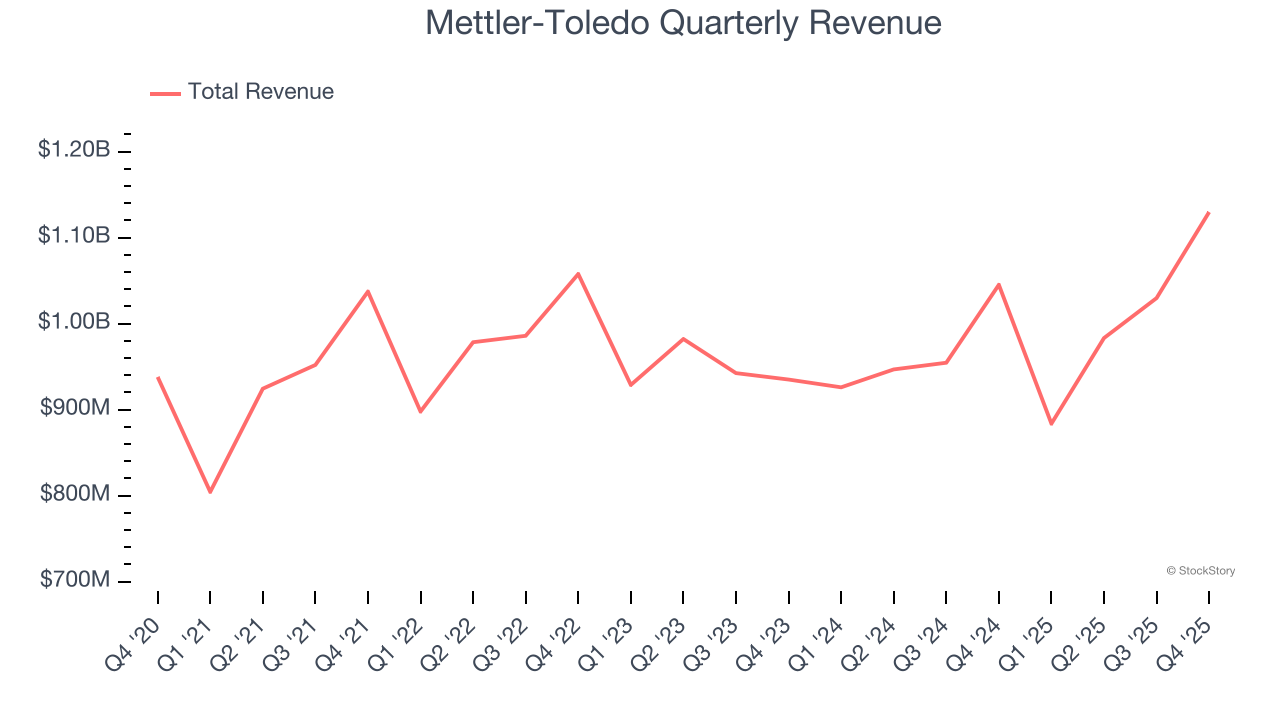

Precision measurement company Mettler-Toledo (NYSE: MTD) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 8.1% year on year to $1.13 billion. On the other hand, next quarter’s revenue guidance of $910.3 million was less impressive, coming in 3.1% below analysts’ estimates. Its non-GAAP profit of $13.36 per share was 4.3% above analysts’ consensus estimates.

Is now the time to buy Mettler-Toledo? Find out by accessing our full research report, it’s free.

Mettler-Toledo (MTD) Q4 CY2025 Highlights:

- Revenue: $1.13 billion vs analyst estimates of $1.10 billion (8.1% year-on-year growth, 2.3% beat)

- Adjusted EPS: $13.36 vs analyst estimates of $12.81 (4.3% beat)

- Revenue Guidance for Q1 CY2026 is $910.3 million at the midpoint, below analyst estimates of $939.6 million

- Adjusted EPS guidance for the upcoming financial year 2026 is $46.38 at the midpoint, beating analyst estimates by 1.2%

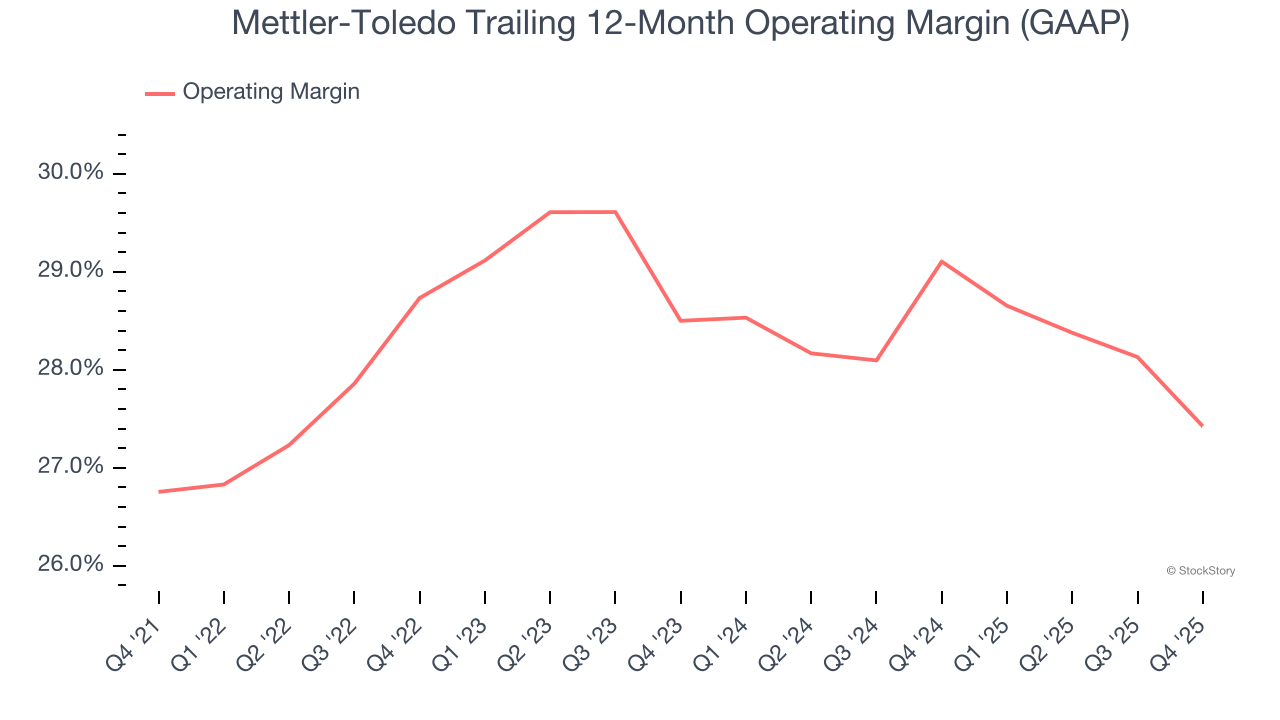

- Operating Margin: 29.1%, down from 31.9% in the same quarter last year

- Free Cash Flow Margin: 16.3%, down from 21.5% in the same quarter last year

- Market Capitalization: $28.39 billion

Patrick Kaltenbach, President and Chief Executive Officer, stated, “We had a great finish to the year with broad based growth by geography and product category. Our team continues to execute very well in a challenging environment and delivered strong Adjusted EPS growth for the quarter with excellent free cash flow conversion for the year.”

Company Overview

With roots dating back to the precision balance innovations of Swiss engineer Erhard Mettler, Mettler-Toledo (NYSE: MTD) manufactures precision weighing instruments, analytical equipment, and product inspection systems used in laboratories, industrial settings, and food retail.

Revenue Growth

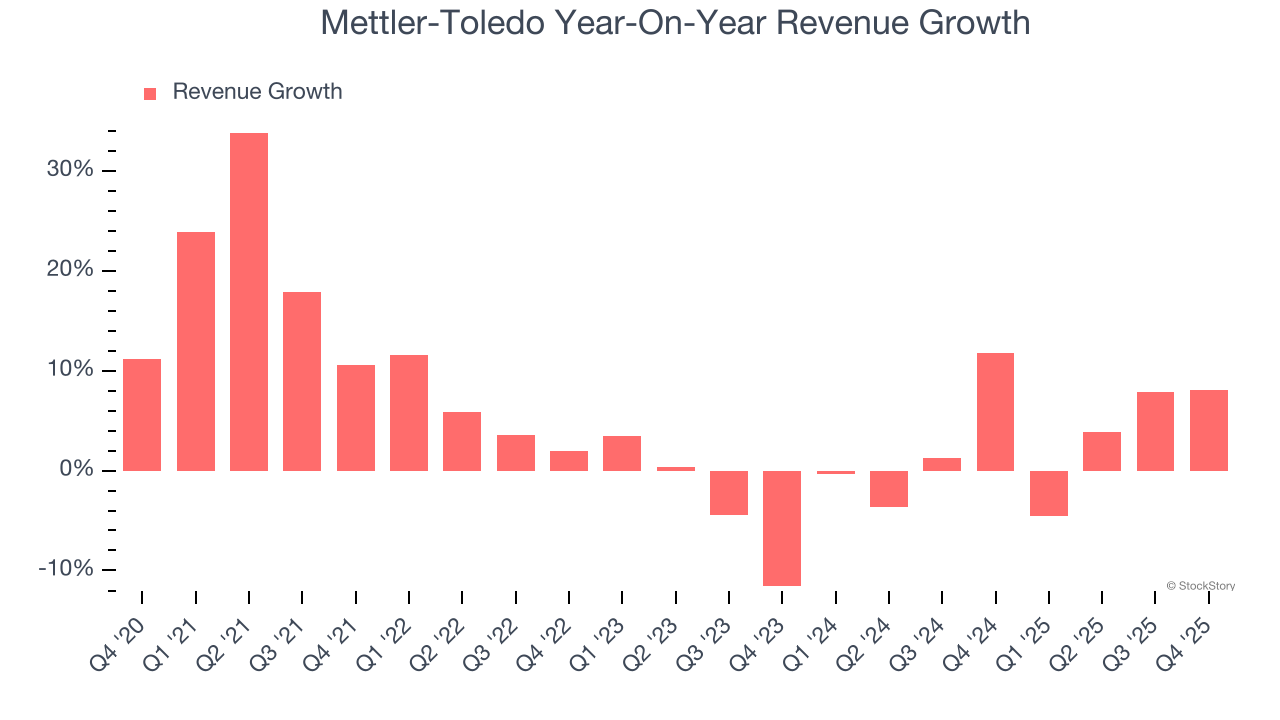

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, Mettler-Toledo’s 5.5% annualized revenue growth over the last five years was mediocre. This fell short of our benchmark for the healthcare sector and is a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Mettler-Toledo’s recent performance shows its demand has slowed as its annualized revenue growth of 3.1% over the last two years was below its five-year trend.

This quarter, Mettler-Toledo reported year-on-year revenue growth of 8.1%, and its $1.13 billion of revenue exceeded Wall Street’s estimates by 2.3%. Company management is currently guiding for a 3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 4.2% over the next 12 months, similar to its two-year rate. While this projection implies its newer products and services will catalyze better top-line performance, it is still below the sector average.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Operating Margin

Mettler-Toledo’s operating margin might fluctuated slightly over the last 12 months but has generally stayed the same, averaging 28.1% over the last five years. This profitability was top-notch for a healthcare business, showing it’s an well-run company with an efficient cost structure.

Analyzing the trend in its profitability, Mettler-Toledo’s operating margin of 27.4% for the trailing 12 months may be around the same as five years ago, but it has decreased by 1.1 percentage points over the last two years.

This quarter, Mettler-Toledo generated an operating margin profit margin of 29.1%, down 2.8 percentage points year on year. This contraction shows it was less efficient because its expenses grew faster than its revenue.

Earnings Per Share

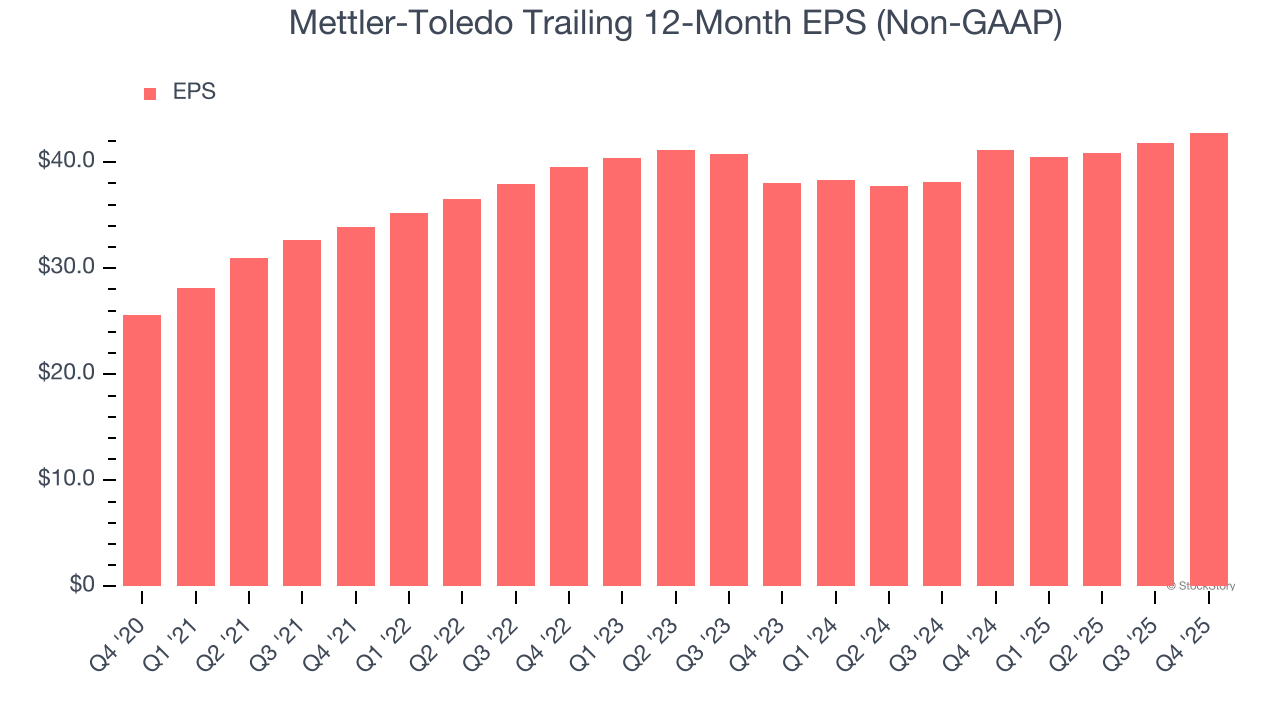

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Mettler-Toledo’s EPS grew at a remarkable 10.8% compounded annual growth rate over the last five years, higher than its 5.5% annualized revenue growth. However, this alone doesn’t tell us much about its business quality because its operating margin didn’t improve.

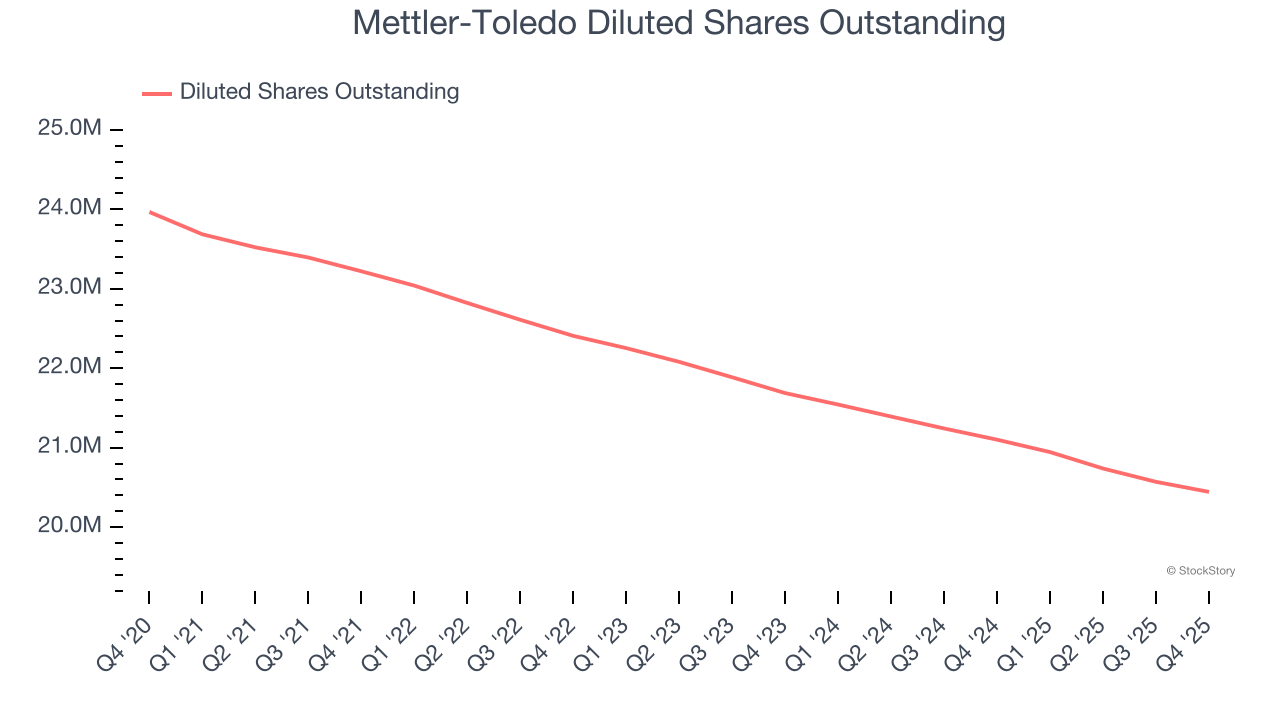

Diving into Mettler-Toledo’s quality of earnings can give us a better understanding of its performance. A five-year view shows that Mettler-Toledo has repurchased its stock, shrinking its share count by 14.7%. This tells us its EPS outperformed its revenue not because of increased operational efficiency but financial engineering, as buybacks boost per share earnings.

In Q4, Mettler-Toledo reported adjusted EPS of $13.36, up from $12.41 in the same quarter last year. This print beat analysts’ estimates by 4.3%. Over the next 12 months, Wall Street expects Mettler-Toledo’s full-year EPS of $42.79 to grow 7.2%.

Key Takeaways from Mettler-Toledo’s Q4 Results

It was encouraging to see Mettler-Toledo beat analysts’ revenue expectations this quarter. We were also happy its full-year EPS guidance narrowly outperformed Wall Street’s estimates. On the other hand, its revenue guidance for next quarter missed and its EPS guidance for next quarter fell short of Wall Street’s estimates. Overall, this was a weaker quarter. The stock remained flat at $1,384 immediately after reporting.

Big picture, is Mettler-Toledo a buy here and now? What happened in the latest quarter matters, but not as much as longer-term business quality and valuation, when deciding whether to invest in this stock. We cover that in our actionable full research report which you can read here (it’s free).