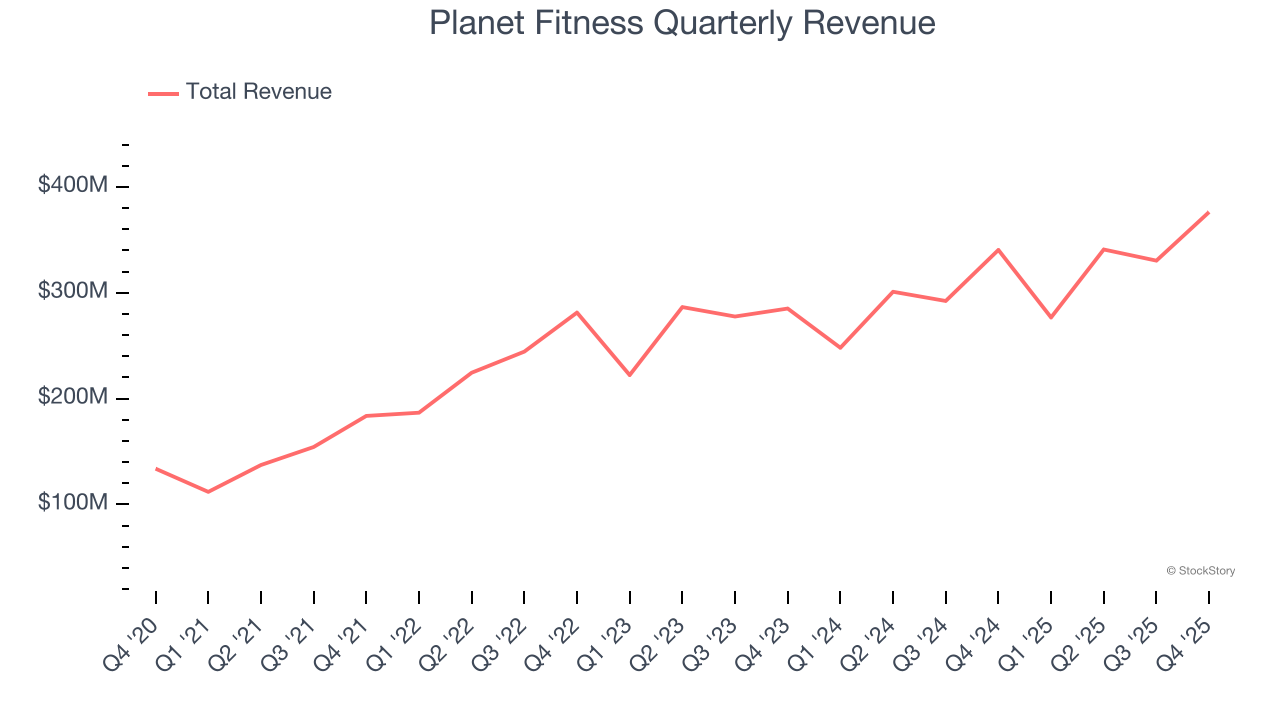

Inclusive gym franchise company (NYSE: PLNT) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, with sales up 10.5% year on year to $376.3 million. Its non-GAAP profit of $0.83 per share was 4.8% above analysts’ consensus estimates.

Is now the time to buy Planet Fitness? Find out by accessing our full research report, it’s free.

Planet Fitness (PLNT) Q4 CY2025 Highlights:

- Revenue: $376.3 million vs analyst estimates of $367.3 million (10.5% year-on-year growth, 2.4% beat)

- Adjusted EPS: $0.83 vs analyst estimates of $0.79 (4.8% beat)

- Adjusted EBITDA: $146.3 million vs analyst estimates of $144 million (38.9% margin, 1.5% beat)

- 2026 Guidance: 9% year-on-year revenue growth on 4-5% same-store sales growth (both misses)

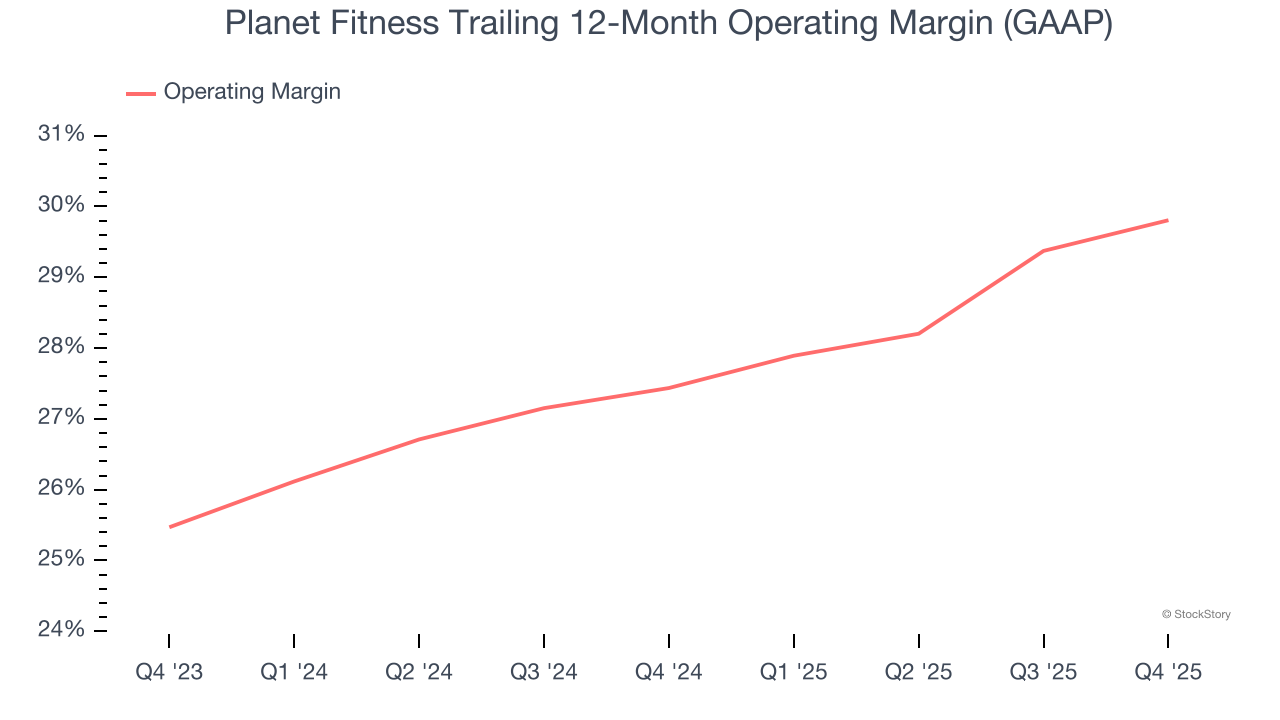

- Operating Margin: 28.2%, up from 26.4% in the same quarter last year

- Free Cash Flow Margin: 15.7%, up from 2.1% in the same quarter last year

- Same-Store Sales rose 5.7% year on year, in line with the same quarter last year

- Market Capitalization: $7.53 billion

"We're pleased with our strong performance in 2025 that was the result of our unwavering focus on our four strategic imperatives. We ended the year with approximately 20.8 million members, and a global footprint of nearly 2,900 clubs, reinforcing the quality of our member experience and our core conviction that anyone can get a great workout at Planet Fitness for an incredible value. Adding approximately 1.1 million net new members in 2025—the first full-year of our 50 percent price increase for new Classic Card members—highlights the incredible demand for our brand," said Colleen Keating, Chief Executive Officer.

Company Overview

Founded by two brothers who purchased a struggling gym, Planet Fitness (NYSE: PLNT) is a gym franchise that caters to casual fitness users by providing a friendly and inclusive atmosphere.

Revenue Growth

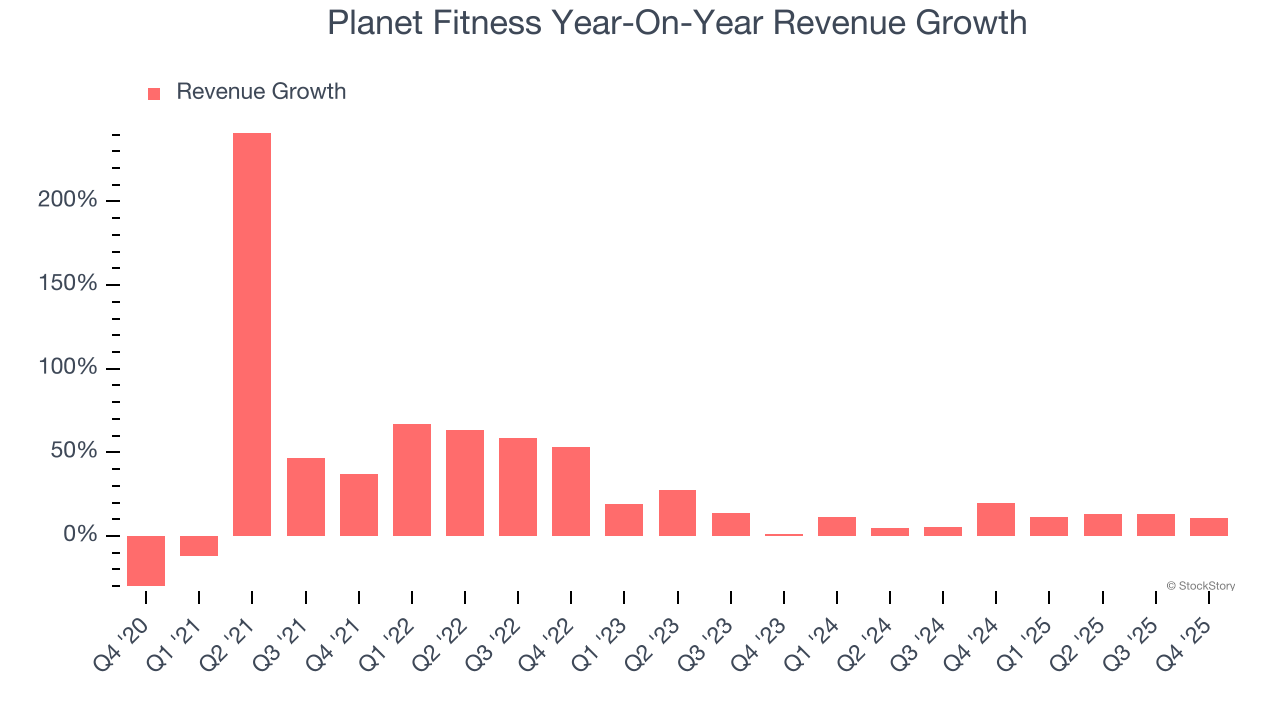

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Planet Fitness grew its sales at a 26.6% annual rate. Though this growth is acceptable on an absolute basis, we need to see more than just topline growth for the consumer discretionary sector, which can display significant earnings volatility. This means our bar for the sector is particularly high, reflecting the non-essential and hit-driven nature of the products and services offered. Additionally, five-year CAGR starts around Covid, when revenue was depressed then rebounded.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Planet Fitness’s recent performance shows its demand has slowed as its annualized revenue growth of 11.2% over the last two years was below its five-year trend. We’re wary when companies in the sector see decelerations in revenue growth, as it could signal changing consumer tastes aided by low switching costs. Note that COVID hurt Planet Fitness’s business in 2020 and part of 2021, and it bounced back in a big way thereafter.

Planet Fitness also reports same-store sales, which show how much revenue its established locations generate. Over the last two years, Planet Fitness’s same-store sales averaged 5.9% year-on-year growth. Because this number is lower than its revenue growth, we can see the opening of new locations is boosting the company’s top-line performance.

This quarter, Planet Fitness reported year-on-year revenue growth of 10.5%, and its $376.3 million of revenue exceeded Wall Street’s estimates by 2.4%.

Looking ahead, sell-side analysts expect revenue to grow 10.9% over the next 12 months, similar to its two-year rate. This projection is underwhelming and indicates its newer products and services will not accelerate its top-line performance yet.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Operating Margin

Planet Fitness’s operating margin has been trending up over the last 12 months and averaged 28.7% over the last two years. The company’s higher efficiency is a breath of fresh air, but its suboptimal cost structure means it still sports paltry profitability for a consumer discretionary business.

This quarter, Planet Fitness generated an operating margin profit margin of 28.2%, up 1.8 percentage points year on year. This increase was a welcome development and shows it was more efficient.

Earnings Per Share

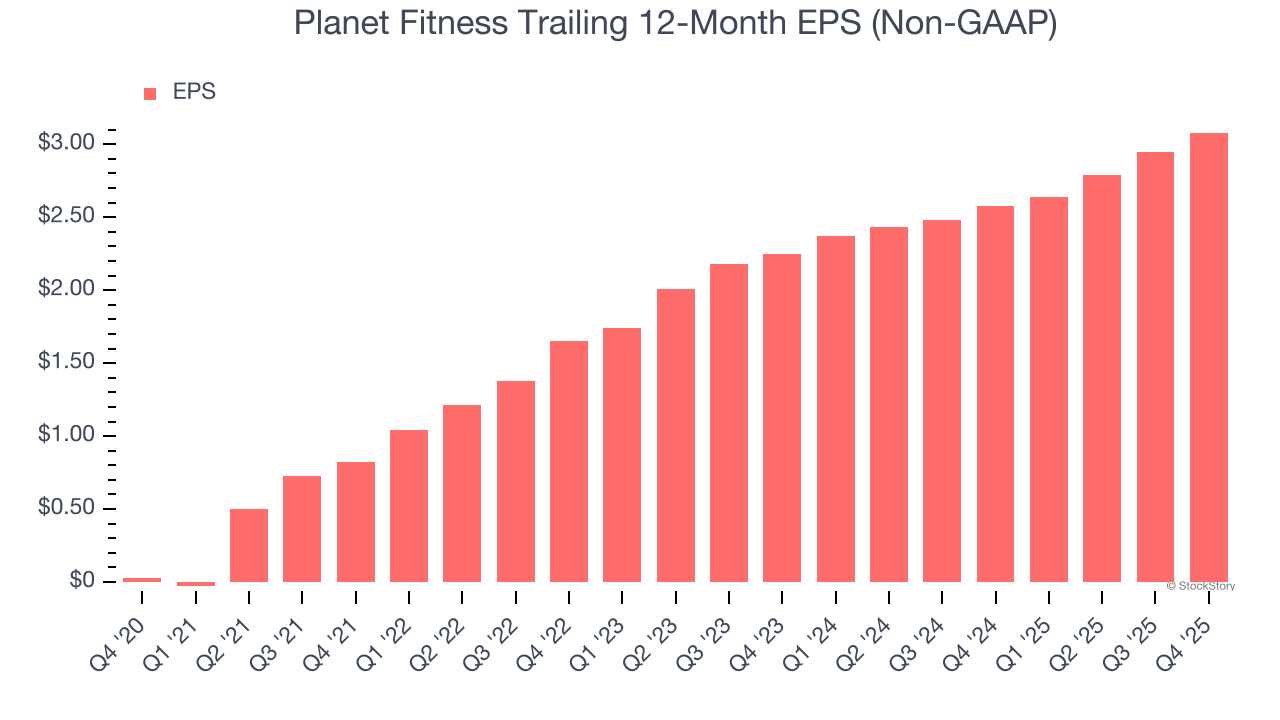

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Planet Fitness’s EPS grew at an astounding 153% compounded annual growth rate over the last five years, higher than its 26.6% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

In Q4, Planet Fitness reported adjusted EPS of $0.83, up from $0.70 in the same quarter last year. This print beat analysts’ estimates by 4.8%. Over the next 12 months, Wall Street expects Planet Fitness’s full-year EPS of $3.08 to grow 14.3%.

Key Takeaways from Planet Fitness’s Q4 Results

It was encouraging to see Planet Fitness beat analysts’ revenue expectations this quarter. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, 2026 guidance calls for 4-5% same-store sales growth and 9% reported year-on-year revenue growth, both of which missed expectations. This outlook is weighing heavily on shares, and the stock traded down 8.5% to $83 immediately after reporting.

So should you invest in Planet Fitness right now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).