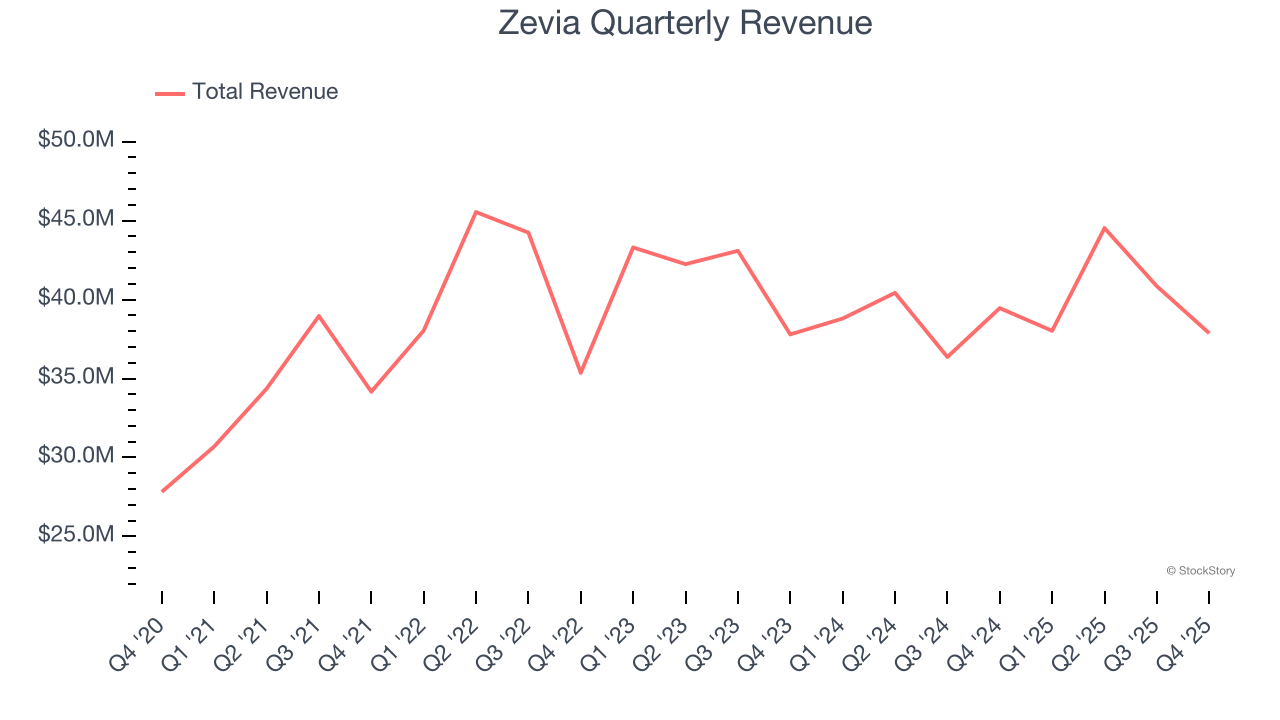

Beverage company Zevia (NYSE: ZVIA) fell short of the market’s revenue expectations in Q4 CY2025, with sales falling 4% year on year to $37.87 million. On the other hand, next quarter’s outlook exceeded expectations with revenue guided to $41 million at the midpoint, or 1.2% above analysts’ estimates. Its GAAP loss of $0.02 per share was in line with analysts’ consensus estimates.

Is now the time to buy Zevia? Find out by accessing our full research report, it’s free.

Zevia (ZVIA) Q4 CY2025 Highlights:

- Revenue: $37.87 million vs analyst estimates of $40.19 million (4% year-on-year decline, 5.8% miss)

- EPS (GAAP): -$0.02 vs analyst estimates of -$0.03 (in line)

- Adjusted EBITDA: $49,000 (0.1% margin, 101% year-on-year growth)

- Revenue Guidance for Q1 CY2026 is $41 million at the midpoint, above analyst estimates of $40.5 million

- EBITDA guidance for the upcoming financial year 2026 is -$250,000 at the midpoint, below analyst estimates of $2.04 million

- Operating Margin: -4%, up from -16.1% in the same quarter last year

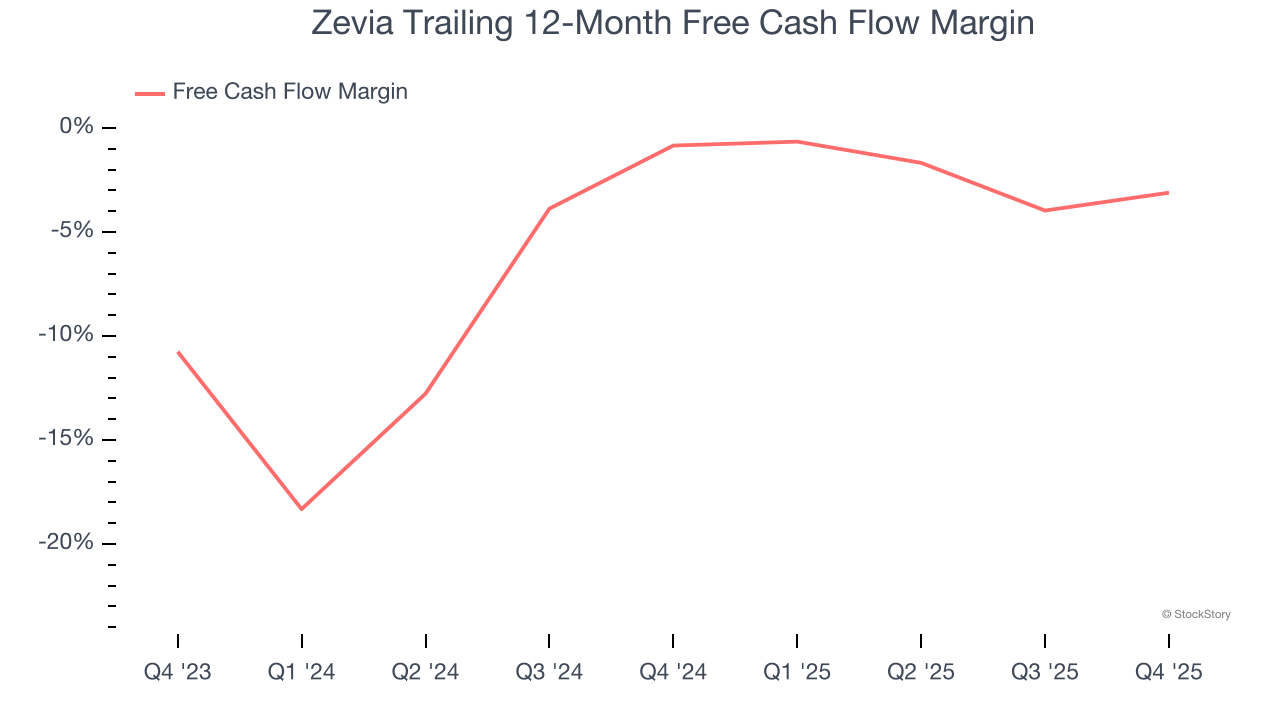

- Free Cash Flow was -$588,000 compared to -$2.04 million in the same quarter last year

- Market Capitalization: $101.1 million

Company Overview

With a primary focus on soda but also a presence in energy drinks and teas, Zevia (NYSE: ZVIA) is a better-for-you beverage company.

Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

With $161.3 million in revenue over the past 12 months, Zevia is a small consumer staples company, which sometimes brings disadvantages compared to larger competitors benefiting from economies of scale and negotiating leverage with retailers.

As you can see below, Zevia struggled to increase demand as its $161.3 million of sales for the trailing 12 months was close to its revenue three years ago. To its credit, however, consumers bought more of its products - we’ll explore what this means in the "Volume Growth" section.

This quarter, Zevia missed Wall Street’s estimates and reported a rather uninspiring 4% year-on-year revenue decline, generating $37.87 million of revenue. Company management is currently guiding for a 7.8% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 8.2% over the next 12 months, an acceleration versus the last three years. This projection is healthy and suggests its newer products will spur better top-line performance.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can’t use accounting profits to pay the bills.

Zevia’s demanding reinvestments have consumed many resources over the last two years, contributing to an average free cash flow margin of negative 2%. This means it lit $2.00 of cash on fire for every $100 in revenue.

Taking a step back, we can see that Zevia’s margin dropped by 2.3 percentage points over the last year. Almost any movement in the wrong direction is undesirable because it is already burning cash. If the trend continues, it could signal it’s becoming a more capital-intensive business.

Zevia burned through $588,000 of cash in Q4, equivalent to a negative 1.6% margin. The company’s cash burn was similar to its $2.04 million of lost cash in the same quarter last year.

Key Takeaways from Zevia’s Q4 Results

We were impressed by how significantly Zevia blew past analysts’ EBITDA expectations this quarter. We were also glad its EPS was in line with Wall Street’s estimates. On the other hand, its full-year EBITDA guidance missed and its revenue fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 6.5% to $1.45 immediately after reporting.

The latest quarter from Zevia’s wasn’t that good. One earnings report doesn’t define a company’s quality, though, so let’s explore whether the stock is a buy at the current price. If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here (it’s free).