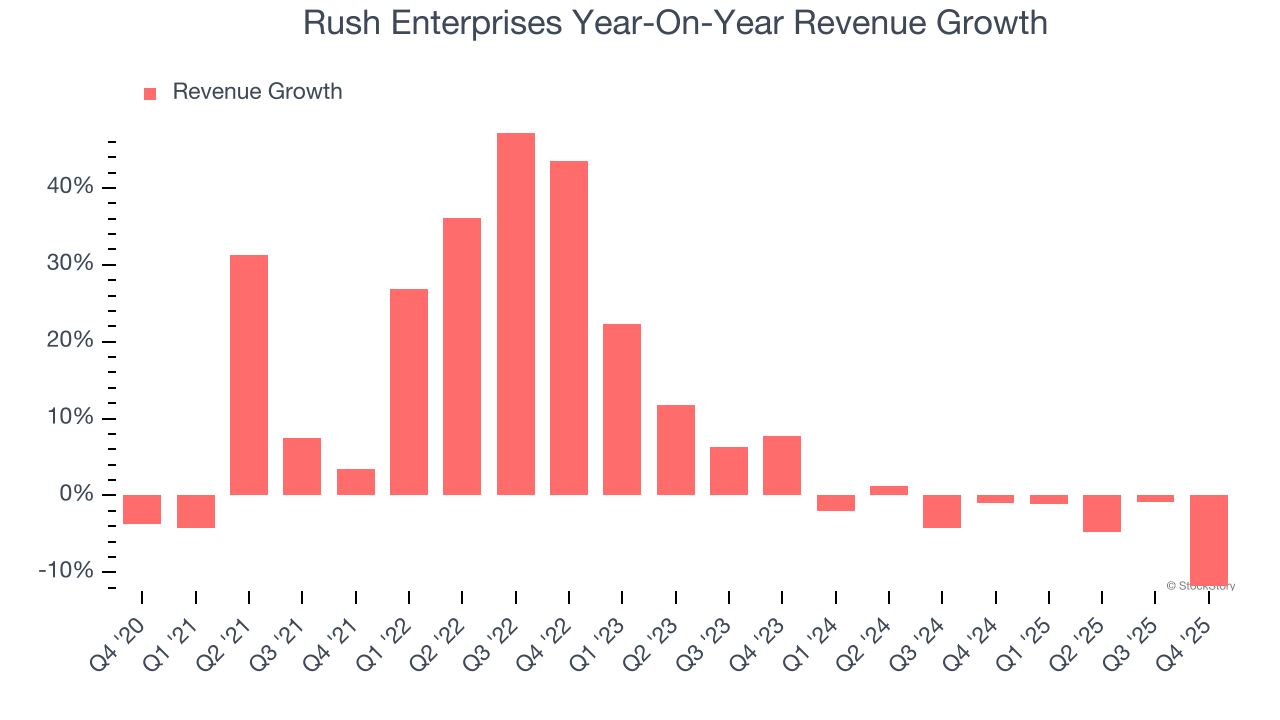

Commercial vehicle retailer Rush Enterprises (NASDAQ: RUSH.A) reported Q4 CY2025 results exceeding the market’s revenue expectations, but sales fell by 11.8% year on year to $1.77 billion. Its GAAP profit of $0.81 per share was 17.1% above analysts’ consensus estimates.

Is now the time to buy Rush Enterprises? Find out by accessing our full research report, it’s free.

Rush Enterprises (RUSHA) Q4 CY2025 Highlights:

- Revenue: $1.77 billion vs analyst estimates of $1.73 billion (11.8% year-on-year decline, 2.6% beat)

- EPS (GAAP): $0.81 vs analyst estimates of $0.69 (17.1% beat)

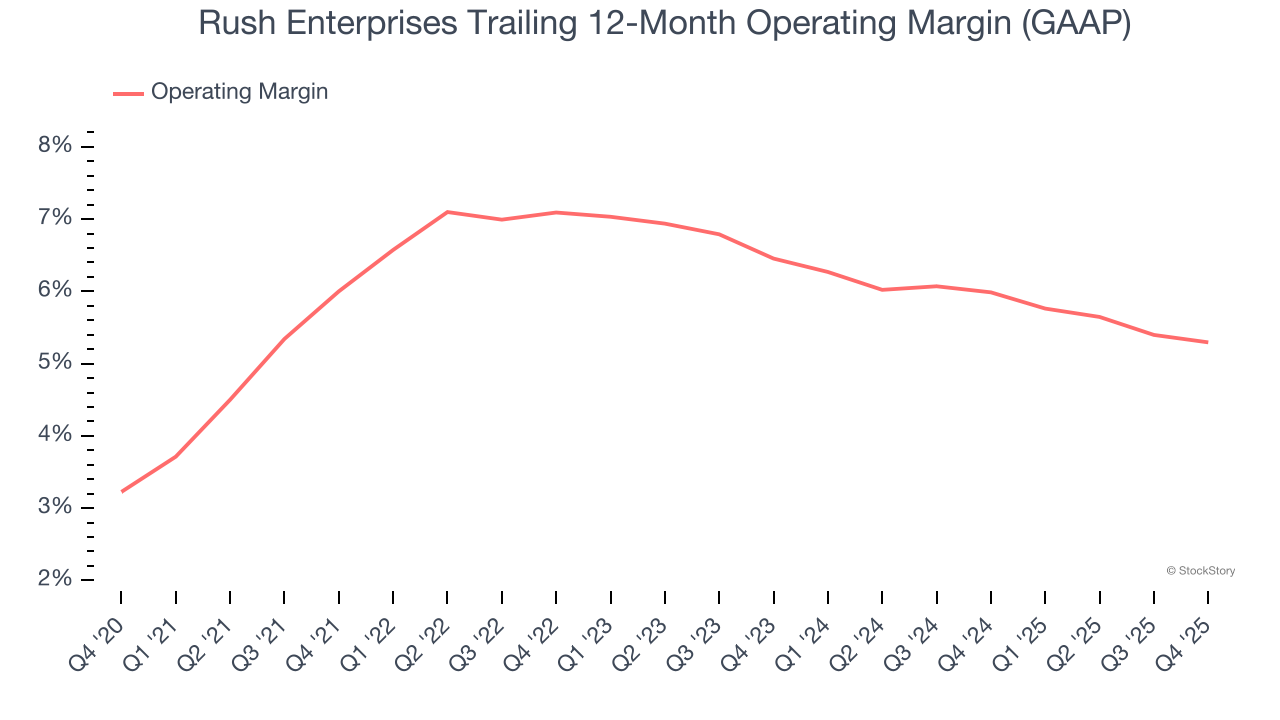

- Operating Margin: 5.2%, in line with the same quarter last year

- Market Capitalization: $5.40 billion

NEW BRAUNFELS, Texas, Feb. 17, 2026 (GLOBE NEWSWIRE) -- Rush Enterprises, Inc. (NASDAQ: RUSHA & RUSHB), which operates the largest network of commercial vehicle dealerships in North America, today announced that for the year ended December 31, 2025, the Company achieved revenues of $7.4 billion and net income of $263.8 million, or $3.27 per diluted share, compared with revenues of $7.8 billion and net income of $304.2 million, or $3.72 per diluted share, for the year ended December 31, 2024. In the third quarter of 2024, the Company recognized a one-time, pre-tax charge of approximately $3.3 million, or $0.03 per share, related to property damage caused by Hurricane Helene. Excluding the one-time losses related to that incident, the Company’s adjusted net income for the year ended December 31, 2024, was $306.7 million, or $3.75 per diluted share. Additionally, the Company’s Board of Directors declared a cash dividend of $0.19 per share of Class A and Class B common stock, to be paid on March 18, 2026, to all shareholders of record as of March 3, 2026.“Despite another challenging year for the commercial vehicle industry, I am proud of the results our team delivered in 2025,” said W.M. “Rusty” Rush, Chairman, Chief Executive Officer and President of Rush Enterprises, Inc.

Company Overview

Headquartered in Texas, Rush Enterprises (NASDAQ: RUSH.A) provides truck-related services and solutions, including sales, leasing, parts, and maintenance for commercial vehicles.

Revenue Growth

Reviewing a company’s long-term sales performance reveals insights into its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Rush Enterprises grew its sales at a solid 9.4% compounded annual growth rate. Its growth beat the average industrials company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Rush Enterprises’s recent performance marks a sharp pivot from its five-year trend as its revenue has shown annualized declines of 3.1% over the last two years.

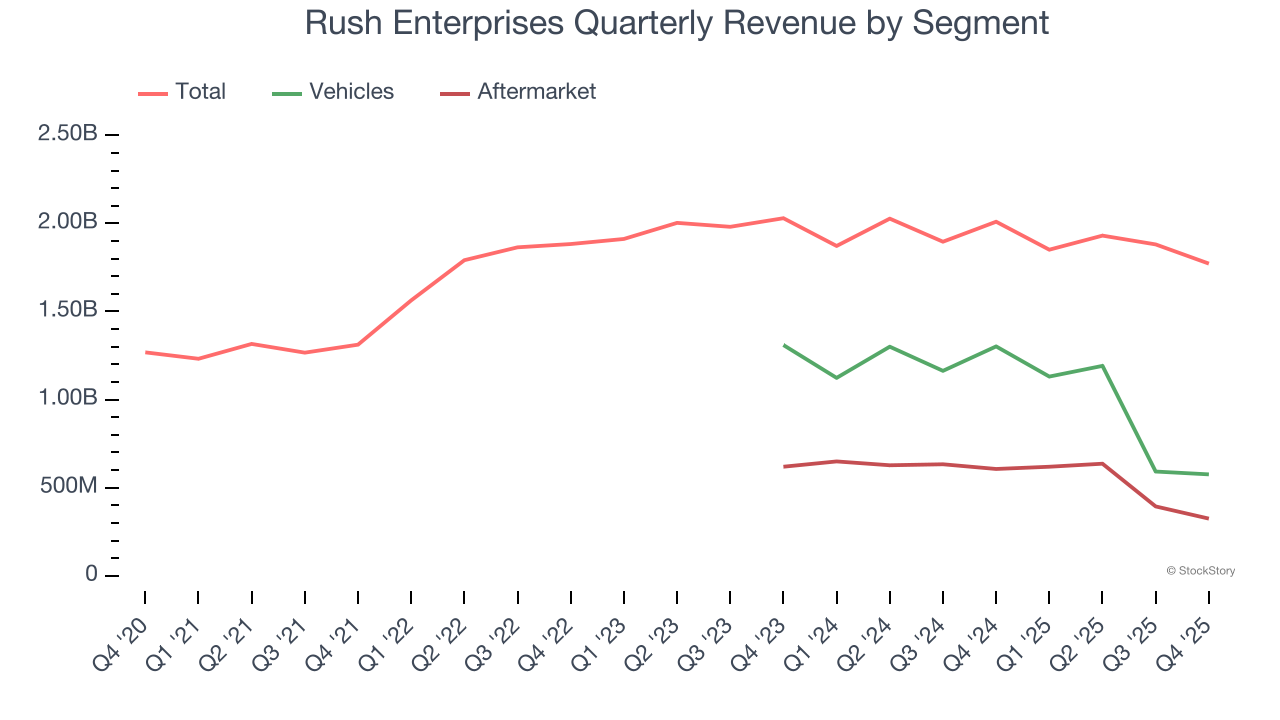

We can better understand the company’s revenue dynamics by analyzing its most important segments, Vehicles and Aftermarket, which are 32.5% and 18.3% of revenue. Over the last two years, Rush Enterprises’s Vehicles revenue (new and used commercial trucks) averaged 22.6% year-on-year declines while its Aftermarket revenue (parts and services) averaged 17.9% declines.

This quarter, Rush Enterprises’s revenue fell by 11.8% year on year to $1.77 billion but beat Wall Street’s estimates by 2.6%.

Looking ahead, sell-side analysts expect revenue to grow 1.2% over the next 12 months. While this projection suggests its newer products and services will spur better top-line performance, it is still below the sector average.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Rush Enterprises’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 6.2% over the last five years. This profitability was paltry for an industrials business and caused by its suboptimal cost structureand low gross margin.

Looking at the trend in its profitability, Rush Enterprises’s operating margin might fluctuated slightly but has generally stayed the same over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Rush Enterprises generated an operating margin profit margin of 5.2%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

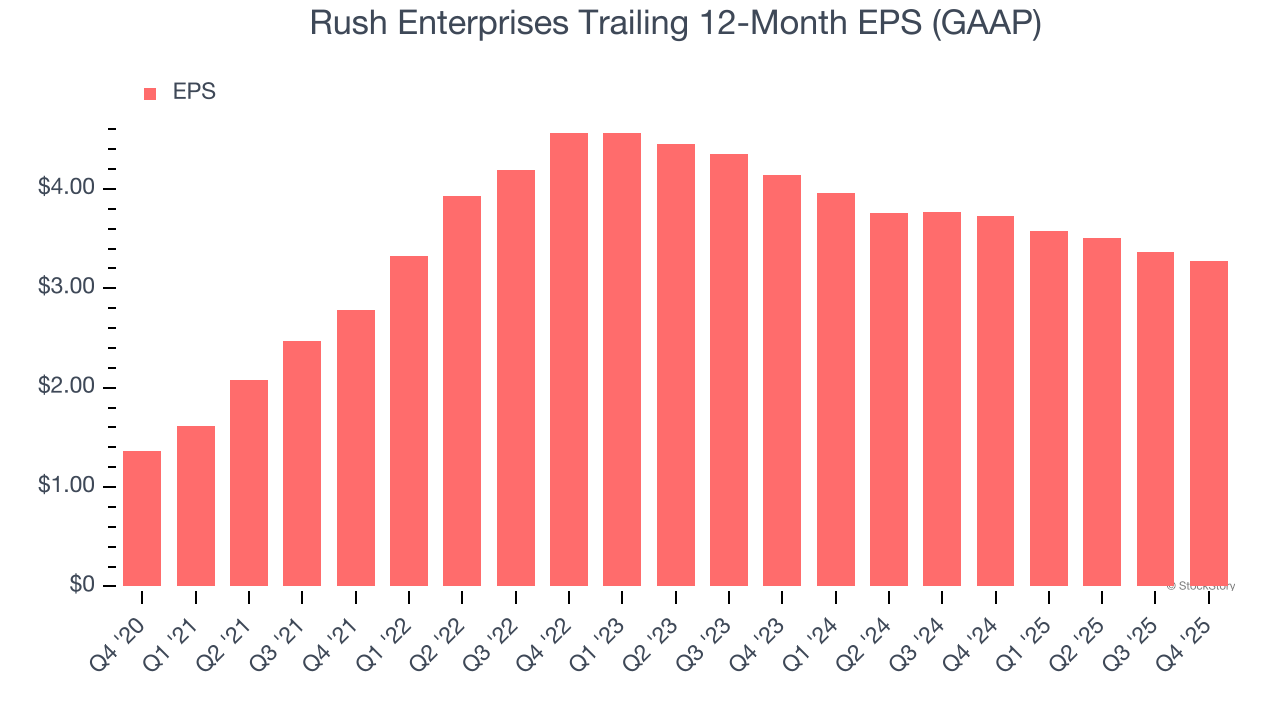

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Rush Enterprises’s EPS grew at an astounding 19.2% compounded annual growth rate over the last five years, higher than its 9.4% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

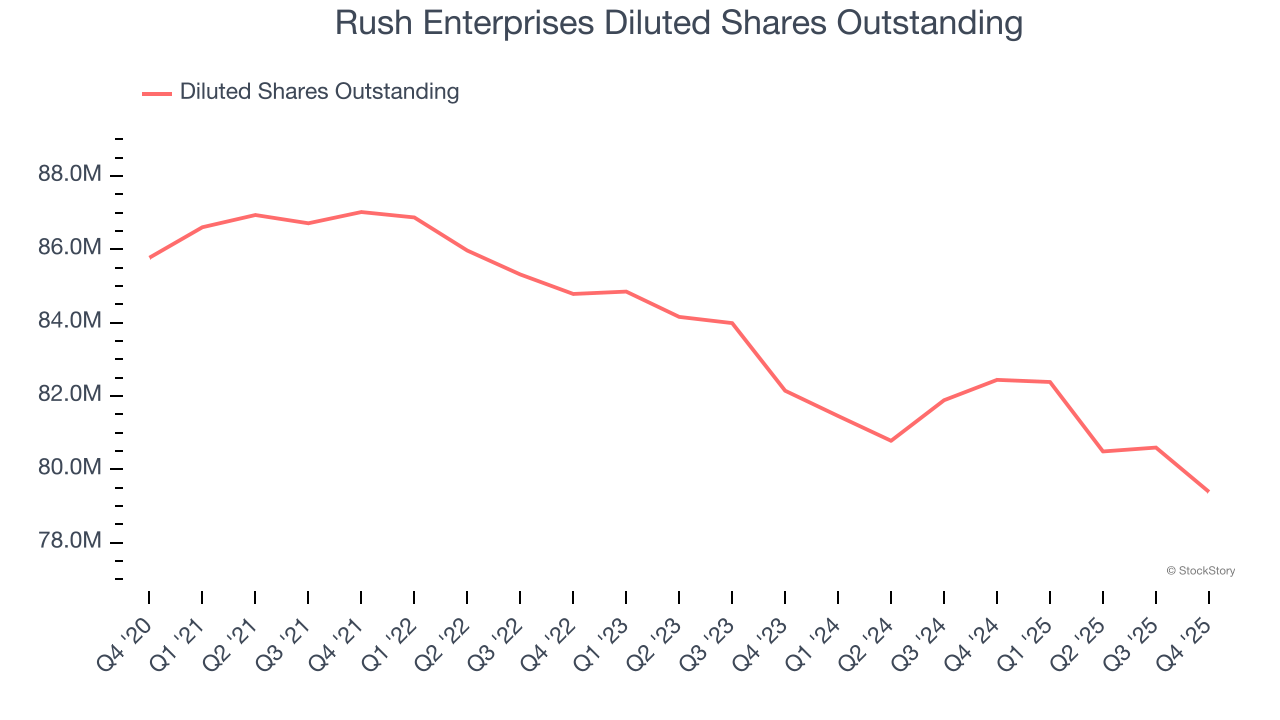

Diving into Rush Enterprises’s quality of earnings can give us a better understanding of its performance. A five-year view shows that Rush Enterprises has repurchased its stock, shrinking its share count by 7.4%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For Rush Enterprises, its two-year annual EPS declines of 11.2% mark a reversal from its (seemingly) healthy five-year trend. We hope Rush Enterprises can return to earnings growth in the future.

In Q4, Rush Enterprises reported EPS of $0.81, down from $0.91 in the same quarter last year. Despite falling year on year, this print easily cleared analysts’ estimates. Over the next 12 months, Wall Street expects Rush Enterprises’s full-year EPS of $3.27 to grow 13.5%.

Key Takeaways from Rush Enterprises’s Q4 Results

We enjoyed seeing Rush Enterprises beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. Overall, this print had some key positives. The stock remained flat at $70.21 immediately after reporting.

So do we think Rush Enterprises is an attractive buy at the current price? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).