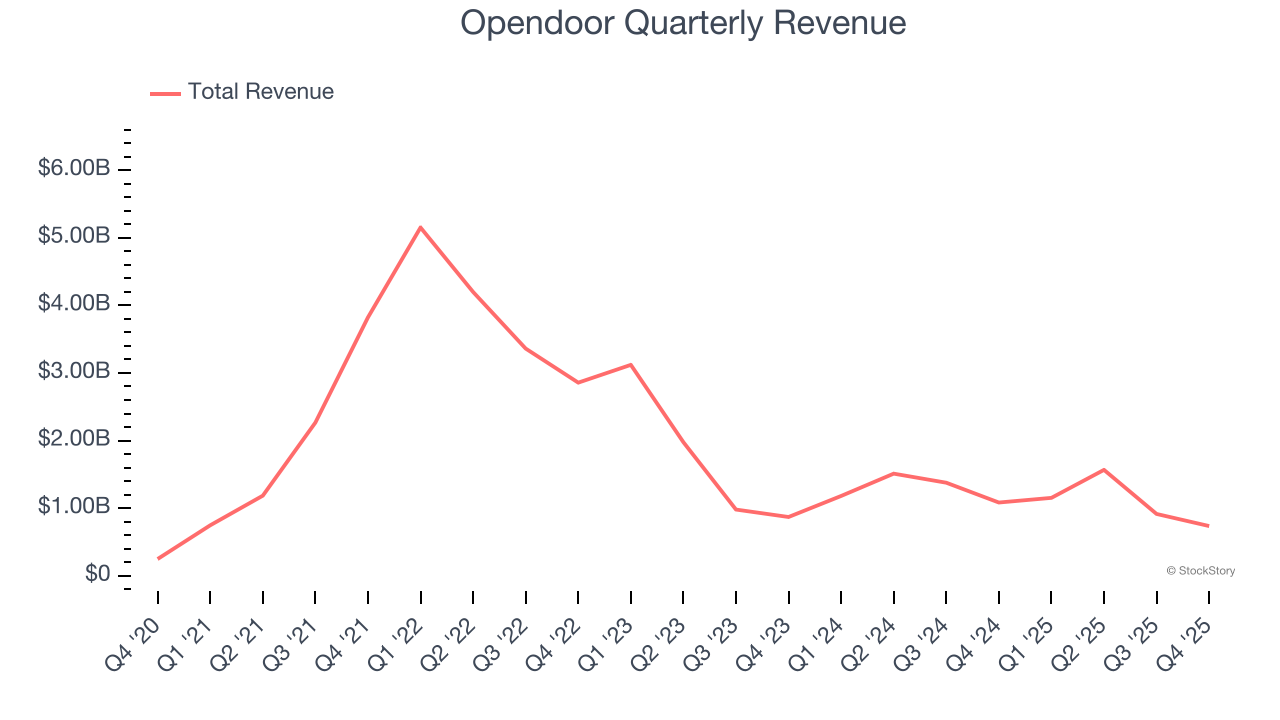

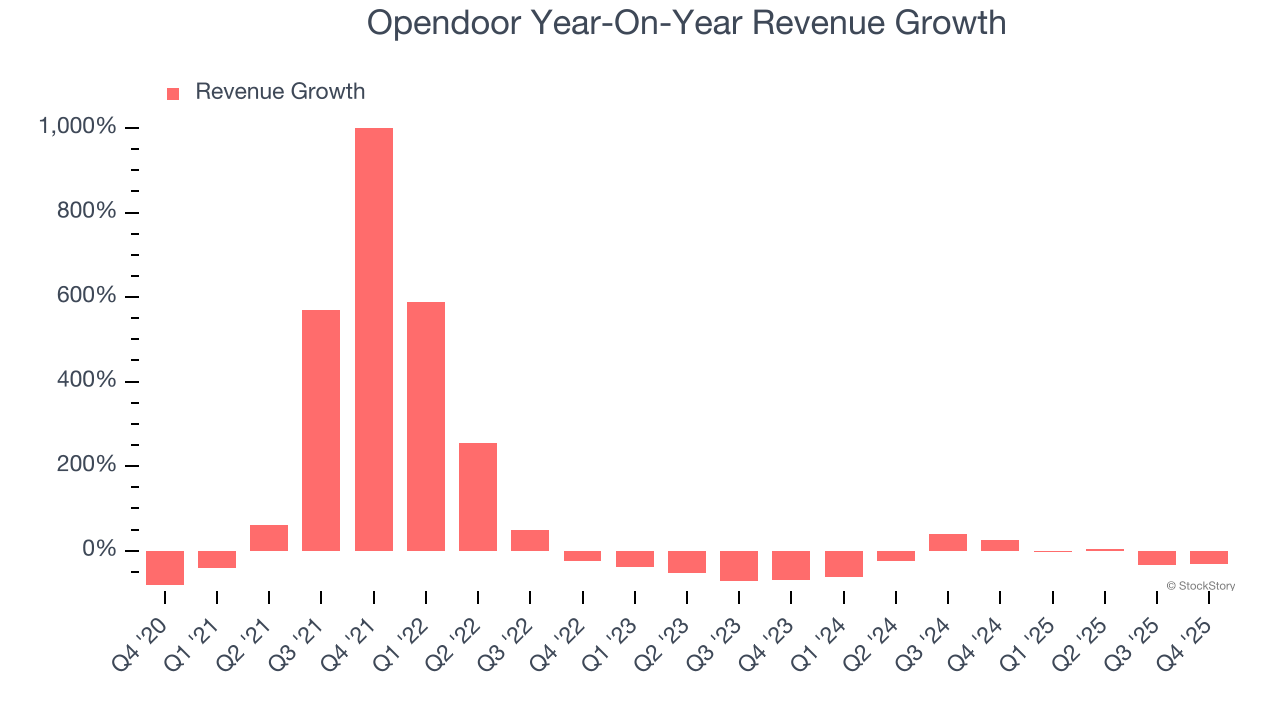

Technology real estate company Opendoor (NASDAQ: OPEN) reported Q4 CY2025 results beating Wall Street’s revenue expectations, but sales fell by 32.1% year on year to $736 million. Its non-GAAP loss of $0.07 per share was 25.3% above analysts’ consensus estimates.

Is now the time to buy Opendoor? Find out by accessing our full research report, it’s free.

Opendoor (OPEN) Q4 CY2025 Highlights:

- Revenue: $736 million vs analyst estimates of $595 million (32.1% year-on-year decline, 23.7% beat)

- Adjusted EPS: -$0.07 vs analyst estimates of -$0.09 (25.3% beat)

- Adjusted EBITDA: -$43 million (-5.8% margin, 12.2% year-on-year growth)

- EBITDA guidance for Q1 CY2026 is $30 million at the midpoint, above analyst estimates of -$37.4 million

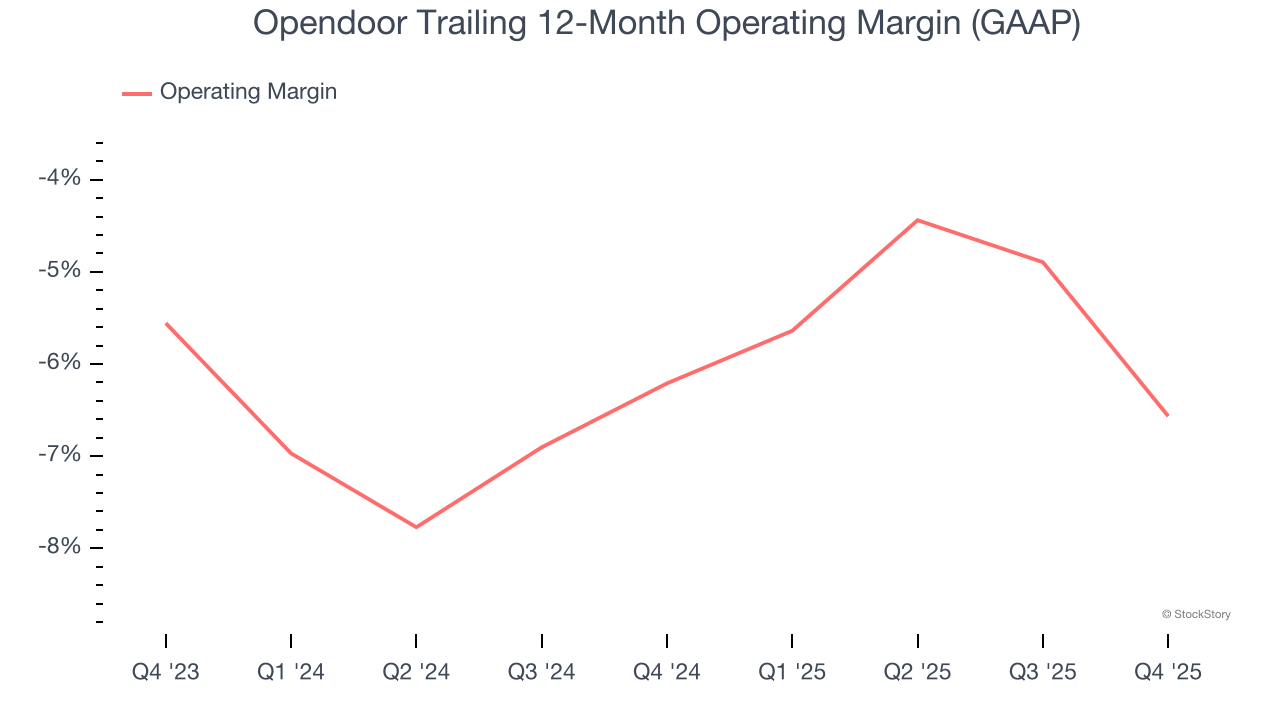

- Operating Margin: -20.4%, down from -8.7% in the same quarter last year

- Free Cash Flow was $67 million, up from -$83 million in the same quarter last year

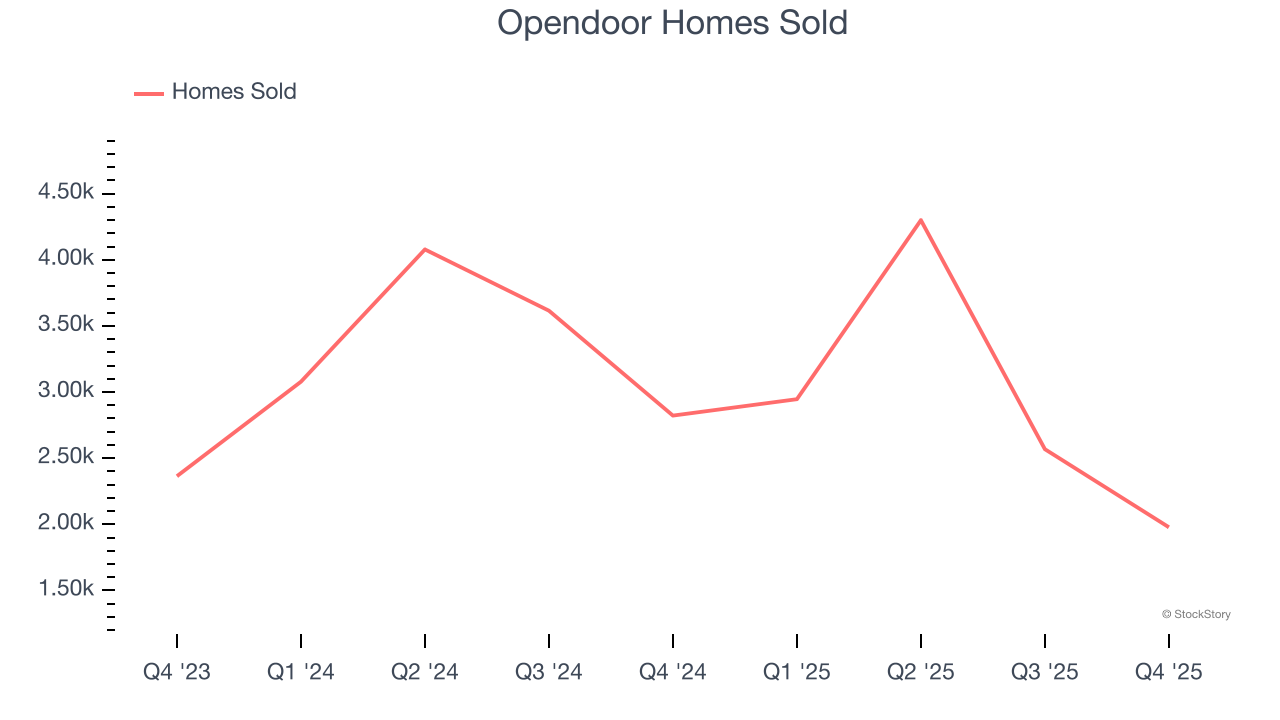

- Homes Sold: 1,978, down 844 year on year

- Market Capitalization: $4.41 billion

“Last quarter, we outlined a four-step plan to transform Opendoor: reach breakeven Adjusted Net Income by the end of 2026 on a 12-month go-forward basis, drive positive unit economics while increasing transaction velocity, transition to direct-to-consumer relationships, and expand our product suite. This quarter demonstrates we are executing on that plan,” said Kaz Nejatian, CEO of Opendoor.

Company Overview

Founded by real estate guru Eric Wu, Opendoor (NASDAQ: OPEN) offers a technology-driven, convenient, and streamlined process to buy and sell homes.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last five years, Opendoor grew its sales at a 11.1% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new product or trend. Opendoor’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 20.7% annually.

We can better understand the company’s revenue dynamics by analyzing its number of homes sold, which reached 1,978 in the latest quarter. Over the last two years, Opendoor’s homes sold averaged 7.7% year-on-year declines. Because this number is higher than its revenue growth during the same period, we can see the company’s monetization has fallen.

This quarter, Opendoor’s revenue fell by 32.1% year on year to $736 million but beat Wall Street’s estimates by 23.7%.

Looking ahead, sell-side analysts expect revenue to grow 7% over the next 12 months. While this projection implies its newer products and services will fuel better top-line performance, it is still below average for the sector.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Opendoor’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging negative 6.4% over the last two years. Unprofitable consumer discretionary companies that fail to improve their losses or grow sales rapidly deserve extra scrutiny. For the time being, it’s unclear if Opendoor’s business model is sustainable.

In Q4, Opendoor generated a negative 20.4% operating margin. The company's consistent lack of profits raise a flag.

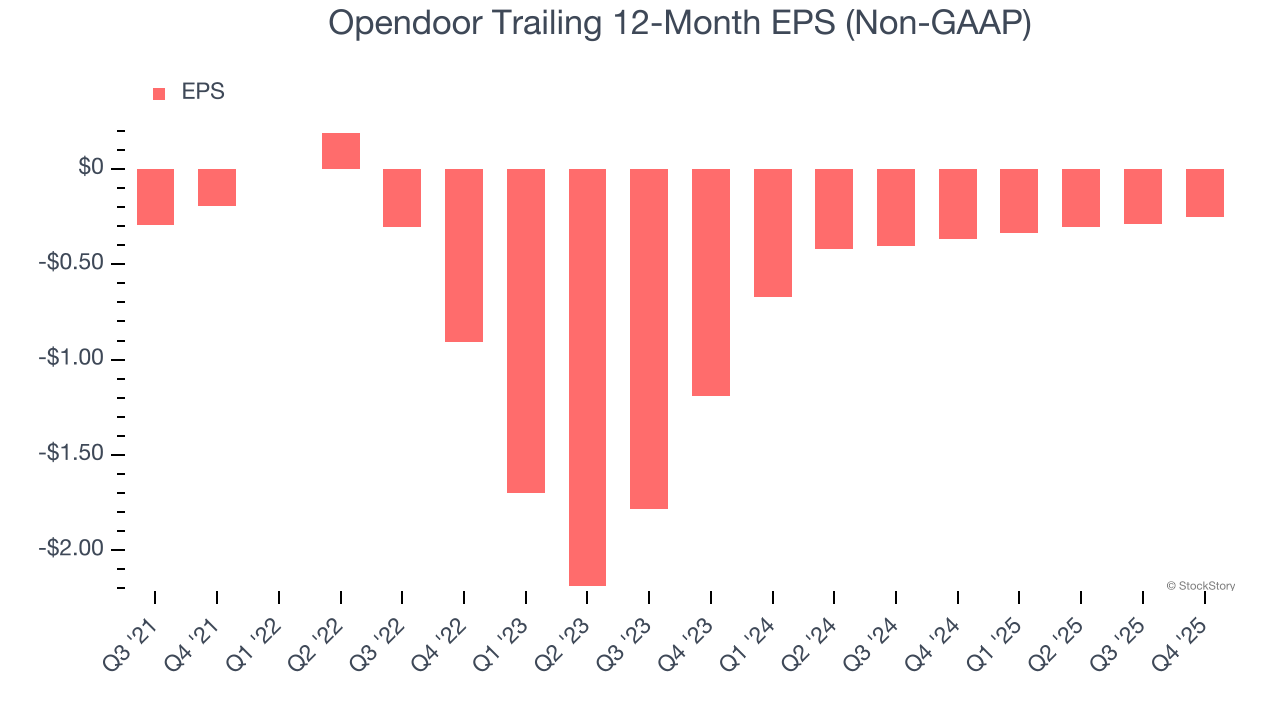

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Opendoor’s earnings losses deepened over the last four years as its EPS dropped 7% annually. However, it’s bucked its trend as of late, increasing its EPS over the last two years. We’ll see if it can maintain its growth.

In Q4, Opendoor reported adjusted EPS of negative $0.07, up from negative $0.11 in the same quarter last year. This print easily cleared analysts’ estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Opendoor to improve its earnings losses. Analysts forecast its full-year EPS of negative $0.25 will advance to negative $0.21.

Key Takeaways from Opendoor’s Q4 Results

We were impressed by Opendoor’s optimistic EBITDA guidance for next quarter, which blew past analysts’ expectations. We were also excited its revenue outperformed Wall Street’s estimates by a wide margin. Zooming out, we think this was a good print with some key areas of upside. The stock traded up 16.5% to $5.36 immediately following the results.

Opendoor put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).