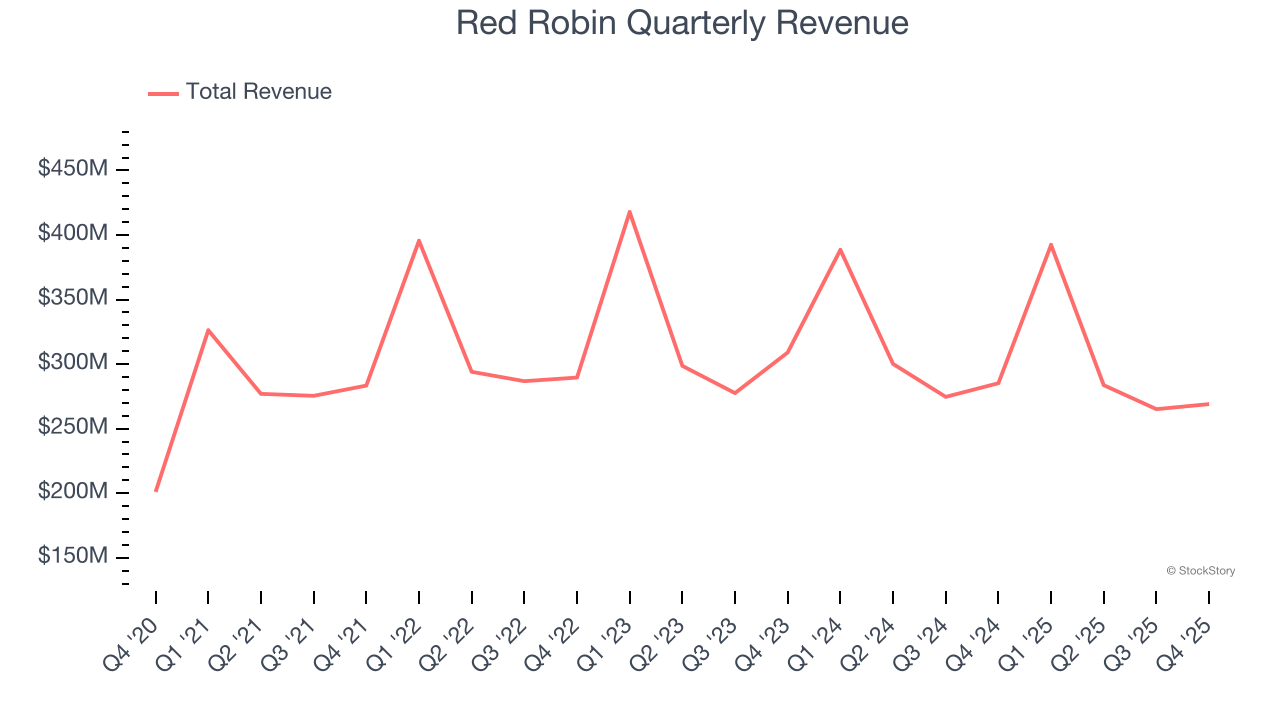

Burger restaurant chain Red Robin (NASDAQ: RRGB) reported revenue ahead of Wall Street’s expectations in Q4 CY2025, but sales fell by 5.7% year on year to $269 million. Its non-GAAP loss of $0.41 per share was 30.2% above analysts’ consensus estimates.

Is now the time to buy Red Robin? Find out by accessing our full research report, it’s free.

Red Robin (RRGB) Q4 CY2025 Highlights:

- Revenue: $269 million vs analyst estimates of $264.3 million (5.7% year-on-year decline, 1.8% beat)

- Adjusted EPS: -$0.41 vs analyst estimates of -$0.59 (30.2% beat)

- Adjusted EBITDA: $11.79 billion vs analyst estimates of $8.78 million (43.81% margin, significant beat)

- EBITDA guidance for the upcoming financial year 2026 is $71.5 million at the midpoint, above analyst estimates of $69.04 million

- Operating Margin: -1.5%, in line with the same quarter last year

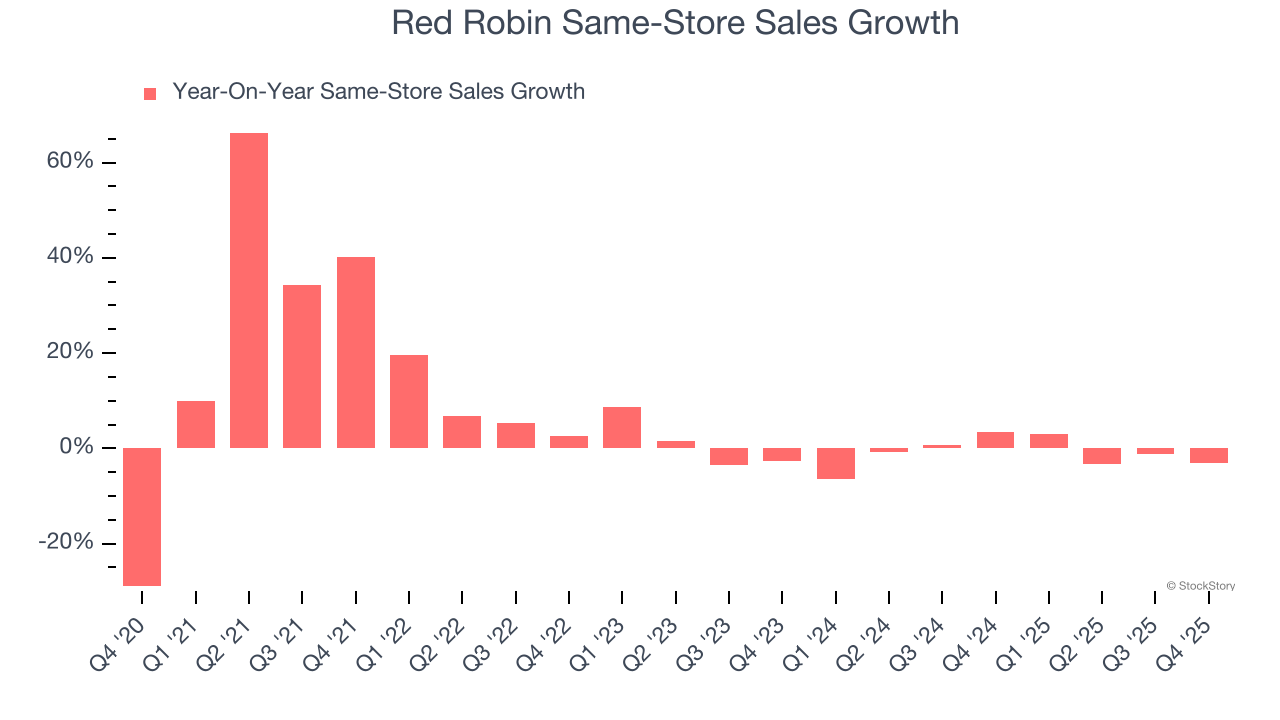

- Same-Store Sales fell 3.1% year on year (3.4% in the same quarter last year)

- Market Capitalization: $66.83 million

Company Overview

Known for its bottomless steak fries, Red Robin (NASDAQ: RRGB) is a chain of casual restaurants specializing in burgers and general American fare.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years.

With $1.21 billion in revenue over the past 12 months, Red Robin is a mid-sized restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale.

As you can see below, Red Robin struggled to generate demand over the last six years. Its sales dropped by 1.4% annually, a poor baseline for our analysis.

This quarter, Red Robin’s revenue fell by 5.7% year on year to $269 million but beat Wall Street’s estimates by 1.8%.

Looking ahead, sell-side analysts expect revenue to decline by 4.5% over the next 12 months, a deceleration versus the last six years. This projection doesn't excite us and indicates its menu offerings will see some demand headwinds.

While Wall Street chases Nvidia at all-time highs, an under-the-radar semiconductor supplier is dominating a critical AI component these giants can’t build without. Click here to access our free report one of our favorites growth stories.

Same-Store Sales

Same-store sales is an industry measure of whether revenue is growing at existing restaurants, and it is driven by customer visits (often called traffic) and the average spending per customer (ticket).

Red Robin’s demand within its existing dining locations has barely increased over the last two years as its same-store sales were flat.

In the latest quarter, Red Robin’s same-store sales fell by 3.1% year on year. This decrease represents a further deceleration from its historical levels. We hope the business can get back on track.

Key Takeaways from Red Robin’s Q4 Results

We were impressed by how significantly Red Robin blew past analysts’ EBITDA expectations this quarter. We were also glad its full-year EBITDA guidance exceeded Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 28.4% to $4.64 immediately following the results.

Sure, Red Robin had a solid quarter, but if we look at the bigger picture, is this stock a buy? We think that the latest quarter is only one piece of the longer-term business quality puzzle. Quality, when combined with valuation, can help determine if the stock is a buy. We cover that in our actionable full research report which you can read here (it’s free).